The Qualys, Inc. (NASDAQ:QLYS) share price has done very well over the last month, posting an excellent gain of 32%. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 4.9% over the last year.

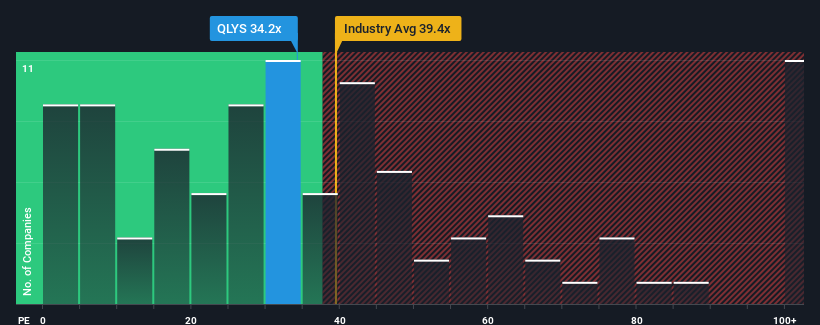

After such a large jump in price, Qualys may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 34.2x, since almost half of all companies in the United States have P/E ratios under 18x and even P/E's lower than 11x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Qualys certainly has been doing a good job lately as it's been growing earnings more than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NasdaqGS:QLYS Price to Earnings Ratio vs Industry November 7th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Qualys.

How Is Qualys' Growth Trending?

In order to justify its P/E ratio, Qualys would need to produce outstanding growth well in excess of the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 23% last year. The strong recent performance means it was also able to grow EPS by 149% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 3.2% per year over the next three years. Meanwhile, the rest of the market is forecast to expand by 11% each year, which is noticeably more attractive.

In light of this, it's alarming that Qualys' P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Final Word

Qualys' P/E is flying high just like its stock has during the last month. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Qualys' analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for Qualys with six simple checks on some of these key factors.

Of course, you might also be able to find a better stock than Qualys. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

In order to justify its P/E ratio, Qualys would need to produce outstanding growth well in excess of the market.

In order to justify its P/E ratio, Qualys would need to produce outstanding growth well in excess of the market.

爲了證明其P / E比率,科力斯需要產生遠遠超過市場的傑出增長。

爲了證明其P / E比率,科力斯需要產生遠遠超過市場的傑出增長。