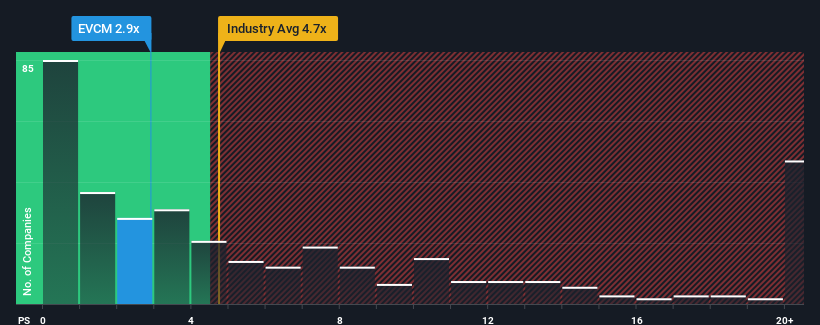

You may think that with a price-to-sales (or "P/S") ratio of 2.9x EverCommerce Inc. (NASDAQ:EVCM) is a stock worth checking out, seeing as almost half of all the Software companies in the United States have P/S ratios greater than 4.7x and even P/S higher than 12x aren't out of the ordinary. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

NasdaqGS:EVCM Price to Sales Ratio vs Industry November 5th 2024

How EverCommerce Has Been Performing

With revenue growth that's inferior to most other companies of late, EverCommerce has been relatively sluggish. The P/S ratio is probably low because investors think this lacklustre revenue performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Keen to find out how analysts think EverCommerce's future stacks up against the industry? In that case, our free report is a great place to start.

Do Revenue Forecasts Match The Low P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as low as EverCommerce's is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered a decent 6.2% gain to the company's revenues. Pleasingly, revenue has also lifted 70% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 2.7% during the coming year according to the eleven analysts following the company. That's shaping up to be materially lower than the 25% growth forecast for the broader industry.

With this information, we can see why EverCommerce is trading at a P/S lower than the industry. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From EverCommerce's P/S?

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of EverCommerce's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. It's hard to see the share price rising strongly in the near future under these circumstances.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for EverCommerce with six simple checks.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered a decent 6.2% gain to the company's revenues. Pleasingly, revenue has also lifted 70% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Retrospectively, the last year delivered a decent 6.2% gain to the company's revenues. Pleasingly, revenue has also lifted 70% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

回顧過去一年,公司的營業收入取得了不錯的6.2%增長。令人高興的是,營業收入也比三年前總體上增長了70%,部分得益於過去12個月的增長。因此,股東們肯定會欣喜看到這些中期營收增長率。

回顧過去一年,公司的營業收入取得了不錯的6.2%增長。令人高興的是,營業收入也比三年前總體上增長了70%,部分得益於過去12個月的增長。因此,股東們肯定會欣喜看到這些中期營收增長率。