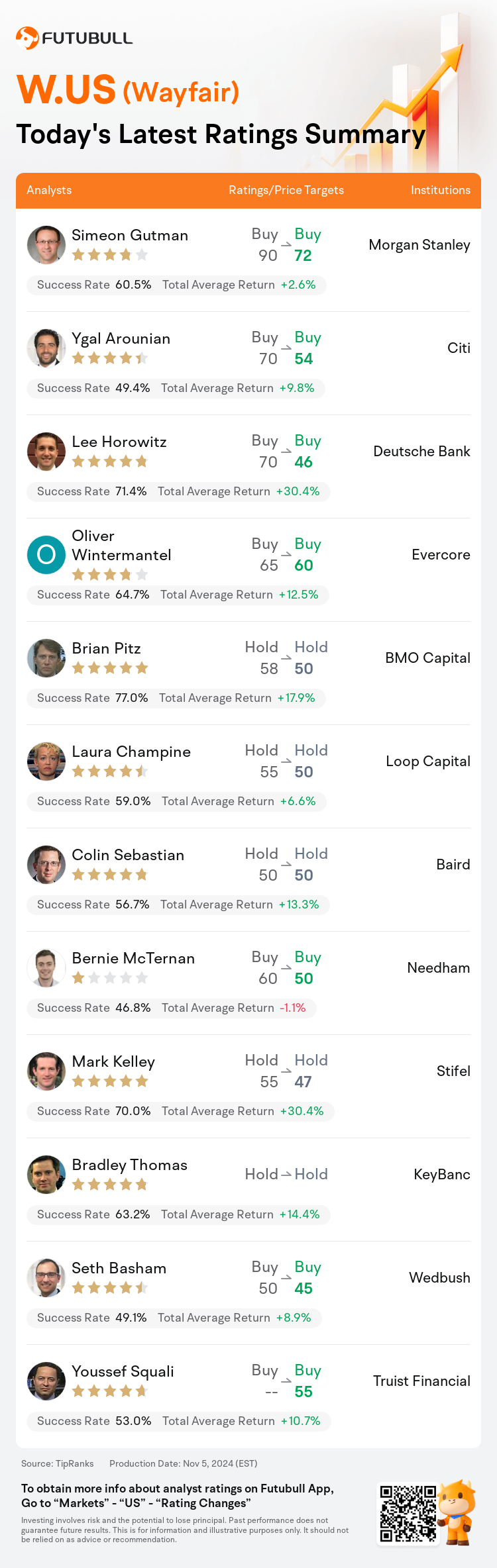

On Nov 05, major Wall Street analysts update their ratings for $Wayfair (W.US)$, with price targets ranging from $45 to $72.

Morgan Stanley analyst Simeon Gutman maintains with a buy rating, and adjusts the target price from $90 to $72.

Citi analyst Ygal Arounian maintains with a buy rating, and adjusts the target price from $70 to $54.

Deutsche Bank analyst Lee Horowitz maintains with a buy rating, and adjusts the target price from $70 to $46.

Deutsche Bank analyst Lee Horowitz maintains with a buy rating, and adjusts the target price from $70 to $46.

Evercore analyst Oliver Wintermantel maintains with a buy rating, and adjusts the target price from $65 to $60.

BMO Capital analyst Brian Pitz maintains with a hold rating, and adjusts the target price from $58 to $50.

Furthermore, according to the comprehensive report, the opinions of $Wayfair (W.US)$'s main analysts recently are as follows:

Wayfair's Q3 results demonstrate the company's capacity to expand market share and maintain cash flow amidst anticipation for a resurgence in industry demand. The company is positioned to counter the notion that increased promotions would lead to gross margin compression by leveraging its relationship with suppliers.

Wayfair's recent financial results presented a mixed picture, with the third quarter performance surpassing expectations, although the fourth quarter forecast suggests more daunting challenges ahead. The overall economic backdrop continues to cast a significant shadow over Wayfair's sector, curbing its growth prospects. Despite the prevailing market conditions, there is an anticipation of the stock trading around these macro influences, with a positive long-term outlook remaining intact.

Interest rates' eventual decrease is anticipated to positively influence home-related sales. Though it's hoped that recent rate reductions are the beginning of a series, there was a note that third-quarter sales dipped 3%, surpassing the projected 1% fall. It's expected that Wayfair will prudently control its overhead expenses while awaiting a market rebound.

The firm adopts a more cautious stance as consumer response to promotions has been tepid leading up to the election. Additionally, the company's ongoing initiatives to manage its take-rate are expected to keep gross margins around the low 30% threshold through the first half of FY25. Despite this, Wayfair's strategies to stimulate demand appear to be contributing to market share gains. Moreover, enhancements to the Loyalty program are anticipated to boost the frequency of customer purchases to 3 to 8 times annually.

The most recent quarterly results for Wayfair were generally on par regarding revenue and adjusted EBITDA, but the guidance for Q4 suggested a potential decline in performance towards the end of the quarter. A more favorable outlook on the company might emerge with evidence of an enhanced overall market for their category and tangible benefits from recent efforts, such as the introduction of a new loyalty scheme and the establishment of a brick-and-mortar retail location.

Here are the latest investment ratings and price targets for $Wayfair (W.US)$ from 12 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

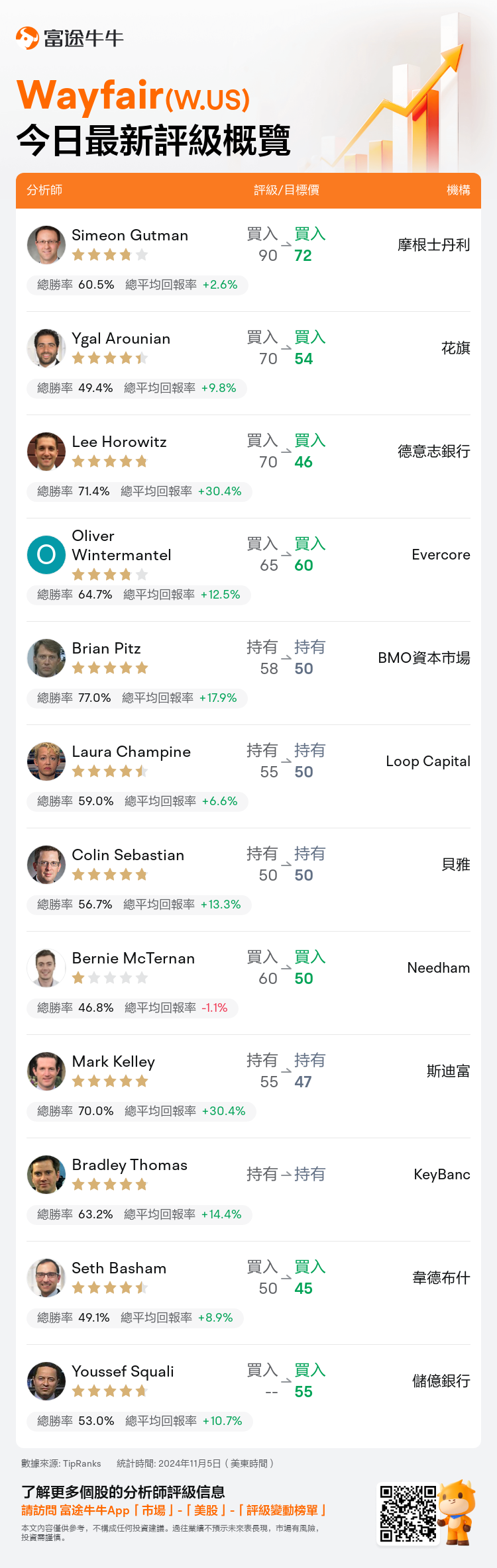

美東時間11月5日,多家華爾街大行更新了$Wayfair (W.US)$的評級,目標價介於45美元至72美元。

摩根士丹利分析師Simeon Gutman維持買入評級,並將目標價從90美元下調至72美元。

花旗分析師Ygal Arounian維持買入評級,並將目標價從70美元下調至54美元。

德意志銀行分析師Lee Horowitz維持買入評級,並將目標價從70美元下調至46美元。

德意志銀行分析師Lee Horowitz維持買入評級,並將目標價從70美元下調至46美元。

Evercore分析師Oliver Wintermantel維持買入評級,並將目標價從65美元下調至60美元。

BMO資本市場分析師Brian Pitz維持持有評級,並將目標價從58美元下調至50美元。

此外,綜合報道,$Wayfair (W.US)$近期主要分析師觀點如下:

wayfair的第三季度結果顯示該公司有能力擴大市場份額,並在行業需求復甦預期中保持現金流。該公司有能力應對增加促銷導致毛利率下壓的觀念,通過與供應商的關係來實現。

wayfair最近的財務業績呈現出一幅褒貶不一的畫面,第三季度表現超出預期,儘管第四季度展望表明面臨更多具挑戰性的問題。整體經濟背景繼續給wayfair所在的板塊蒙上重重陰影,抑制了其增長前景。儘管市場條件仍然存在,但人們預計股票將受到這些宏觀影響的影響,樂觀的長期前景仍將保持完好。

預期利率最終下降將積極影響與住房相關的銷售。儘管希望最近的減息只是一系列減息的開始,但注意到第三季度銷售下滑了3%,超過了預計的1%下降。預計wayfair將在等待市場反彈時謹慎控制其開支。

公司採取更謹慎的態度,因爲消費者對促銷的反應在選舉之前相對冷淡。此外,公司持續管理其佣金率的舉措預計將使毛利率維持在25財年上半年的低30%門檻附近。儘管如此,wayfair刺激需求的策略似乎正在增加市場份額。此外,忠誠計劃的改進預計將提升客戶購買頻率,每年3至8次。

wayfair最近的季度業績在營業收入和調整後的息稅折舊攤銷前利潤方面大致持平,但第四季度的指引表明季末的表現有可能下降。隨着在該類別的整體市場以及最近努力所帶來的實實在在的收益的證據的出現,對該公司的更爲有利的前景可能會出現,比如推出新的忠誠計劃和建立實體零售店。

以下爲今日12位分析師對$Wayfair (W.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。