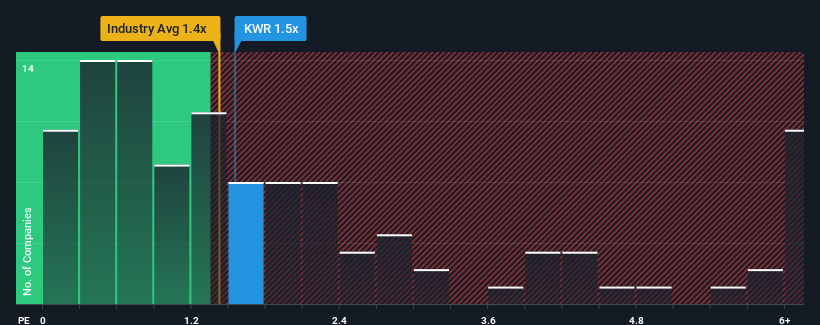

With a median price-to-sales (or "P/S") ratio of close to 1.3x in the Chemicals industry in the United States, you could be forgiven for feeling indifferent about Quaker Chemical Corporation's (NYSE:KWR) P/S ratio of 1.5x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

NYSE:KWR Price to Sales Ratio vs Industry November 2nd 2024

What Does Quaker Chemical's Recent Performance Look Like?

Quaker Chemical has been struggling lately as its revenue has declined faster than most other companies. One possibility is that the P/S is moderate because investors think the company's revenue trend will eventually fall in line with most others in the industry. You'd much rather the company improve its revenue if you still believe in the business. Or at the very least, you'd be hoping it doesn't keep underperforming if your plan is to pick up some stock while it's not in favour.

Want the full picture on analyst estimates for the company? Then our free report on Quaker Chemical will help you uncover what's on the horizon.

How Is Quaker Chemical's Revenue Growth Trending?

In order to justify its P/S ratio, Quaker Chemical would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a frustrating 5.5% decrease to the company's top line. Regardless, revenue has managed to lift by a handy 9.6% in aggregate from three years ago, thanks to the earlier period of growth. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 2.5% during the coming year according to the six analysts following the company. With the industry predicted to deliver 3.2% growth , the company is positioned for a comparable revenue result.

With this information, we can see why Quaker Chemical is trading at a fairly similar P/S to the industry. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Bottom Line On Quaker Chemical's P/S

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

A Quaker Chemical's P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Chemicals industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. If all things remain constant, the possibility of a drastic share price movement remains fairly remote.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Quaker Chemical with six simple checks.

If you're unsure about the strength of Quaker Chemical's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered a frustrating 5.5% decrease to the company's top line. Regardless, revenue has managed to lift by a handy 9.6% in aggregate from three years ago, thanks to the earlier period of growth. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

Retrospectively, the last year delivered a frustrating 5.5% decrease to the company's top line. Regardless, revenue has managed to lift by a handy 9.6% in aggregate from three years ago, thanks to the earlier period of growth. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

回顧過去一年,公司的營業收入出現令人沮喪的5.5%下降。儘管如此,由於早期增長的影響,營業收入總體上成功增長了可觀的9.6%,從三年前開始。因此,儘管他們希望繼續保持增長勢頭,股東們對中期營收增長率大致滿意。

回顧過去一年,公司的營業收入出現令人沮喪的5.5%下降。儘管如此,由於早期增長的影響,營業收入總體上成功增長了可觀的9.6%,從三年前開始。因此,儘管他們希望繼續保持增長勢頭,股東們對中期營收增長率大致滿意。