Unfortunately for some shareholders, the Enviri Corporation (NYSE:NVRI) share price has dived 29% in the last thirty days, prolonging recent pain. Longer-term, the stock has been solid despite a difficult 30 days, gaining 13% in the last year.

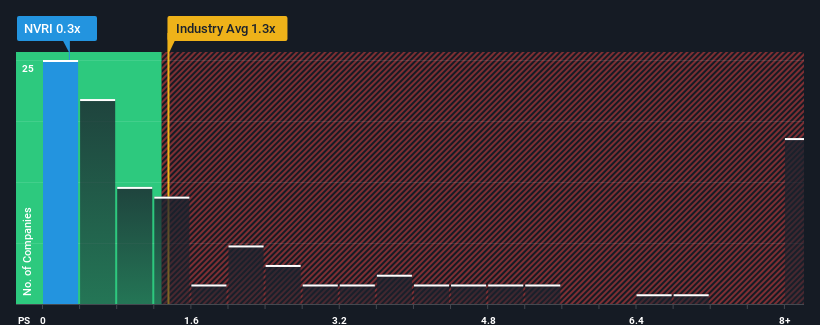

Since its price has dipped substantially, Enviri's price-to-sales (or "P/S") ratio of 0.3x might make it look like a buy right now compared to the Commercial Services industry in the United States, where around half of the companies have P/S ratios above 1.3x and even P/S above 4x are quite common. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

NYSE:NVRI Price to Sales Ratio vs Industry November 2nd 2024

How Has Enviri Performed Recently?

While the industry has experienced revenue growth lately, Enviri's revenue has gone into reverse gear, which is not great. It seems that many are expecting the poor revenue performance to persist, which has repressed the P/S ratio. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Enviri.

How Is Enviri's Revenue Growth Trending?

Enviri's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Retrospectively, the last year delivered a frustrating 6.6% decrease to the company's top line. Still, the latest three year period has seen an excellent 33% overall rise in revenue, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

Looking ahead now, revenue is anticipated to climb by 7.8% per year during the coming three years according to the four analysts following the company. That's shaping up to be similar to the 9.2% each year growth forecast for the broader industry.

In light of this, it's peculiar that Enviri's P/S sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

The Bottom Line On Enviri's P/S

The southerly movements of Enviri's shares means its P/S is now sitting at a pretty low level. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've seen that Enviri currently trades on a lower than expected P/S since its forecast growth is in line with the wider industry. Despite average revenue growth estimates, there could be some unobserved threats keeping the P/S low. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

The company's balance sheet is another key area for risk analysis. Take a look at our free balance sheet analysis for Enviri with six simple checks on some of these key factors.

If these risks are making you reconsider your opinion on Enviri, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Enviri's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Enviri's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Enviri的市銷率將會與那些預期增長有限,並且重要性表現不如行業板塊的公司相類似。

Enviri的市銷率將會與那些預期增長有限,並且重要性表現不如行業板塊的公司相類似。