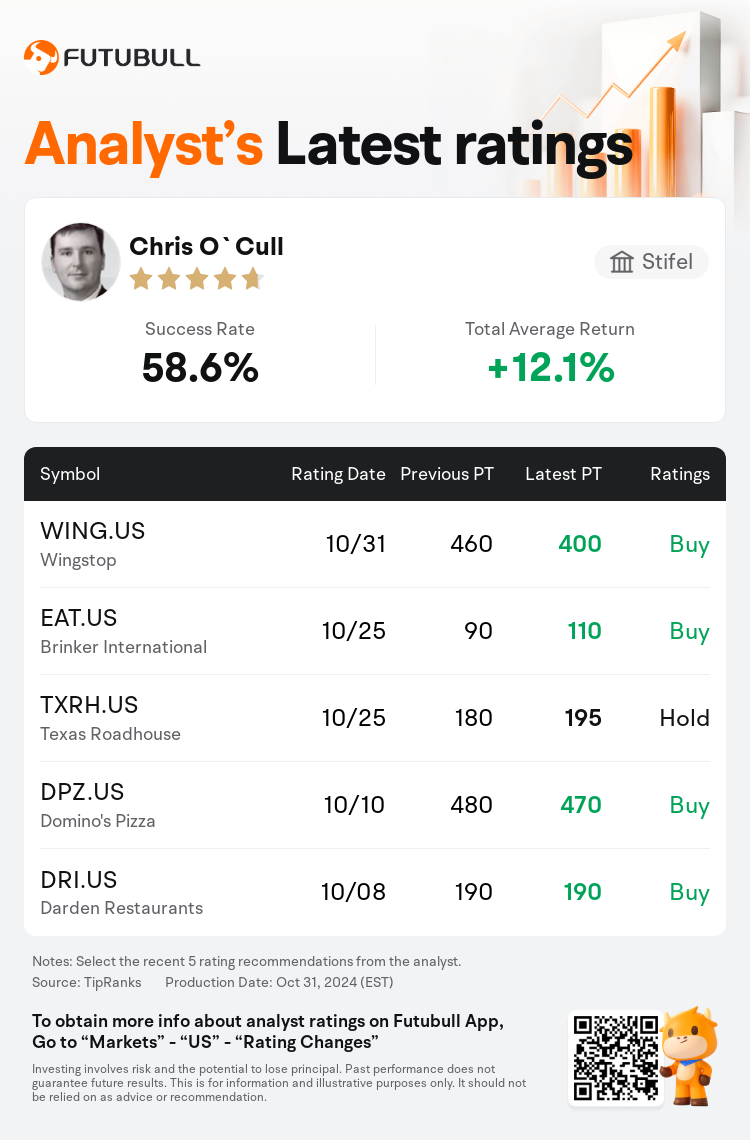

Stifel analyst Chris O`Cull maintains $Wingstop (WING.US)$ with a buy rating, and adjusts the target price from $460 to $400.

According to TipRanks data, the analyst has a success rate of 58.6% and a total average return of 12.1% over the past year.

Furthermore, according to the comprehensive report, the opinions of $Wingstop (WING.US)$'s main analysts recently are as follows:

Furthermore, according to the comprehensive report, the opinions of $Wingstop (WING.US)$'s main analysts recently are as follows:

The company's Q3 results did not meet the high expectations yet still displayed significant strength with a 21% increase in comparable store sales led by traffic, and the guidance for 2024 units was enhanced, indicating strong franchisee demand. Analysts recommend purchasing shares following the post-earnings decline, citing Wingstop's consistent 40%-plus three-year compounded comparable store sales.

Wingstop's third-quarter earnings per share fell short, owing to somewhat weaker comparable store sales, softer restaurant margins, and increased general and administrative expenses coupled with higher taxes. Despite this, the robust momentum of Wingstop's overall business persists, with its long-term potential remaining intact. However, a current slowdown in comparable store sales growth may restrain the stock until a more evident stabilization in light of the comp and valuation dynamics.

The recent post-quarterly results decline in Wingstop's valuation is perceived as excessive. The view is that the company stands out in the industry with its ability to drive transaction growth in various economic conditions over short, medium, and long-term periods. It's anticipated that the company's continued outperformance in same-store sales will propel superior unit economics, which could, in turn, lead to an increase in unit growth and annual long-term EBITDA growth surpassing the current expectations set by the company's management.

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

斯迪富分析師Chris O`Cull維持$Wingstop (WING.US)$買入評級,並將目標價從460美元下調至400美元。

根據TipRanks數據顯示,該分析師近一年總勝率為58.6%,總平均回報率為12.1%。

此外,綜合報道,$Wingstop (WING.US)$近期主要分析師觀點如下:

此外,綜合報道,$Wingstop (WING.US)$近期主要分析師觀點如下:

公司Q3的業績雖然未達到高預期,但仍表現出顯著實力,可比店鋪銷售增長21%,主要由流量驅動,2024年單位指引得到加強,表明強勁的加盟商需求。分析師建議在季度業績下滑後購買股票,稱讚Wingstop連續40%以上的三年複合可比店鋪銷售。

Wingstop第三季度每股收益不及預期,因可比店鋪銷售略有疲軟,餐廳利潤較低,一般和管理費用增加,再加上較高稅收。儘管如此,Wingstop整體業務的強勁勢頭仍在持續,其長期潛力仍然保持完好。然而,目前可比店鋪銷售增長的放緩可能會使股票受到限制,直到更明顯的穩定在比較和估值動態的光芒中。

最近季度業績下滑導致Wingstop估值被認爲過度。觀點認爲公司在行業中脫穎而出,能夠在短期、中期和長期各種經濟條件下推動交易增長。預計公司持續在同店銷售中的表現將推動卓越的單位經濟學,進而導致單位增長和年度長期EBITDA增長超過公司管理層設定的目前預期。

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。