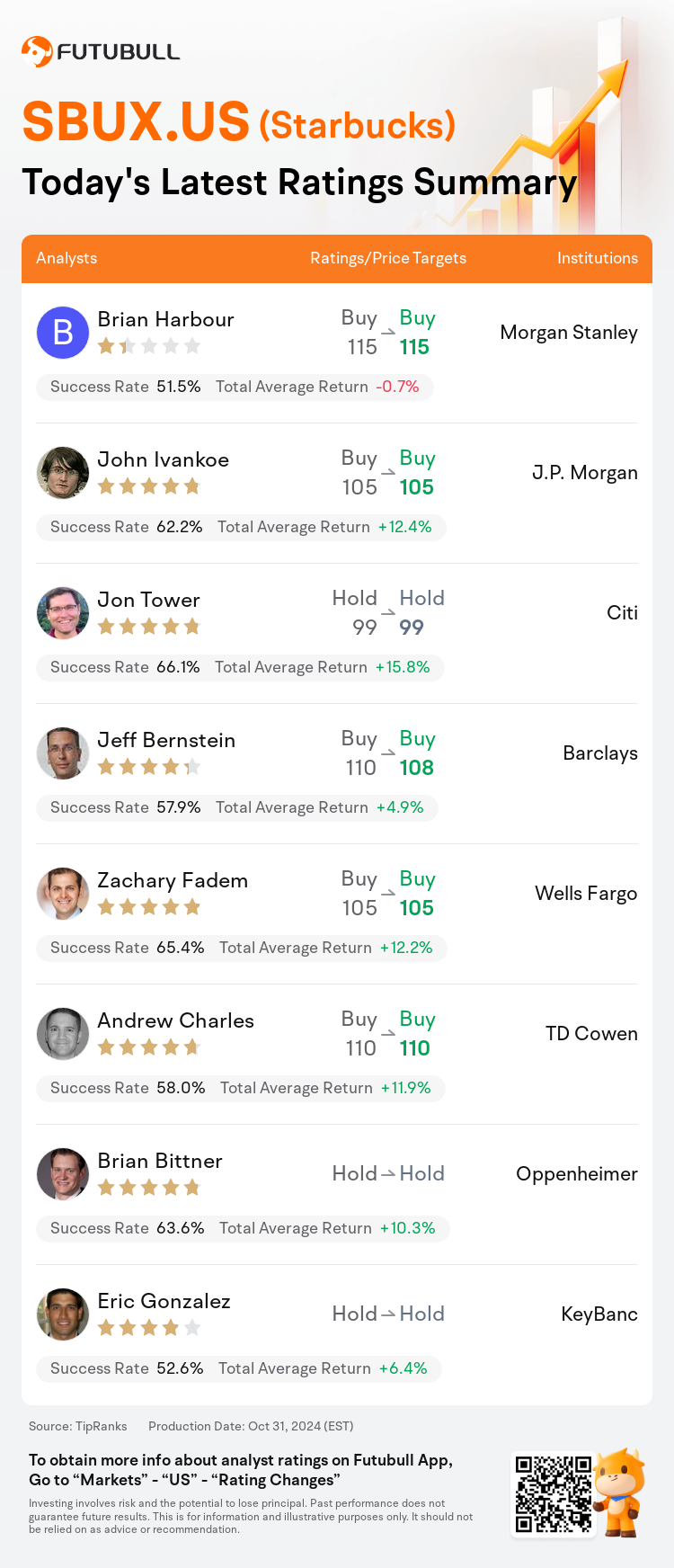

On Oct 31, major Wall Street analysts update their ratings for $Starbucks (SBUX.US)$, with price targets ranging from $99 to $115.

Morgan Stanley analyst Brian Harbour maintains with a buy rating, and maintains the target price at $115.

J.P. Morgan analyst John Ivankoe maintains with a buy rating, and maintains the target price at $105.

Citi analyst Jon Tower maintains with a hold rating, and maintains the target price at $99.

Citi analyst Jon Tower maintains with a hold rating, and maintains the target price at $99.

Barclays analyst Jeff Bernstein maintains with a buy rating, and adjusts the target price from $110 to $108.

Wells Fargo analyst Zachary Fadem maintains with a buy rating, and maintains the target price at $105.

Furthermore, according to the comprehensive report, the opinions of $Starbucks (SBUX.US)$'s main analysts recently are as follows:

Following the earnings report, it's noted that Starbucks is undertaking numerous initiatives aimed at bolstering the brand over both short and long terms. Although these strategies are not expected to produce immediate results, they lay out a clear vision that is anticipated to attract large-cap, growth investors. The sentiment suggests that these shares are poised for an upswing in advance of the company's anticipated recovery.

Starbucks' strategic initiatives are beginning to crystallize, aligning with anticipations set prior to the quarter. Nonetheless, unless there is a significant positive shift in costs in future quarters, it seems likely there will be a considerable adjustment to earnings in fiscal 2025, casting doubts on the attractiveness of the stock's current valuation.

The firm's perspective is that Starbucks' current valuation accurately encompasses the growing challenges related to near-term revenue and profit projections. This is balanced by a certain degree of assurance in the management's capacity for delivering sustained yearly growth in operating margins and earnings per share, that align with the company's historical growth patterns.

The preliminary announcement of the fiscal Q4 outcomes last week shifted the emphasis during the earnings call towards the company's future prospects. While the upcoming quarters are anticipated to pose challenges, there is an expectation that the latter half of 2025 will provide substantial signs that the strategic plan is effective. Observations suggest optimism regarding the comprehensive nature of the new CEO's plan and its potential to significantly enhance the customer experience and the company's overall direction.

Here are the latest investment ratings and price targets for $Starbucks (SBUX.US)$ from 8 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

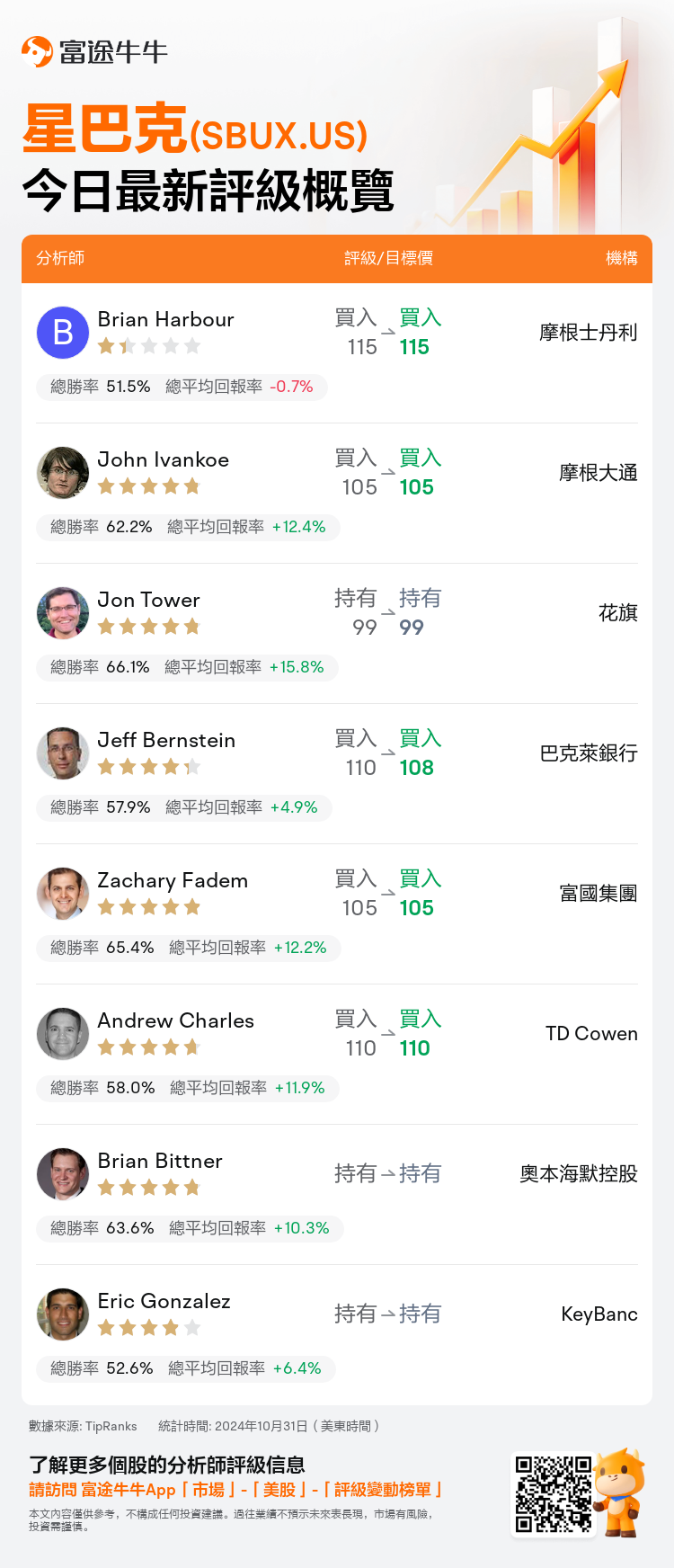

美東時間10月31日,多家華爾街大行更新了$星巴克 (SBUX.US)$的評級,目標價介於99美元至115美元。

摩根士丹利分析師Brian Harbour維持買入評級,維持目標價115美元。

摩根大通分析師John Ivankoe維持買入評級,維持目標價105美元。

花旗分析師Jon Tower維持持有評級,維持目標價99美元。

花旗分析師Jon Tower維持持有評級,維持目標價99美元。

巴克萊銀行分析師Jeff Bernstein維持買入評級,並將目標價從110美元下調至108美元。

富國集團分析師Zachary Fadem維持買入評級,維持目標價105美元。

此外,綜合報道,$星巴克 (SBUX.US)$近期主要分析師觀點如下:

在業績報告之後,注意到星巴克正在進行許多旨在加強品牌長短期影響力的舉措。儘管這些策略不太可能立即產生結果,但它們確立了一個清晰的願景,預計將吸引大市值成長型投資者。市場情緒表明,這些股票有望在公司預期的復甦之前出現上升趨勢。

星巴克的戰略舉措開始明晰化,與季度前預期相符。然而,除非未來幾個季度成本出現顯著正面變化,否則很可能會在2025財年出現相當大的盈利調整,對當前股價估值的吸引力產生懷疑。

公司認爲,星巴克當前的估值準確地包含了與短期營收和利潤預測相關的日益增多的挑戰。這一趨勢得到一定程度的平衡,即確保了管理層在提供持續年度收入增長和每股收益方面的能力,這與公司歷史增長模式一致。

上週發佈的財季Q4結果初步宣佈轉移了盈利會的重點至公司未來前景。雖然未來幾個季度預計會面臨挑戰,但人們期待2025年下半年將提供大量跡象表明戰略計劃有效。觀察表明了對新CEO計劃全面性質和其潛力顯着提升客戶體驗及公司整體方向的樂觀態度。

以下爲今日8位分析師對$星巴克 (SBUX.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。