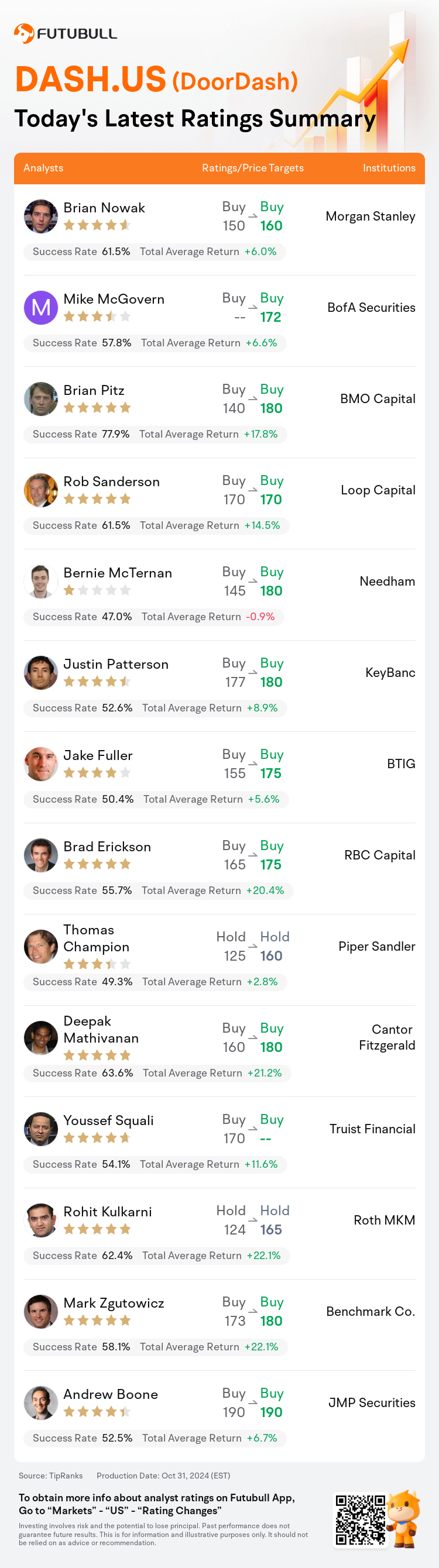

On Oct 31, major Wall Street analysts update their ratings for $DoorDash (DASH.US)$, with price targets ranging from $160 to $190.

Morgan Stanley analyst Brian Nowak maintains with a buy rating, and adjusts the target price from $150 to $160.

BofA Securities analyst Mike McGovern maintains with a buy rating, and sets the target price at $172.

BMO Capital analyst Brian Pitz maintains with a buy rating, and adjusts the target price from $140 to $180.

BMO Capital analyst Brian Pitz maintains with a buy rating, and adjusts the target price from $140 to $180.

Loop Capital analyst Rob Sanderson maintains with a buy rating, and maintains the target price at $170.

Needham analyst Bernie McTernan maintains with a buy rating, and adjusts the target price from $145 to $180.

Furthermore, according to the comprehensive report, the opinions of $DoorDash (DASH.US)$'s main analysts recently are as follows:

Following a solid quarter that surpassed revenue expectations but offered less margin growth, analysts maintain a positive outlook on DoorDash. Projections for 2025 now anticipate higher gross order value, revenue, and EBITDA than previously forecasted.

DoorDash has demonstrated robust Q3 EBITDA and anticipates a vigorous Q4, propelled by consistent expansion in the restaurant sector, ongoing substantial growth in new verticals and international markets, coupled with enhanced unit economics.

DoorDash's Q3 results were impressive, showcasing robust gross order value guidance and EBITDA that was marginally below buy-side forecasts. Notably, the company's sustained order growth is being fueled by rising order frequency, unprecedented customer loyalty which is further enhanced by new partnerships, an upswing in gross profit suggesting reduced profit impact from emerging verticals, and an uptick in advertising revenue.

DoorDash reported Q3 gross order values that surpassed expectations, accompanied by EBITDA improvements. These enhancements were a result of gross margin leverage paired with reduced legal fees. Additionally, DoorDash achieved a record high in order frequency, which can be attributed to the enhanced variety of product offerings.

Expectations were high leading into the quarterly earnings report, yet DoorDash delivered with strong growth, increased margins, and its initial positive net income on a GAAP basis.

Here are the latest investment ratings and price targets for $DoorDash (DASH.US)$ from 14 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

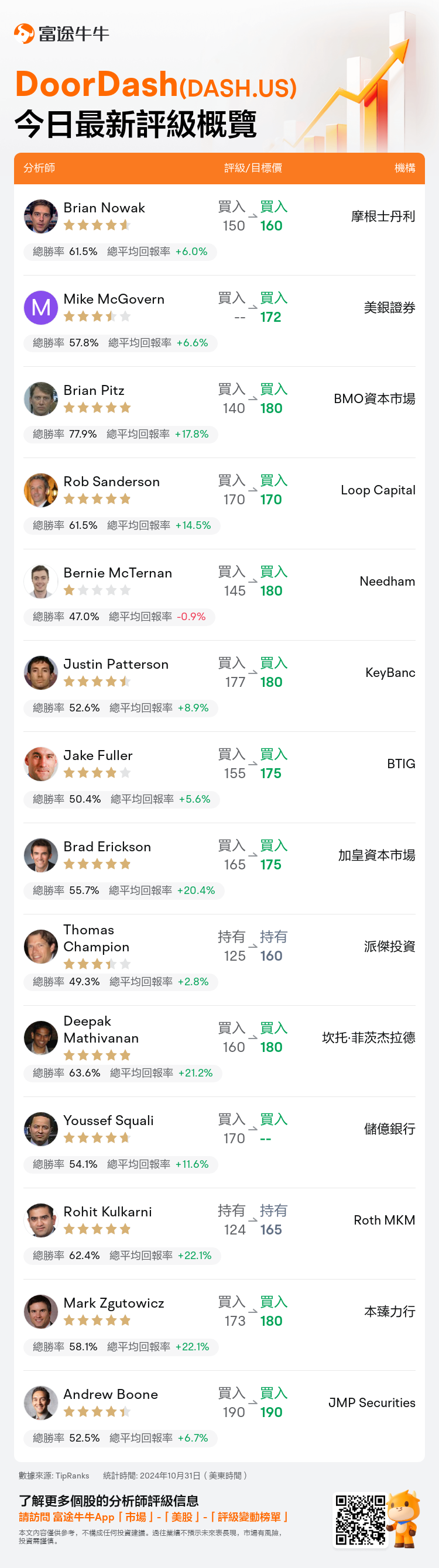

美東時間10月31日,多家華爾街大行更新了$DoorDash (DASH.US)$的評級,目標價介於160美元至190美元。

摩根士丹利分析師Brian Nowak維持買入評級,並將目標價從150美元上調至160美元。

美銀證券分析師Mike McGovern維持買入評級,目標價172美元。

BMO資本市場分析師Brian Pitz維持買入評級,並將目標價從140美元上調至180美元。

BMO資本市場分析師Brian Pitz維持買入評級,並將目標價從140美元上調至180美元。

Loop Capital分析師Rob Sanderson維持買入評級,維持目標價170美元。

Needham分析師Bernie McTernan維持買入評級,並將目標價從145美元上調至180美元。

此外,綜合報道,$DoorDash (DASH.US)$近期主要分析師觀點如下:

在一個實現營收預期但提供較少毛利增長的穩健季度之後,分析師們對doordash持積極態度。2025年的預測現在預計比以前預測的更高的毛訂單價值、營業收入和EBITDA。

doordash展示了強勁的第三季度EBITDA,預計第四季度將繼續強勁增長,得益於餐飲板塊持續擴張,在新垂直領域和國際市場的大幅增長,以及單位經濟的提升。

doordash的第三季度業績令人印象深刻,展示了強勁的毛訂單價值指引和略低於買入方預測的EBITDA。值得注意的是,公司持續的訂單增長受到訂單頻率上升、空前的客戶忠誠度推動,後者又得到新合作伙伴關係的進一步增強的支撐,毛利潤的增長暗示新興垂直領域的盈利影響減少,廣告營業收入的上升。

doordash報告了超出預期的第三季度毛訂單價值,並伴隨着EBITDA的改善。這些改進是由毛利率槓桿作用和降低的法律費用帶來的。此外,doordash取得了訂單頻率創紀錄的高水平,這可以歸因於產品種類的增加。

市場對季度盈利報告持有高期望,然而,doordash以強勁增長、增加的毛利率和最初的積極淨利潤表現出色。

以下爲今日14位分析師對$DoorDash (DASH.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。