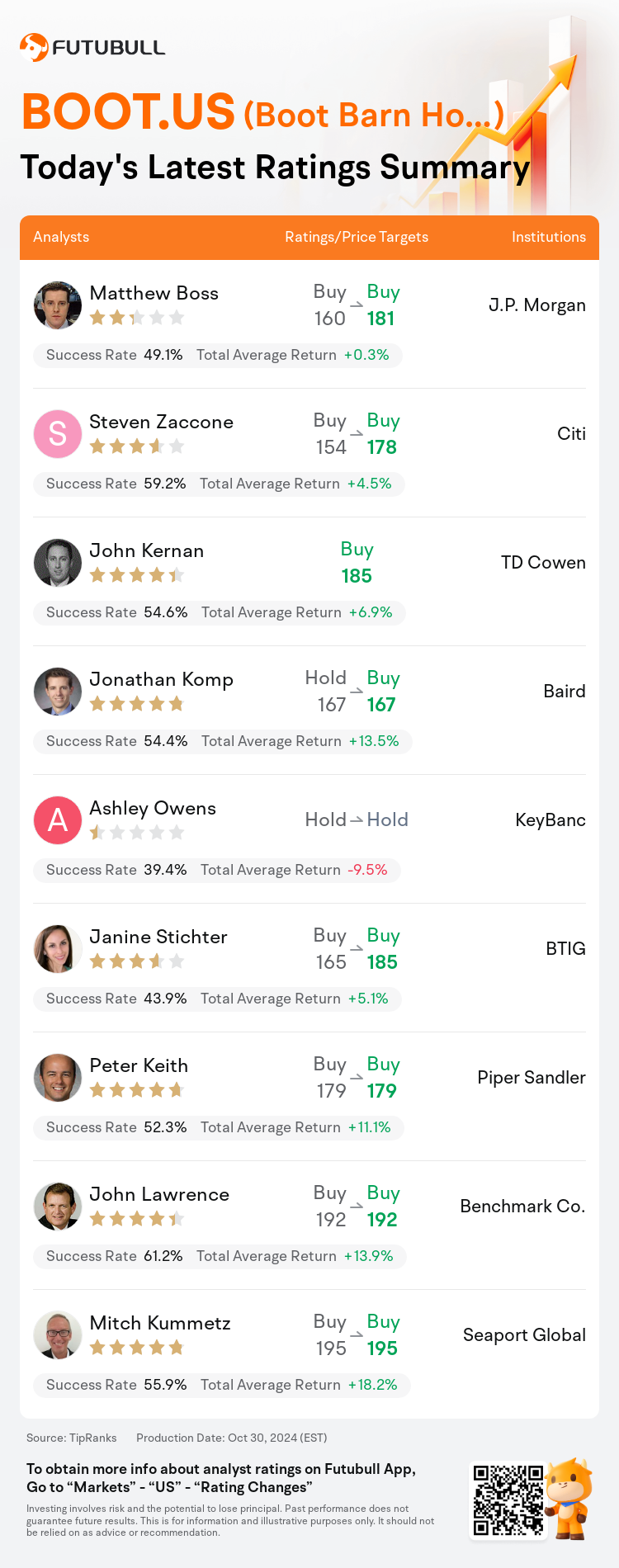

On Oct 30, major Wall Street analysts update their ratings for $Boot Barn Holdings (BOOT.US)$, with price targets ranging from $167 to $195.

J.P. Morgan analyst Matthew Boss maintains with a buy rating, and adjusts the target price from $160 to $181.

Citi analyst Steven Zaccone maintains with a buy rating, and adjusts the target price from $154 to $178.

TD Cowen analyst John Kernan initiates coverage with a buy rating, and sets the target price at $185.

TD Cowen analyst John Kernan initiates coverage with a buy rating, and sets the target price at $185.

Baird analyst Jonathan Komp upgrades to a buy rating, and maintains the target price at $167.

KeyBanc analyst Ashley Owens maintains with a hold rating.

Furthermore, according to the comprehensive report, the opinions of $Boot Barn Holdings (BOOT.US)$'s main analysts recently are as follows:

Boot Barn's recent fiscal Q2 report surpassed expectations, prompting a positive outlook. The report highlighted a notable increase in comparable sales, primarily driven by a surge in transaction growth. Additionally, the company's smooth executive transition is noted to be the result of a well-planned, multi-year succession strategy.

Boot Barn demonstrated robust fiscal Q2 same-store-sales performance surpassing Street forecasts. However, the earnings impact did not meet market expectations mainly because of elevated incentive compensation and unique legal expenditures. Analysts suggest that Boot Barn is regaining solid same-store-sales momentum, with its business model progressively approaching its 20% earnings growth trajectory.

The recent 20% decline in Boot Barn's stock price, believed to be partly due to the unexpected CEO transition among other minor concerns, is seen as presenting a more attractive risk/reward scenario. Confidence remains in the company's potential for favorable earnings growth, driven by significant opportunities for expansion. Additionally, with the valuation falling below the median of its peers, there appears to be a possibility for substantial upside within the next year, with limited further downside, supporting a positive outlook.

Boot Barn's second quarter showcased strong performance, aligning with projections following an optimistic update earlier in September. Notably, all product categories are experiencing positive trends, even those that previously lagged, such as women's western wear and work-related apparel. Furthermore, the company's e-commerce revenue has seen a positive shift for seven months consecutively, marking an end to a persistently negative trend and indicating an uptick in momentum during the second quarter.

Here are the latest investment ratings and price targets for $Boot Barn Holdings (BOOT.US)$ from 9 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

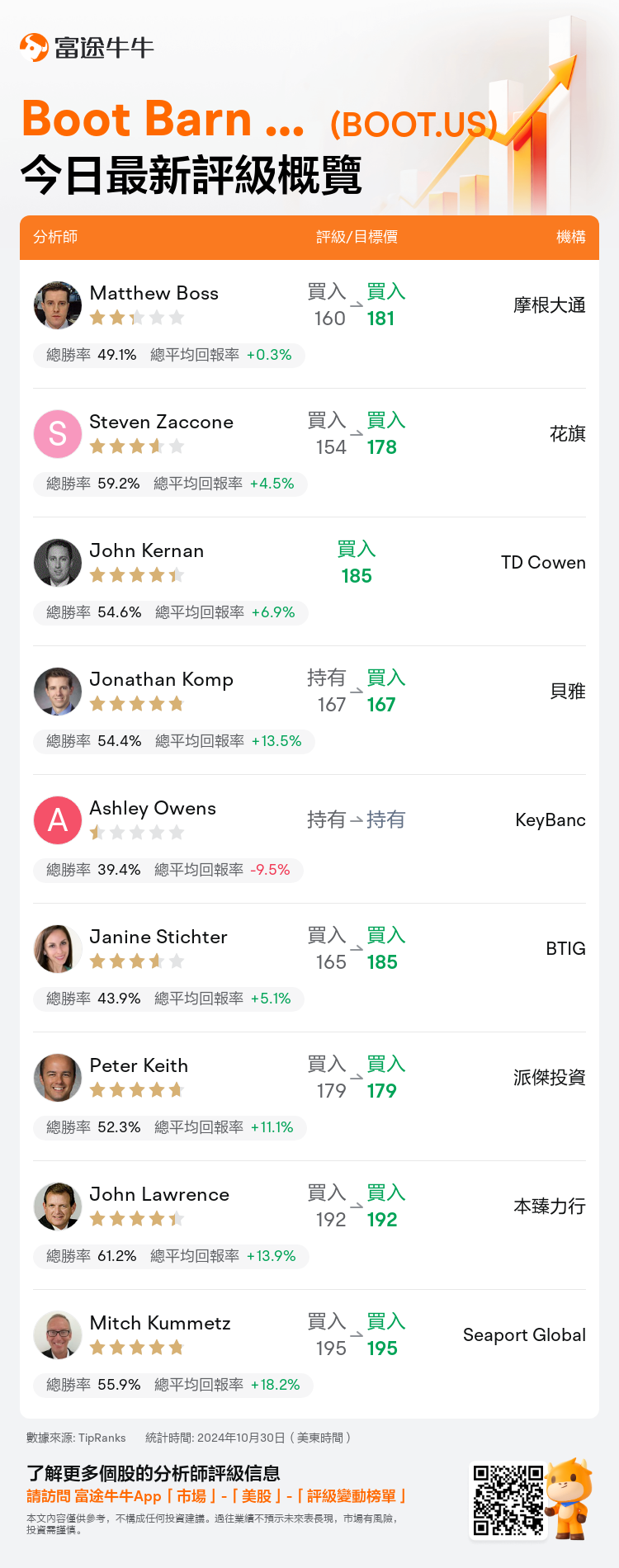

美東時間10月30日,多家華爾街大行更新了$Boot Barn Holdings (BOOT.US)$的評級,目標價介於167美元至195美元。

摩根大通分析師Matthew Boss維持買入評級,並將目標價從160美元上調至181美元。

花旗分析師Steven Zaccone維持買入評級,並將目標價從154美元上調至178美元。

TD Cowen分析師John Kernan首次給予買入評級,目標價185美元。

TD Cowen分析師John Kernan首次給予買入評級,目標價185美元。

貝雅分析師Jonathan Komp上調至買入評級,維持目標價167美元。

KeyBanc分析師Ashley Owens維持持有評級。

此外,綜合報道,$Boot Barn Holdings (BOOT.US)$近期主要分析師觀點如下:

Boot Barn最近的財季Q2報告超出預期,促使積極展望。報告突出了可比銷售額的顯著增長,主要受到交易增長的激增推動。此外,公司順利的高管過渡被認爲是一個經過精心策劃的、持續多年的繼任策略的結果。

Boot Barn展示了強勁的財季Q2同店銷售業績,超過了華爾街的預測。然而,由於激勵報酬和獨特的法律支出增加,收益影響未能達到市場預期。分析師們建議,Boot Barn正在重新獲得穩健的同店銷售增長勢頭,其商業模式逐漸接近20%的盈利增長軌道。

Boot Barn股價最近下跌20%,部分原因被認爲是由於意外的首席執行官過渡,以及其他較小的關注點,這被視爲呈現更具吸引力的風險/回報情景。對公司潛在獲得有利盈利增長的信心仍然存在,這受益於擴張的重大機會。此外,伴隨估值低於同行中位數,明年內存在相當大的上升可能性,並且下行空間有限,支持積極展望。

Boot Barn第二季度展示出強勁業績,與9月初的樂觀更新相符。值得注意的是,所有產品類別都呈現出積極的趨勢,甚至那些過去落後的類別,如女性西部服裝和勞動相關服裝。此外,公司的電子商務營業收入連續七個月呈現積極變化,標誌着持續下跌趨勢的結束,並表明在第二季度勢頭有所上揚。

以下爲今日9位分析師對$Boot Barn Holdings (BOOT.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。