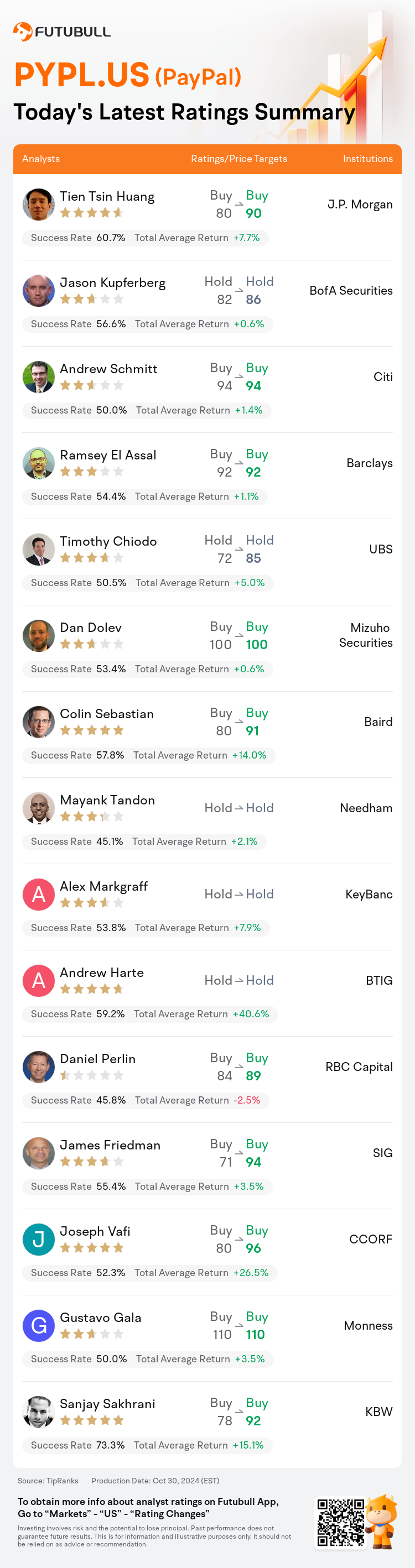

On Oct 30, major Wall Street analysts update their ratings for $PayPal (PYPL.US)$, with price targets ranging from $85 to $110.

J.P. Morgan analyst Tien Tsin Huang maintains with a buy rating, and adjusts the target price from $80 to $90.

BofA Securities analyst Jason Kupferberg maintains with a hold rating, and adjusts the target price from $82 to $86.

Citi analyst Andrew Schmitt maintains with a buy rating, and maintains the target price at $94.

Citi analyst Andrew Schmitt maintains with a buy rating, and maintains the target price at $94.

Barclays analyst Ramsey El Assal maintains with a buy rating, and maintains the target price at $92.

UBS analyst Timothy Chiodo maintains with a hold rating, and adjusts the target price from $72 to $85.

Furthermore, according to the comprehensive report, the opinions of $PayPal (PYPL.US)$'s main analysts recently are as follows:

PayPal's consistent performance post Q3 announcement is noted, despite prior stock appreciation, denser market positioning, and high anticipations. Looking ahead to 2024, which is anticipated to be a pivot year, current valuation and market sentiment are believed to provide a buffer against potential declines.

PayPal's updated FY24 guidance, accompanied by stable mid-single digit growth in Branded Checkout, has instilled a moderately increased confidence in the company's primary gross profit catalyst moving forward. Additionally, there are preliminary anticipations for growth in transaction margin dollars in 2025.

PayPal is positioned to achieve steady mid-single digit gross profit growth with a sustainable high-single to low-double digit growth in earnings per share. However, initiatives to enhance Branded growth, increase Pay with Venom utilization, and develop Fastlane are anticipated to necessitate a prolonged period of patience, potentially until late 2025 to 2026.

Following the Q3 report, the market's reaction to PayPal shares, which closed down 4%, is considered a positive sign given the stock's recent robust performance. This comes as investors weigh the company's performance which surpassed consensus expectations on key transaction margin dollars and adjusted earnings, leading to an improved forecast for FY24. Analysts note that while the financial expectations for fiscal 2025 appear to be well-positioned, the demands for operational excellence are increasing.

Following PayPal's third-quarter earnings surpassing expectations, there was an observed acceleration in the growth of the company's transaction margin dollars. Despite the anticipation of a near-term deceleration in growth as a result of diminishing gains from interest income, the guidance provided by management for the fourth quarter is perceived as unduly cautious.

Here are the latest investment ratings and price targets for $PayPal (PYPL.US)$ from 15 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

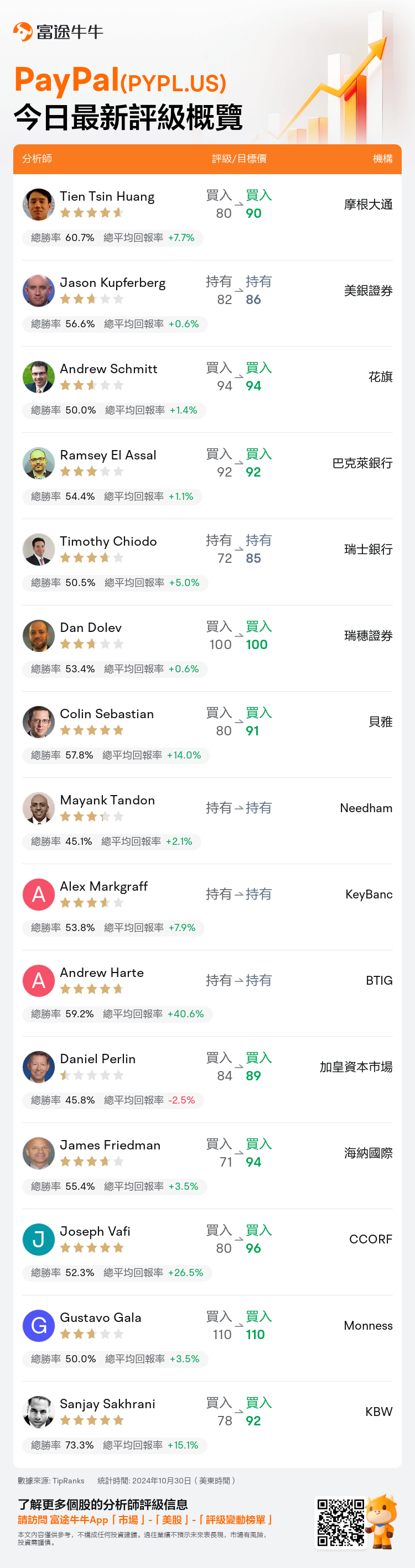

美東時間10月30日,多家華爾街大行更新了$PayPal (PYPL.US)$的評級,目標價介於85美元至110美元。

摩根大通分析師Tien Tsin Huang維持買入評級,並將目標價從80美元上調至90美元。

美銀證券分析師Jason Kupferberg維持持有評級,並將目標價從82美元上調至86美元。

花旗分析師Andrew Schmitt維持買入評級,維持目標價94美元。

花旗分析師Andrew Schmitt維持買入評級,維持目標價94美元。

巴克萊銀行分析師Ramsey El Assal維持買入評級,維持目標價92美元。

瑞士銀行分析師Timothy Chiodo維持持有評級,並將目標價從72美元上調至85美元。

此外,綜合報道,$PayPal (PYPL.US)$近期主要分析師觀點如下:

paypal在Q3公告後表現穩定,儘管之前股價上漲,市場定位更密集,預期較高。展望2024年,預計將是一個轉折年,當前估值和市場情緒被認爲能夠對潛在下降提供保護。

paypal更新了FY24指引,伴隨着Branded Checkout穩定的中單位數增長,加強了人們對公司主要毛利潤催化劑未來發展的信心。此外,2025年交易邊際美元增長的初步預期。

paypal定位爲實現毛利潤穩定增長的中單位數,每股收益可持續增長高單位數至低兩位數。然而,增強Branded增長、增加Pay with Venom利用率和開發Fastlane的舉措預計需要長期耐心,可能要等到2025年末至2026年。

在Q3報告後,paypal股票收盤下跌4%,市場對此表示肯定,考慮到該股最近的強勁表現。這是因爲投資者正在權衡公司的表現,超出了對關鍵交易邊際美元和調整後收益的一致預期,導致FY24預測改善。分析師指出,儘管2025財年的財務預期似乎處在一個良好位置,對運營卓越的需求正在增加。

隨着paypal第三季度盈利超過預期,公司交易邊際美元增長加速。儘管由於利息收入減少導致未來增長近期放緩的預期,管理層提供的第四季度指引被認爲過於謹慎。

以下爲今日15位分析師對$PayPal (PYPL.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。