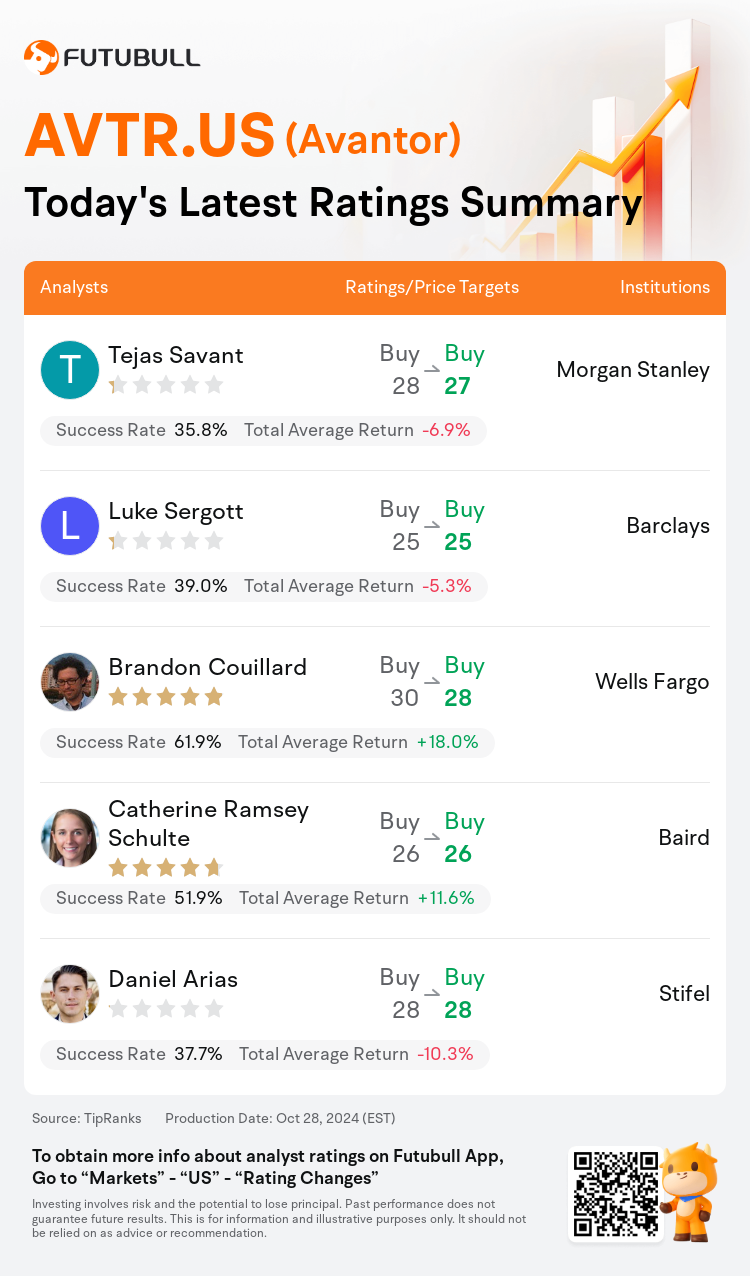

On Oct 28, major Wall Street analysts update their ratings for $Avantor (AVTR.US)$, with price targets ranging from $25 to $28.

Morgan Stanley analyst Tejas Savant maintains with a buy rating, and adjusts the target price from $28 to $27.

Barclays analyst Luke Sergott maintains with a buy rating, and maintains the target price at $25.

Wells Fargo analyst Brandon Couillard maintains with a buy rating, and adjusts the target price from $30 to $28.

Wells Fargo analyst Brandon Couillard maintains with a buy rating, and adjusts the target price from $30 to $28.

Baird analyst Catherine Ramsey Schulte maintains with a buy rating, and maintains the target price at $26.

Stifel analyst Daniel Arias maintains with a buy rating, and maintains the target price at $28.

Furthermore, according to the comprehensive report, the opinions of $Avantor (AVTR.US)$'s main analysts recently are as follows:

Avantor experienced a return to growth in LSS and Bioprocessing recovery, which was balanced out by weakness in U.S. semiconductor performance, according to an analysis shared with investors following the company's earnings release.

The firm expressed satisfaction with Avantor's robust free cash flow generation during the quarter and the gradual uptick in bioprocessing and equipment & instrumentation revenue, which surpassed expectations. Although management has not offered projections for 2025, the expectation is for a consistent, gradual enhancement throughout the fiscal year.

The softness in the semiconductor segment is overshadowing what is otherwise considered a 'solid' revenue outcome. Attention remains fixated on the EBITDA margin shortfall, casting doubts on the prospect of achieving a 20% EBITDA margin by the year 2025. It is anticipated that the company will approach this target, but it will necessitate a favorable product mix and additional cost reductions to attain it. Expectations for growth have been moderated to 3%, taking into account the semiconductor situation and margin outlook for 2025.

The firm indicated that Avantor's third quarter performance surpassed expectations, despite a notable weakness in the Semiconductor segment. The Bioprocess area showed strong results, while the Laboratory division experienced a modest improvement alongside robust cost management and Free Cash Flow generation.

Avantor's $12M revenue shortfall, primarily due to decreased sales in applied markets, was somewhat mitigated by stronger results in Lab Solutions and bioprocessing segments. Despite the revenue miss, there's a positive outlook on the stock's performance during downturns and confidence in the company's ability to meet its FY25 financial targets.

Here are the latest investment ratings and price targets for $Avantor (AVTR.US)$ from 5 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

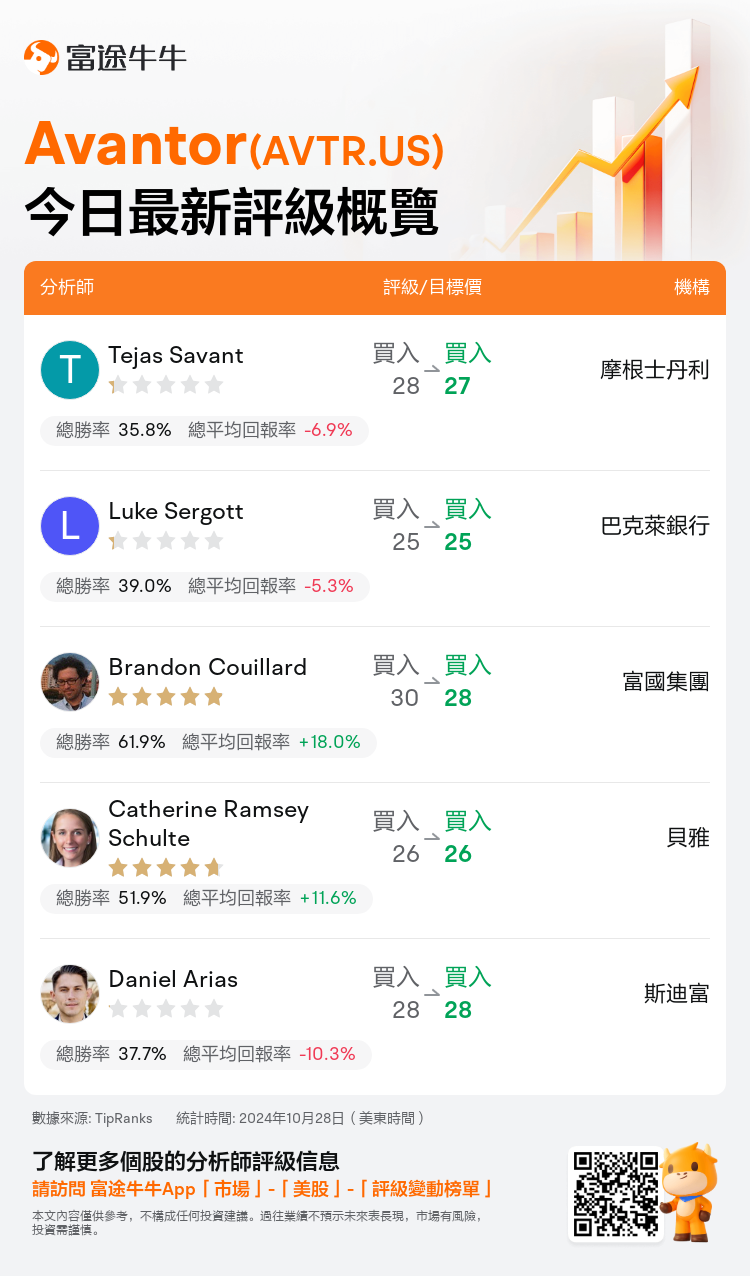

美東時間10月28日,多家華爾街大行更新了$Avantor (AVTR.US)$的評級,目標價介於25美元至28美元。

摩根士丹利分析師Tejas Savant維持買入評級,並將目標價從28美元下調至27美元。

巴克萊銀行分析師Luke Sergott維持買入評級,維持目標價25美元。

富國集團分析師Brandon Couillard維持買入評級,並將目標價從30美元下調至28美元。

富國集團分析師Brandon Couillard維持買入評級,並將目標價從30美元下調至28美元。

貝雅分析師Catherine Ramsey Schulte維持買入評級,維持目標價26美元。

斯迪富分析師Daniel Arias維持買入評級,維持目標價28美元。

此外,綜合報道,$Avantor (AVTR.US)$近期主要分析師觀點如下:

avantor的長短期服務與生物加工領域的增長恢復,抵消了美國半導體表現的疲軟,根據向投資者分享的分析,該分析是在公司發佈收益後進行的。

公司對avantor在本季度強勁的自由現金流生成以及生物加工和設備與儀器營業收入逐漸回升表示滿意,這超出了預期。儘管管理層未提供2025年的預測,但預期在財政年度內會實現一致、逐步的增長。

半導體板塊的疲軟現象正掩蓋了其他方面被認爲是『穩健』的營業收入結果。人們仍然關注EBITDA利潤率的不足,對2025年實現20%的EBITDA利潤率的前景表示懷疑。預計公司將實現這一目標,但這將需要一個有利的產品組合和額外的成本削減才能實現。對於增長的預期已經下調至3%,考慮到2025年的半導體情況和利潤前景。

公司表示,儘管半導體板塊存在明顯的疲軟現象,但avantor的第三季度表現超出了預期。生物工藝領域取得了強勁的業績,而實驗室部門在強勁的成本管理和自由現金流生成的同時出現了適度改善。

avantor的1200萬美元營業收入不足主要是由於應用市場銷售額下降,而在實驗室解決方案和生物加工領域取得了較好的成績,這在一定程度上有所緩解。儘管營業收入不達預期,對於股票在市場低迷時表現的看法還是積極的,對公司能夠實現2025財年財務目標充滿信心。

以下爲今日5位分析師對$Avantor (AVTR.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。