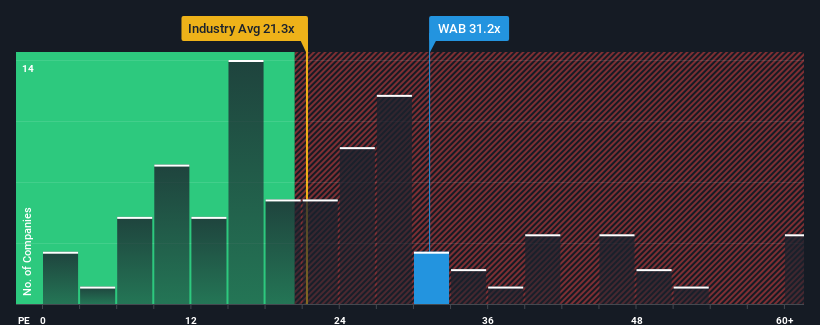

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 17x, you may consider Westinghouse Air Brake Technologies Corporation (NYSE:WAB) as a stock to avoid entirely with its 31.2x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Recent times have been pleasing for Westinghouse Air Brake Technologies as its earnings have risen in spite of the market's earnings going into reverse. It seems that many are expecting the company to continue defying the broader market adversity, which has increased investors' willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:WAB Price to Earnings Ratio vs Industry October 28th 2024 Want the full picture on analyst estimates for the company? Then our free report on Westinghouse Air Brake Technologies will help you uncover what's on the horizon.

Is There Enough Growth For Westinghouse Air Brake Technologies?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Westinghouse Air Brake Technologies' to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 43%. Pleasingly, EPS has also lifted 150% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the eleven analysts covering the company suggest earnings should grow by 19% over the next year. With the market only predicted to deliver 15%, the company is positioned for a stronger earnings result.

In light of this, it's understandable that Westinghouse Air Brake Technologies' P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Westinghouse Air Brake Technologies maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

Plus, you should also learn about this 1 warning sign we've spotted with Westinghouse Air Brake Technologies.

Of course, you might also be able to find a better stock than Westinghouse Air Brake Technologies. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of earnings growth, the company posted a terrific increase of 43%. Pleasingly, EPS has also lifted 150% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

If we review the last year of earnings growth, the company posted a terrific increase of 43%. Pleasingly, EPS has also lifted 150% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

如果我們回顧去年的收益增長,公司實現了驚人的增長達43%。令人高興的是,每股收益從三年前開始已經累計增長了150%,這要歸功於過去12個月的增長。因此,我們可以開始確認公司在這段時間內增長收益做得非常好。

如果我們回顧去年的收益增長,公司實現了驚人的增長達43%。令人高興的是,每股收益從三年前開始已經累計增長了150%,這要歸功於過去12個月的增長。因此,我們可以開始確認公司在這段時間內增長收益做得非常好。