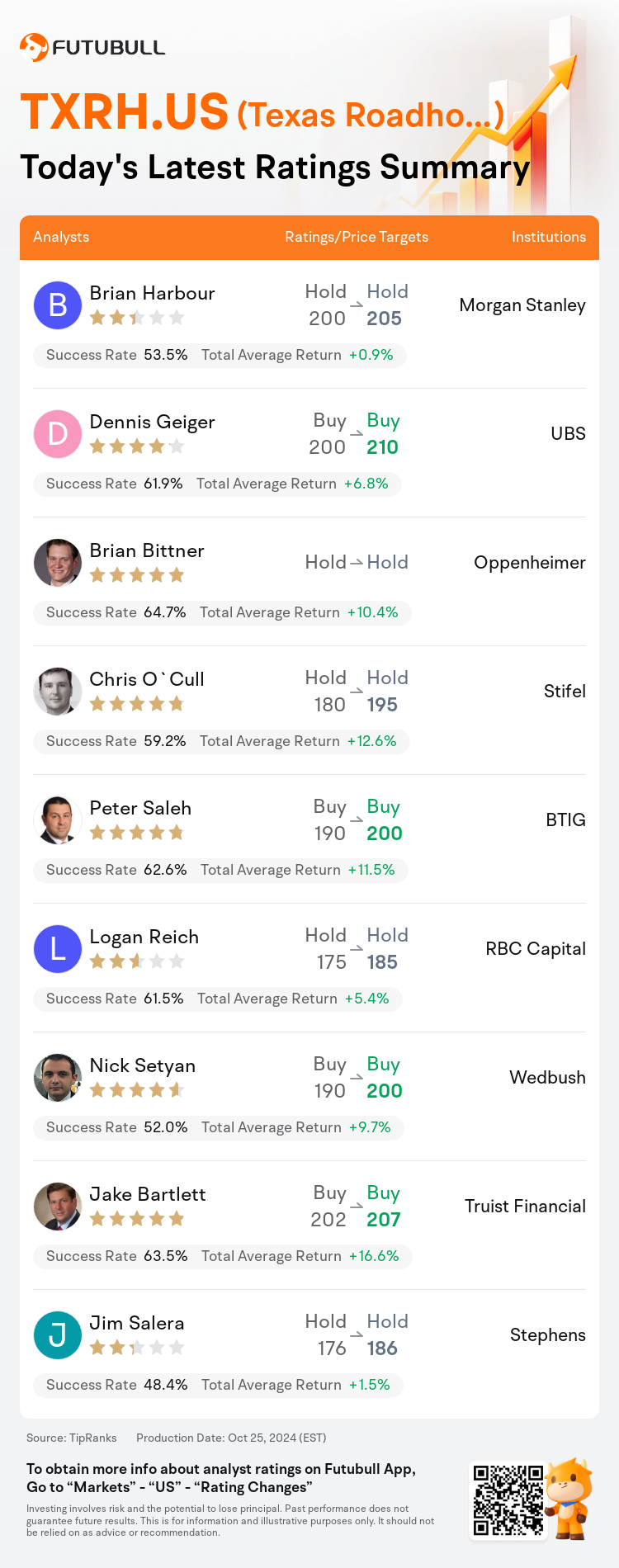

On Oct 25, major Wall Street analysts update their ratings for $Texas Roadhouse (TXRH.US)$, with price targets ranging from $185 to $210.

Morgan Stanley analyst Brian Harbour maintains with a hold rating, and adjusts the target price from $200 to $205.

UBS analyst Dennis Geiger maintains with a buy rating, and adjusts the target price from $200 to $210.

Oppenheimer analyst Brian Bittner maintains with a hold rating.

Oppenheimer analyst Brian Bittner maintains with a hold rating.

Stifel analyst Chris O`Cull maintains with a hold rating, and adjusts the target price from $180 to $195.

BTIG analyst Peter Saleh maintains with a buy rating, and adjusts the target price from $190 to $200.

Furthermore, according to the comprehensive report, the opinions of $Texas Roadhouse (TXRH.US)$'s main analysts recently are as follows:

Texas Roadhouse posted a robust performance for the quarter, which, while not significantly surpassing expectations, has led to a slight increase in projections that remain higher than the consensus.

The company's Q3 performance was robust, despite a shortfall in earnings attributed to challenges with labor and taxes.

Texas Roadhouse's third-quarter results showcased continued strong same-store sales momentum and restaurant margin expansion. The guidance for 2025 on commodities was more favorable than many expected. There is optimism surrounding the significant traffic increases and the acceleration in trends quarter-to-date, in spite of challenging economic conditions and increasingly tough comparisons. It is believed that the company's leading traffic momentum, potential for multiyear earnings growth, and the prospect of returning to sustainable margins of 17%-18% underpin the possibility for upside.

Texas Roadhouse has maintained strong momentum through the quarter, with an acceleration in comparable store sales and an approximately 100 basis point increase in traffic into October. Additionally, the company has seen labor productivity enhancements, with both labor hour growth and traffic growth below 30% in the third quarter, thereby driving leverage.

The company's Q3 earnings did not meet expectations, influenced by higher depreciation, amortization, taxes, and insurance adjustments. Recognition of the company's commendable comparable growth amidst a difficult market condition is noted. However, it is cautioned that the stock's valuation multiple is considered high and that the consensus EPS forecast for 2025 may be overly optimistic.

Here are the latest investment ratings and price targets for $Texas Roadhouse (TXRH.US)$ from 9 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

美東時間10月25日,多家華爾街大行更新了$德州公路酒吧 (TXRH.US)$的評級,目標價介於185美元至210美元。

摩根士丹利分析師Brian Harbour維持持有評級,並將目標價從200美元上調至205美元。

瑞士銀行分析師Dennis Geiger維持買入評級,並將目標價從200美元上調至210美元。

奧本海默控股分析師Brian Bittner維持持有評級。

奧本海默控股分析師Brian Bittner維持持有評級。

斯迪富分析師Chris O`Cull維持持有評級,並將目標價從180美元上調至195美元。

BTIG分析師Peter Saleh維持買入評級,並將目標價從190美元上調至200美元。

此外,綜合報道,$德州公路酒吧 (TXRH.US)$近期主要分析師觀點如下:

在這個季度,德州公路酒吧表現強勁,雖然沒有顯着超過預期,但已導致略微增加的預測,仍高於共識。

儘管由於勞工和稅收方面的挑戰而導致收益不足,但該公司的第三季度表現強勁。

德州公路酒吧第三季度的業績展示了持續強勁的同店銷售動力和餐廳利潤率增長。2025年關於商品的指引比許多人預期更有利。儘管經濟條件困難,比較日益嚴峻,但人們對於顯著的訪問量增加和季度至今趨勢加速感到樂觀。據信,公司領先的訪問量增長動能、多年收益增長的潛力以及恢復至17%-18%可持續利潤率的可能性支撐着上升的可能性。

德州公路酒吧通過這個季度保持着強勁的動力,同店銷售量加速增長,交通量在10月份增長了約100個點子。此外,該公司看到了勞動生產力的提高,第三季度勞動時間增長和交通增長均低於30%,從而推動了槓桿效應。

公司的第三季度收益沒有達到預期,受到折舊、攤銷、稅收和保險調整的影響。儘管認可了公司在困難的市場條件下可比增長的良好表現。然而,需要提醒的是,該股票的估值倍數被認爲較高,並且2025年的共識每股收益預測可能過於樂觀。

以下爲今日9位分析師對$德州公路酒吧 (TXRH.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。