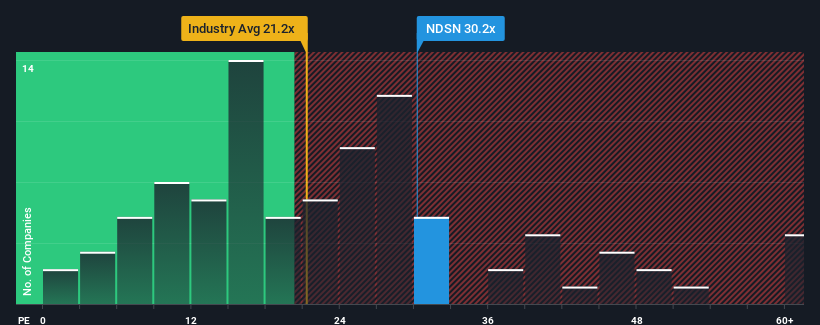

With a price-to-earnings (or "P/E") ratio of 30.2x Nordson Corporation (NASDAQ:NDSN) may be sending very bearish signals at the moment, given that almost half of all companies in the United States have P/E ratios under 18x and even P/E's lower than 10x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

With earnings that are retreating more than the market's of late, Nordson has been very sluggish. It might be that many expect the dismal earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be very nervous about the viability of the share price.

NasdaqGS:NDSN Price to Earnings Ratio vs Industry October 24th 2024 Keen to find out how analysts think Nordson's future stacks up against the industry? In that case, our free report is a great place to start.

Is There Enough Growth For Nordson?

The only time you'd be truly comfortable seeing a P/E as steep as Nordson's is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered a frustrating 5.6% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 32% overall rise in EPS, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Looking ahead now, EPS is anticipated to climb by 14% per annum during the coming three years according to the nine analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 10% per annum, which is noticeably less attractive.

With this information, we can see why Nordson is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Nordson maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 1 warning sign for Nordson that you should be aware of.

Of course, you might also be able to find a better stock than Nordson. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered a frustrating 5.6% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 32% overall rise in EPS, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Retrospectively, the last year delivered a frustrating 5.6% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 32% overall rise in EPS, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

回顧來看,去年公司的底線出現了令人沮喪的5.6%下降。儘管短期表現令人不滿,但最近三年的整體EPS增長率達到了出色的32%。雖然曲折,但可以說公司最近的收益增長已經足夠了。

回顧來看,去年公司的底線出現了令人沮喪的5.6%下降。儘管短期表現令人不滿,但最近三年的整體EPS增長率達到了出色的32%。雖然曲折,但可以說公司最近的收益增長已經足夠了。