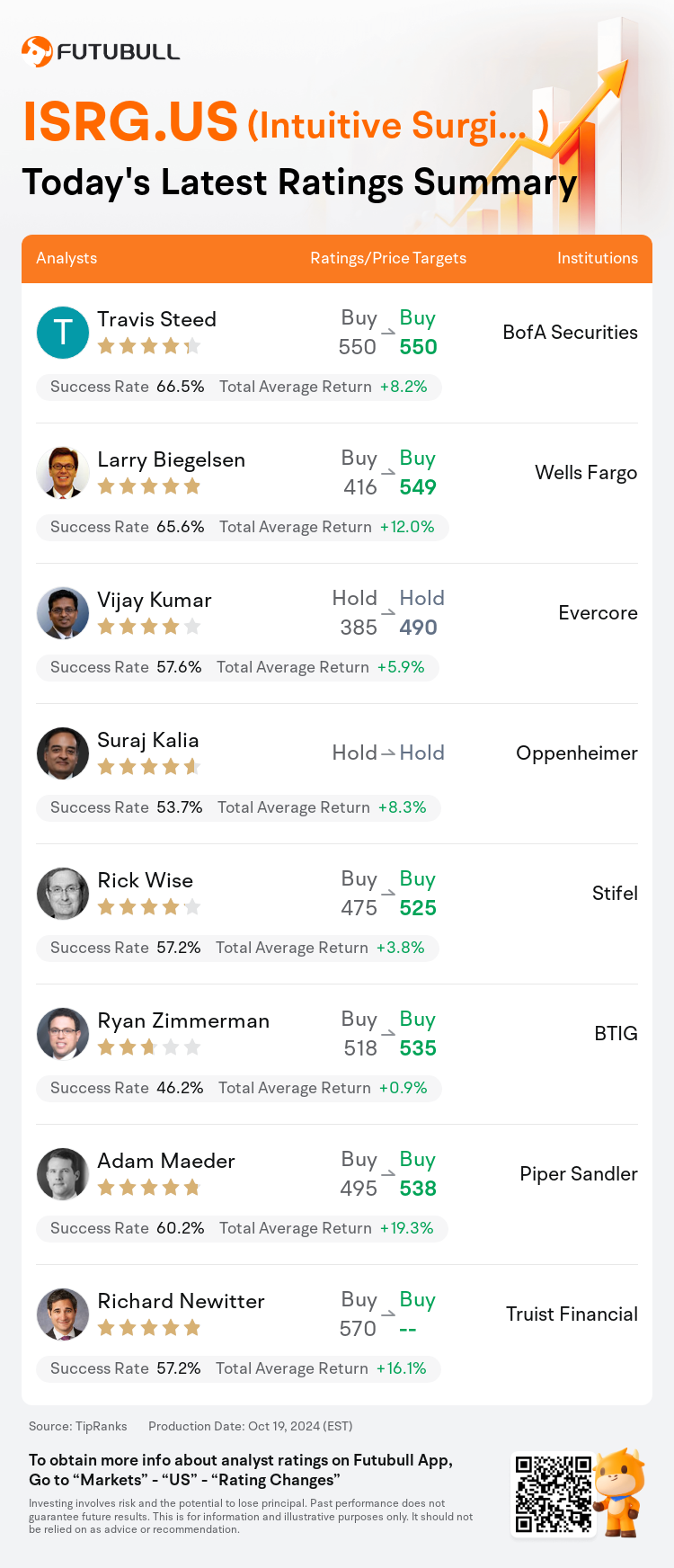

On Oct 19, major Wall Street analysts update their ratings for $Intuitive Surgical (ISRG.US)$, with price targets ranging from $490 to $550.

BofA Securities analyst Travis Steed maintains with a buy rating, and maintains the target price at $550.

Wells Fargo analyst Larry Biegelsen maintains with a buy rating, and adjusts the target price from $416 to $549.

Evercore analyst Vijay Kumar maintains with a hold rating, and adjusts the target price from $385 to $490.

Evercore analyst Vijay Kumar maintains with a hold rating, and adjusts the target price from $385 to $490.

Oppenheimer analyst Suraj Kalia maintains with a hold rating.

Stifel analyst Rick Wise maintains with a buy rating, and adjusts the target price from $475 to $525.

Furthermore, according to the comprehensive report, the opinions of $Intuitive Surgical (ISRG.US)$'s main analysts recently are as follows:

The company's Q3 earnings surpassed expectations, characterized by a 'strong quarter' with significant placements of the Da Vinci 5 system, a surge in procedure volumes, and maintained margin discipline. Additionally, the company's management has revised its FY24 procedure volume growth forecast to a range of 16%-17%, from the previously estimated 15.5%-17%. This adjustment takes into account the potential for a continued decline in bariatric procedures and growing challenges in Asia, such as extended physician strikes in Korea, while also considering a scenario where bariatric procedures stabilize at current rates and the situation in Korea and China does not deteriorate further.

The projection for Intuitive Surgical's revenue outperformance in FY25 appears to be reflected in current market expectations. Following the company's quarterly financial disclosure, it's indicated that the estimate for FY25 earnings per share has been adjusted upward by approximately 3%.

Intuitive Surgical reported robust third-quarter results, outperforming expectations in two crucial aspects - placements of their DV5 systems and growth in procedures. The company is witnessing significant growth momentum following the U.S. approval of the da Vinci 5 system. The early adoption of DV5 is progressing faster than the previous fourth-generation system's launch, with promising signs of potential growth acceleration in the coming years.

The company's Q3 earnings and revenue surpassed expectations, alongside an 18% increase in procedure volume, which also exceeded the consensus forecast by 100 basis points. The expectation is for the growth momentum to persist, especially with the widening array of regulatory clearances for Dv5, anticipating sustained expansion into the latter part of FY25.

The firm has once again raised their expectations, reinforcing their belief in the ongoing potential for growth which supports the company's high valuation. The company is seen as a top-tier long-term growth pick following its performance that surpassed estimates and showed growth acceleration on almost all fronts.

Here are the latest investment ratings and price targets for $Intuitive Surgical (ISRG.US)$ from 8 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

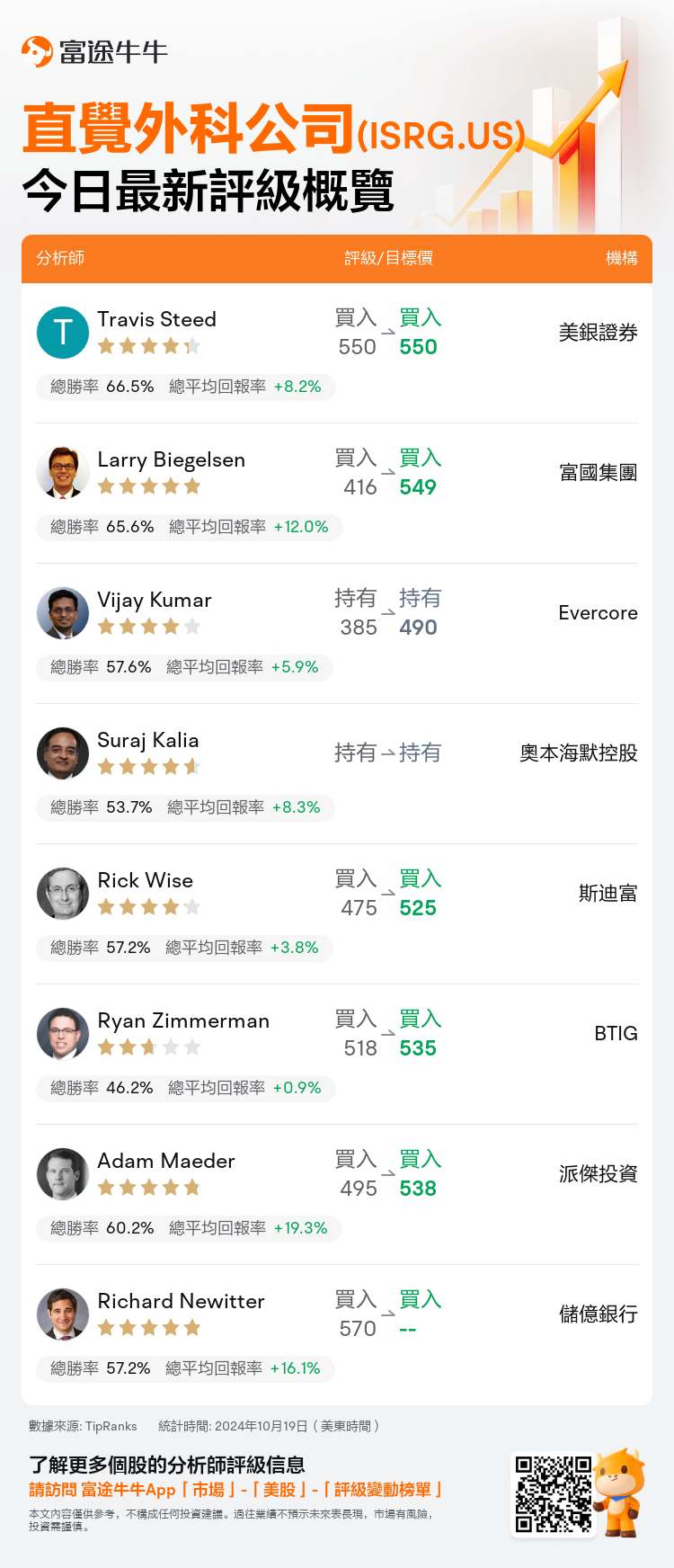

美東時間10月19日,多家華爾街大行更新了$直覺外科公司 (ISRG.US)$的評級,目標價介於490美元至550美元。

美銀證券分析師Travis Steed維持買入評級,維持目標價550美元。

富國集團分析師Larry Biegelsen維持買入評級,並將目標價從416美元上調至549美元。

Evercore分析師Vijay Kumar維持持有評級,並將目標價從385美元上調至490美元。

Evercore分析師Vijay Kumar維持持有評級,並將目標價從385美元上調至490美元。

奧本海默控股分析師Suraj Kalia維持持有評級。

斯迪富分析師Rick Wise維持買入評級,並將目標價從475美元上調至525美元。

此外,綜合報道,$直覺外科公司 (ISRG.US)$近期主要分析師觀點如下:

公司的第三季度收入超出預期,表現爲「強勁季度」,達芬奇5系統的安置數量顯著增加,程序量激增,保持利潤率紀律。此外,公司管理層已將FY24程序量增長預測修訂爲16%-17%的區間,而之前估計爲15.5%-17%。該調整考慮了手術量可能持續下降以及亞洲日益嚴峻的挑戰,如韓國醫生長期罷工,同時還考慮了一種情形,在這種情況下,減重手術量在當前水平穩定,韓國和中國的局勢不會進一步惡化。

在FY25,直覺外科公司營收表現超預期的預測似乎已經反映在當前市場預期中。在公司季度財務披露之後,指出FY25每股收益估計已上調約3%。

直覺外科公司報告了強勁的第三季度業績,兩個關鍵方面超出預期—他們DV5系統的安置以及程序增長。公司正在經歷顯著的增長勢頭,隨着達芬奇5系統在美國獲批准。DV5的早期採用速度比上一代系統的推出更快,顯示出未來幾年潛在增長加速的跡象。

公司的第三季度收入和營業收入超出預期,手術量增長18%,也比共識預測高出100個點子。預期增長勢頭將持續,尤其是隨着DV5獲得更多監管批准,預期持續擴張至FY25後期。

該公司再次提高了他們的期望,鞏固了他們對持續增長潛力的信心,這支持了公司的高估值。該公司被視爲頂級長期增長選擇,因爲其表現超出預期,並在幾乎所有方面顯示出增長加速。

以下爲今日8位分析師對$直覺外科公司 (ISRG.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。