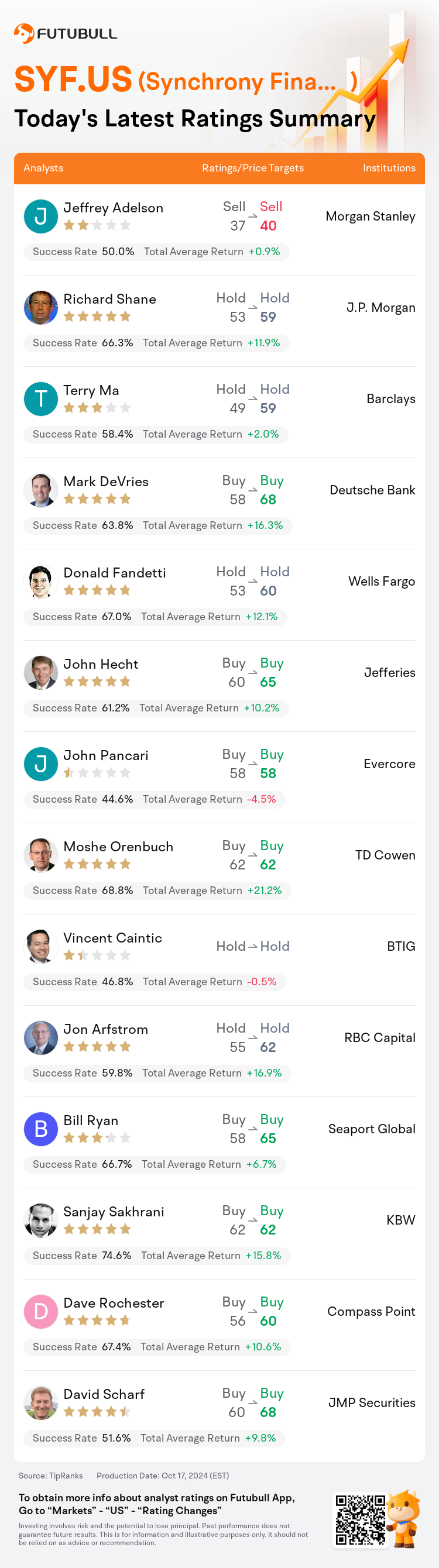

On Oct 17, major Wall Street analysts update their ratings for $Synchrony Financial (SYF.US)$, with price targets ranging from $40 to $68.

Morgan Stanley analyst Jeffrey Adelson maintains with a sell rating, and adjusts the target price from $37 to $40.

J.P. Morgan analyst Richard Shane maintains with a hold rating, and adjusts the target price from $53 to $59.

Barclays analyst Terry Ma maintains with a hold rating, and adjusts the target price from $49 to $59.

Barclays analyst Terry Ma maintains with a hold rating, and adjusts the target price from $49 to $59.

Deutsche Bank analyst Mark DeVries maintains with a buy rating, and adjusts the target price from $58 to $68.

Wells Fargo analyst Donald Fandetti maintains with a hold rating, and adjusts the target price from $53 to $60.

Furthermore, according to the comprehensive report, the opinions of $Synchrony Financial (SYF.US)$'s main analysts recently are as follows:

Synchrony delivered a strong EPS showing, and the narrative regarding delinquency stabilization persists. Despite these factors, the outlook remains cautious due to potential risks including the imposition of a late fee cap, credit expectations, and a forecasted deceleration in spending growth by 2025.

Post the Q3 report, the mitigant impact and credit were key areas of focus, with the view that Synchrony demonstrated sufficient progress in both areas to alleviate any concerns.

Synchrony's third-quarter outcomes displayed ongoing advancements in credit stabilization and compensation for lost late fees. This progress persists despite the evolving landscape of litigation and political events, which now suggest that the anticipated impact on late fee revenue might be less probable.

The third-quarter earnings per share (EPS) of $1.94 surpassed market expectations, bolstered by robust net interest income and margins. It has been highlighted that the company's updated earnings guidance for FY24, which excludes the Pets Best gain, is based on the assumption that there will be no late fee regulation in 2024. This is a shift from earlier projections that included an October 1 implementation forecast.

The company's Q3 earnings surpassed expectations, demonstrating solid fundamentals with core performance aligning with projections. Credit trends at the company are showing signs of stabilization, and the return to normal growth is indicative of the firm's commitment to credit discipline amidst the current economic conditions.

Here are the latest investment ratings and price targets for $Synchrony Financial (SYF.US)$ from 14 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

美東時間10月17日,多家華爾街大行更新了$Synchrony Financial (SYF.US)$的評級,目標價介於40美元至68美元。

摩根士丹利分析師Jeffrey Adelson維持賣出評級,並將目標價從37美元上調至40美元。

摩根大通分析師Richard Shane維持持有評級,並將目標價從53美元上調至59美元。

巴克萊銀行分析師Terry Ma維持持有評級,並將目標價從49美元上調至59美元。

巴克萊銀行分析師Terry Ma維持持有評級,並將目標價從49美元上調至59美元。

德意志銀行分析師Mark DeVries維持買入評級,並將目標價從58美元上調至68美元。

富國集團分析師Donald Fandetti維持持有評級,並將目標價從53美元上調至60美元。

此外,綜合報道,$Synchrony Financial (SYF.US)$近期主要分析師觀點如下:

Synchrony展示出了強勁的每股收益,關於拖欠穩定性的敘述依然持續。儘管存在這些因素,由於潛在風險,包括晚付費上限的設定、信用預期以及到2025年支出增長放緩的預測,展望仍然謹慎。

發帖Q3報告後,緩解影響和信用是關注的重點領域,認爲Synchrony在這兩個領域都取得了足夠的進展以消除任何擔憂。

Synchrony第三季度業績顯示了信用穩定和補償失去的晚付費持續推進。儘管訴訟和政治事件不斷髮展,但這一進展表明,晚付費收入預期的影響可能較不可能。

第三季度每股收益爲1.94美元,超過了市場預期,得益於強勁的淨利息收入和利潤率。公司針對FY24更新的盈利指引排除了Pets Best收益,這是基於假設2024年不會出台晚付費規定。這與早前預測有所不同,當時包括了10月1日的實施預測。

公司的Q3盈利超出預期,展示了核心業績與預期一致的堅實基本面。公司的信貸趨勢顯示出穩定跡象,恢復正常增長表明公司在當前經濟環境下堅守信貸紀律的承諾。

以下爲今日14位分析師對$Synchrony Financial (SYF.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。