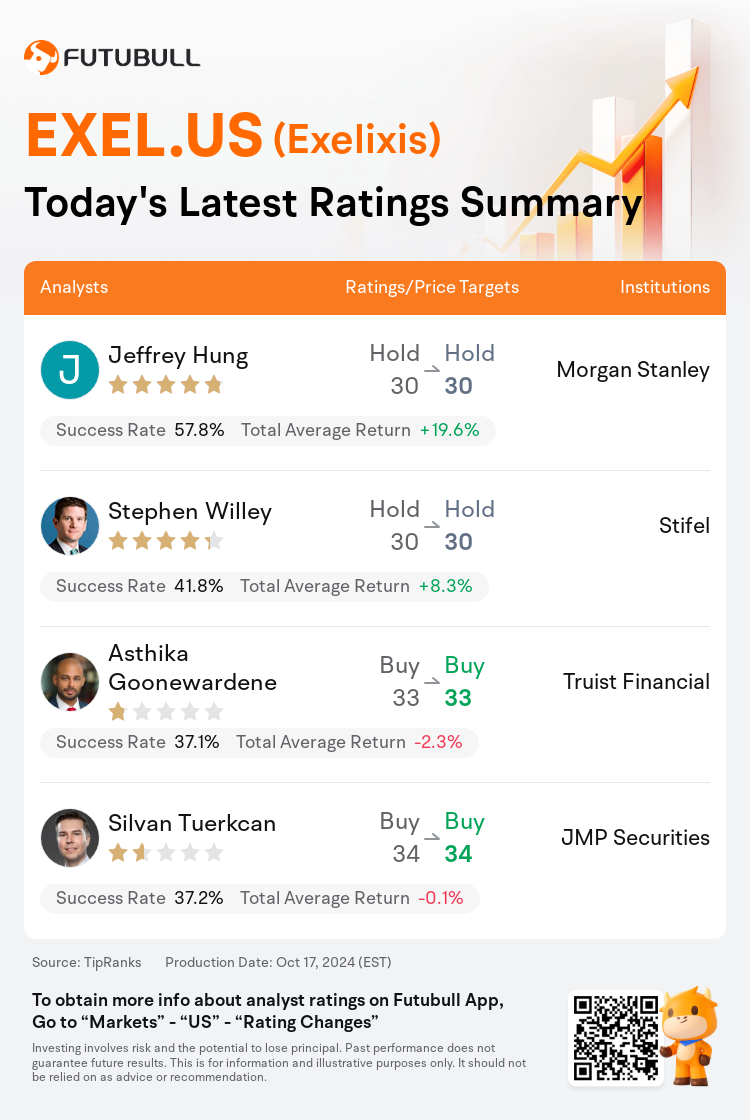

On Oct 17, major Wall Street analysts update their ratings for $Exelixis (EXEL.US)$, with price targets ranging from $30 to $34.

Morgan Stanley analyst Jeffrey Hung maintains with a hold rating, and maintains the target price at $30.

Stifel analyst Stephen Willey maintains with a hold rating, and maintains the target price at $30.

Truist Financial analyst Asthika Goonewardene maintains with a buy rating, and maintains the target price at $33.

Truist Financial analyst Asthika Goonewardene maintains with a buy rating, and maintains the target price at $33.

JMP Securities analyst Silvan Tuerkcan maintains with a buy rating, and maintains the target price at $34.

Furthermore, according to the comprehensive report, the opinions of $Exelixis (EXEL.US)$'s main analysts recently are as follows:

The recent judicial decision regarding the Cabometyx MSN II case confirmed that the Malate Salt Patents remain valid, and the '349 patent was neither infringed upon nor invalid. This outcome is largely favorable as it ensures patent protection until 2030. Nevertheless, the ruling did not reach the most optimistic scenario which would have extended patent protection until 2032.

The recent ruling securing Cabometyx patent protection until 2030 has presented a renewed outlook for the company's shares. The progress of the company's pipeline is now emerging as a key factor for the stock's valuation. The extension of Cabo's exclusivity and the resulting improved outlook for the stock has led to increased optimism.

The recent resolution of the MSN Laboratories litigation is deemed an incremental boon for Exelixis, enhancing the predictability of Cabometyx's market exclusivity and granting the company a clearer perspective on future business development endeavors. The potential of zanzalintinib is seen as a significant element in the firm's strategy to evolve its business model following Cabometyx. Furthermore, the newly formed partnerships with a major pharmaceutical company are viewed with interest.

Following a legal ruling that MSN infringed on certain polymorph patents, it's believed that the validity of the claims for all involved patents stands. This development suggests that each additional year of intellectual protection for Cabometyx could translate into significant free cash flow. The outcome may prompt investors to take a closer look at zanza and other assets in the pipeline.

Here are the latest investment ratings and price targets for $Exelixis (EXEL.US)$ from 4 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

美東時間10月17日,多家華爾街大行更新了$伊克力西斯 (EXEL.US)$的評級,目標價介於30美元至34美元。

摩根士丹利分析師Jeffrey Hung維持持有評級,維持目標價30美元。

斯迪富分析師Stephen Willey維持持有評級,維持目標價30美元。

儲億銀行分析師Asthika Goonewardene維持買入評級,維持目標價33美元。

儲億銀行分析師Asthika Goonewardene維持買入評級,維持目標價33美元。

JMP Securities分析師Silvan Tuerkcan維持買入評級,維持目標價34美元。

此外,綜合報道,$伊克力西斯 (EXEL.US)$近期主要分析師觀點如下:

關於Cabometyx MSN II案件的最新司法裁決確認了Malate Salt專利仍然有效,而 '349 專利既沒有受到侵權也不無效。這一結果在很大程度上是有利的,因爲它確保了專利保護直到2030年。然而,裁決並沒有達到最樂觀的情況,這將延長專利保護至2032年。

最近的裁決確保了Cabometyx在2030年之前的專利保護,爲公司股票帶來了更新的展望。公司管道的進展現在成爲股票估值的一個關鍵因素。 Cabo獨家權的延長以及由此帶來的股票前景改善已經引發了增加的樂觀情緒。

最近解決了MSN Laboratories的訴訟被認爲是Exelixis的一個增量利好,增強了Cabometyx的市場獨佔性的可預測性,併爲公司在未來業務發展方面提供了更清晰的視角。 Zanzalintinib的潛力被視爲該公司在Cabometyx後跟隨其業務模式演變的重要因素。此外,與一家主要藥品公司新建立的合作伙伴關係備受關注。

在一項針對MSN侵犯某些多態性專利的法律裁決之後,人們認爲所有涉及的專利的聲明有效。這一發展表明,爲Cabometyx提供每一年的知識產權保護可能會轉化爲可觀的自由現金流。這一結果可能促使投資者更加關注Zanza和管道中的其他資產。

以下爲今日4位分析師對$伊克力西斯 (EXEL.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。