Acuity Brands, Inc.'s (NYSE:AYI) price-to-earnings (or "P/E") ratio of 21.9x might make it look like a sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 18x and even P/E's below 10x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

Recent times have been pleasing for Acuity Brands as its earnings have risen in spite of the market's earnings going into reverse. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

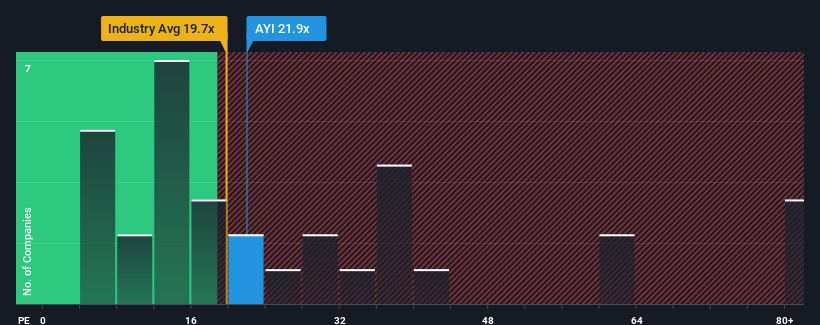

NYSE:AYI Price to Earnings Ratio vs Industry October 17th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Acuity Brands.

Does Growth Match The High P/E?

The only time you'd be truly comfortable seeing a P/E as high as Acuity Brands' is when the company's growth is on track to outshine the market.

If we review the last year of earnings growth, the company posted a terrific increase of 26%. The latest three year period has also seen an excellent 65% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 8.3% as estimated by the eight analysts watching the company. That's shaping up to be materially lower than the 15% growth forecast for the broader market.

With this information, we find it concerning that Acuity Brands is trading at a P/E higher than the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Bottom Line On Acuity Brands' P/E

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Acuity Brands currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for Acuity Brands with six simple checks on some of these key factors.

You might be able to find a better investment than Acuity Brands. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Acuity Brands, Inc. (紐交所:AYI) 目前的市盈率爲21.9倍,與美國市場相比可能看起來像是一個賣出選擇,因爲約一半公司的市盈率低於18倍,甚至低於10倍的市盈率也相當普遍。儘管如此,僅僅看市盈率並不能全面評估,因爲可能存在某些原因導致市盈率高於預期。

If we review the last year of earnings growth, the company posted a terrific increase of 26%. The latest three year period has also seen an excellent 65% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

If we review the last year of earnings growth, the company posted a terrific increase of 26%. The latest three year period has also seen an excellent 65% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

如果我們回顧過去一年的收益增長,該公司實現了驚人的26%的增長。最近三年的期間,每股收益也出現了65%的全面增長,受短期業績的支撐。因此,股東們可能會對這些中期收益增長率感到滿意。

如果我們回顧過去一年的收益增長,該公司實現了驚人的26%的增長。最近三年的期間,每股收益也出現了65%的全面增長,受短期業績的支撐。因此,股東們可能會對這些中期收益增長率感到滿意。