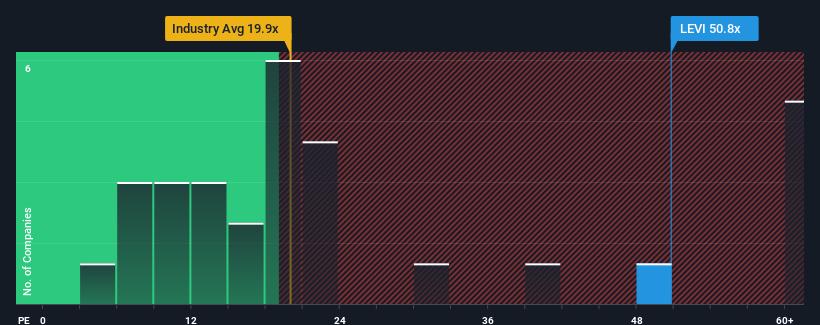

Levi Strauss & Co.'s (NYSE:LEVI) price-to-earnings (or "P/E") ratio of 50.8x might make it look like a strong sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 18x and even P/E's below 10x are quite common. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Recent times haven't been advantageous for Levi Strauss as its earnings have been falling quicker than most other companies. One possibility is that the P/E is high because investors think the company will turn things around completely and accelerate past most others in the market. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

NYSE:LEVI Price to Earnings Ratio vs Industry October 7th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Levi Strauss.

Is There Enough Growth For Levi Strauss?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Levi Strauss' to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 44%. This means it has also seen a slide in earnings over the longer-term as EPS is down 66% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 65% each year during the coming three years according to the analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 10% per annum, which is noticeably less attractive.

In light of this, it's understandable that Levi Strauss' P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Levi Strauss' analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Levi Strauss, and understanding them should be part of your investment process.

You might be able to find a better investment than Levi Strauss. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 44%. This means it has also seen a slide in earnings over the longer-term as EPS is down 66% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 44%. This means it has also seen a slide in earnings over the longer-term as EPS is down 66% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

回顧過去一年的收益,令人沮喪的是公司的利潤下降了44%。這意味着它在過去三年中的每股收益總額也下降了66%。因此,股東們可能對中期收益增長率感到悲觀。

回顧過去一年的收益,令人沮喪的是公司的利潤下降了44%。這意味着它在過去三年中的每股收益總額也下降了66%。因此,股東們可能對中期收益增長率感到悲觀。