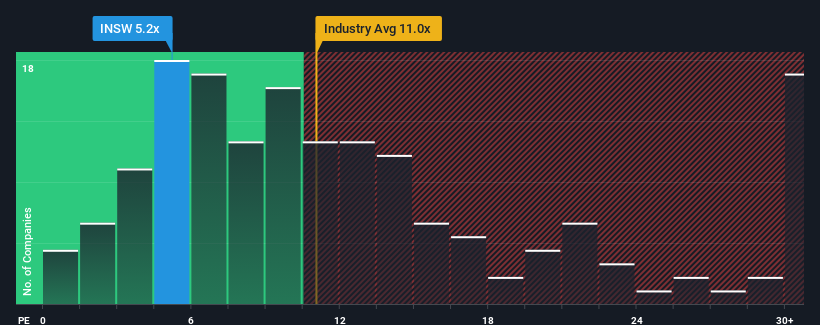

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") above 19x, you may consider International Seaways, Inc. (NYSE:INSW) as a highly attractive investment with its 5.2x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

With earnings that are retreating more than the market's of late, International Seaways has been very sluggish. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

NYSE:INSW Price to Earnings Ratio vs Industry October 4th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on International Seaways.

How Is International Seaways' Growth Trending?

International Seaways' P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 21%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Looking ahead now, EPS is anticipated to slump, contracting by 11% per annum during the coming three years according to the six analysts following the company. Meanwhile, the broader market is forecast to expand by 10% per annum, which paints a poor picture.

In light of this, it's understandable that International Seaways' P/E would sit below the majority of other companies. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of International Seaways' analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for International Seaways (1 makes us a bit uncomfortable) you should be aware of.

You might be able to find a better investment than International Seaways. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 21%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 21%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

首先回顧一下,去年公司的每股收益增長並不令人興奮,因爲它發佈了令人失望的下降21%。不幸的是,這使其回到了三年前的起點,那時整體上每股收益的增長几乎不存在。因此,從我們的角度來看,該公司在增長收入方面在那段時間內取得了一些成果。

首先回顧一下,去年公司的每股收益增長並不令人興奮,因爲它發佈了令人失望的下降21%。不幸的是,這使其回到了三年前的起點,那時整體上每股收益的增長几乎不存在。因此,從我們的角度來看,該公司在增長收入方面在那段時間內取得了一些成果。