Those holding Nexa Resources S.A. (NYSE:NEXA) shares would be relieved that the share price has rebounded 26% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Looking back a bit further, it's encouraging to see the stock is up 29% in the last year.

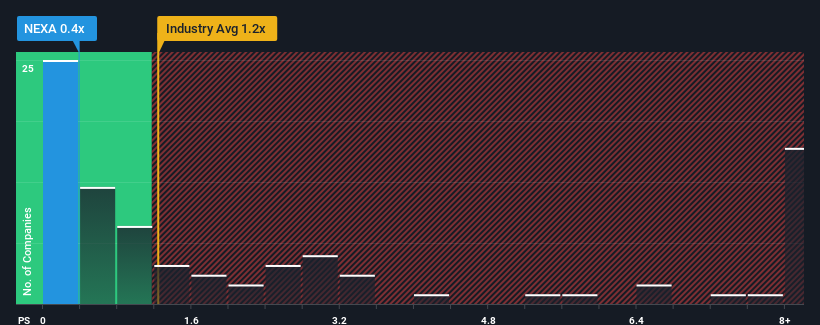

In spite of the firm bounce in price, Nexa Resources may still be sending bullish signals at the moment with its price-to-sales (or "P/S") ratio of 0.4x, since almost half of all companies in the Metals and Mining industry in the United States have P/S ratios greater than 1.2x and even P/S higher than 5x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

NYSE:NEXA Price to Sales Ratio vs Industry October 2nd 2024

What Does Nexa Resources' P/S Mean For Shareholders?

While the industry has experienced revenue growth lately, Nexa Resources' revenue has gone into reverse gear, which is not great. Perhaps the P/S remains low as investors think the prospects of strong revenue growth aren't on the horizon. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Nexa Resources.

Do Revenue Forecasts Match The Low P/S Ratio?

Nexa Resources' P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 6.5%. Regardless, revenue has managed to lift by a handy 5.4% in aggregate from three years ago, thanks to the earlier period of growth. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 2.7% as estimated by the six analysts watching the company. That's shaping up to be materially lower than the 22% growth forecast for the broader industry.

In light of this, it's understandable that Nexa Resources' P/S sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

The latest share price surge wasn't enough to lift Nexa Resources' P/S close to the industry median. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Nexa Resources' analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

You always need to take note of risks, for example - Nexa Resources has 1 warning sign we think you should be aware of.

If you're unsure about the strength of Nexa Resources' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Nexa Resources' P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Nexa Resources' P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Nexa Resources的市銷率對於預期增長有限且重要的表現不及行業板塊。

Nexa Resources的市銷率對於預期增長有限且重要的表現不及行業板塊。