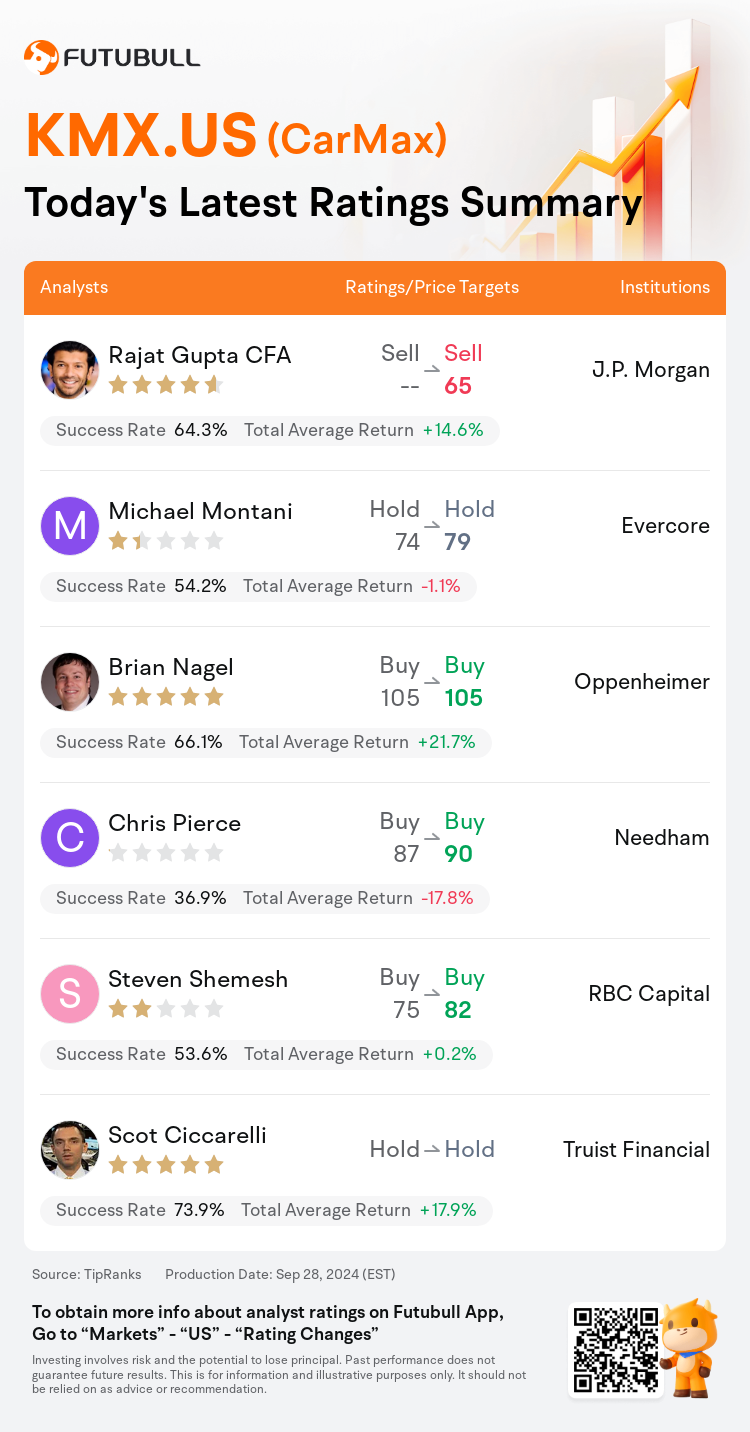

On Sep 28, major Wall Street analysts update their ratings for $CarMax (KMX.US)$, with price targets ranging from $65 to $105.

J.P. Morgan analyst Rajat Gupta CFA maintains with a sell rating, and sets the target price at $65.

Evercore analyst Michael Montani maintains with a hold rating, and adjusts the target price from $74 to $79.

Oppenheimer analyst Brian Nagel maintains with a buy rating, and maintains the target price at $105.

Oppenheimer analyst Brian Nagel maintains with a buy rating, and maintains the target price at $105.

Needham analyst Chris Pierce maintains with a buy rating, and adjusts the target price from $87 to $90.

RBC Capital analyst Steven Shemesh maintains with a buy rating, and adjusts the target price from $75 to $82.

Furthermore, according to the comprehensive report, the opinions of $CarMax (KMX.US)$'s main analysts recently are as follows:

CarMax's fiscal Q2 results offered a sneak peek at stabilizing share and potential growth in retail profits. Nonetheless, the possibility of increased loan losses and an inconsistent backdrop for low to middle income consumers still poses a risk. Looking forward, there's an anticipation for a gradual stabilization of market share and a betterment in underlying profitability, even though earnings per share strength may stay subdued into calendar 2025.

CarMax's Q2 outcomes were a blend of an earnings shortfall contrasted with a surpass in revenue. The company experienced a 4.3% uptick in comparable retail units, suggesting a hopeful trend into Q3, yet faced a 14% year-over-year decrease in CarMax Auto Finance income, alongside indications of deteriorating credit metrics. Despite a reduction in the projected earnings per share for FY24 and FY25, it's believed that unit trends have found a stable footing. Additionally, the anticipation of lower interest rates is seen as a catalyst for a higher earnings multiple estimate.

Here are the latest investment ratings and price targets for $CarMax (KMX.US)$ from 6 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

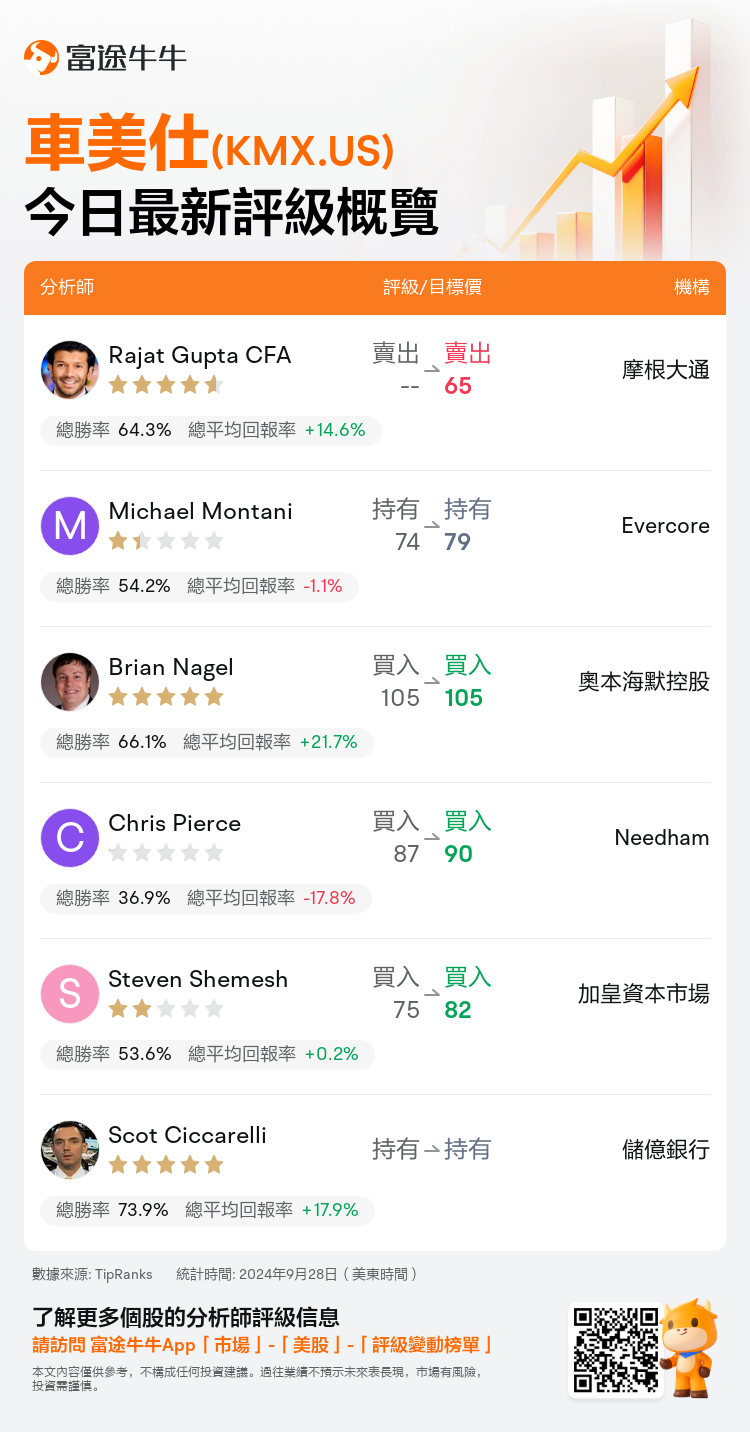

美東時間9月28日,多家華爾街大行更新了$車美仕 (KMX.US)$的評級,目標價介於65美元至105美元。

摩根大通分析師Rajat Gupta CFA維持賣出評級,目標價65美元。

Evercore分析師Michael Montani維持持有評級,並將目標價從74美元上調至79美元。

奧本海默控股分析師Brian Nagel維持買入評級,維持目標價105美元。

奧本海默控股分析師Brian Nagel維持買入評級,維持目標價105美元。

Needham分析師Chris Pierce維持買入評級,並將目標價從87美元上調至90美元。

加皇資本市場分析師Steven Shemesh維持買入評級,並將目標價從75美元上調至82美元。

此外,綜合報道,$車美仕 (KMX.US)$近期主要分析師觀點如下:

CarMax的第二財季業績爲穩定的份額和零售利潤的潛在增長提供了先睹爲快。儘管如此,中低收入消費者貸款損失增加的可能性以及背景不一致仍然構成風險。展望未來,儘管到2025年,每股收益的強勁勢頭可能會保持低迷,但人們預計市場份額將逐漸穩定,基礎盈利能力將得到改善。

CarMax第二季度的業績混合了收益不足與收入的超額形成鮮明對比。該公司的可比零售單位增長了4.3%,這表明第三季度呈現出令人鼓舞的趨勢,但CarMax汽車融資收入同比下降了14%,同時有信貸指標惡化的跡象。儘管24財年和25財年的預計每股收益有所下降,但據信單位趨勢已經找到了穩定的基礎。此外,對較低利率的預期被視爲提高收益倍數估計值的催化劑。

以下爲今日6位分析師對$車美仕 (KMX.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。