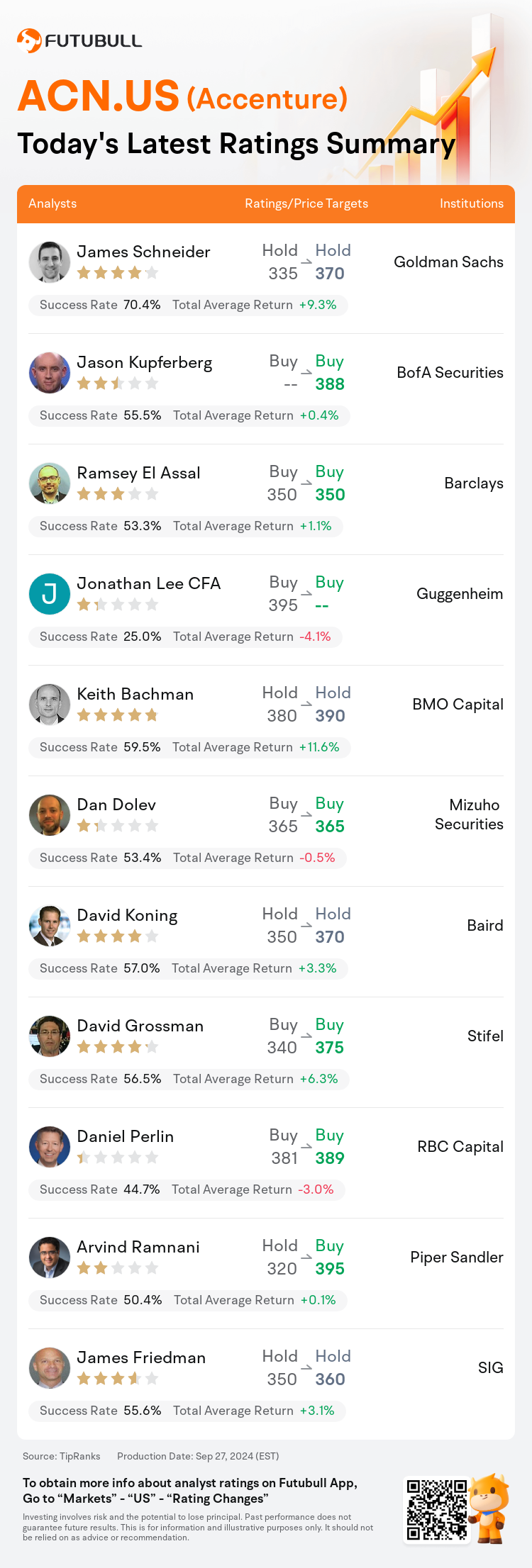

On Sep 27, major Wall Street analysts update their ratings for $Accenture (ACN.US)$, with price targets ranging from $350 to $395.

Goldman Sachs analyst James Schneider maintains with a hold rating, and adjusts the target price from $335 to $370.

BofA Securities analyst Jason Kupferberg maintains with a buy rating, and sets the target price at $388.

Barclays analyst Ramsey El Assal maintains with a buy rating, and maintains the target price at $350.

Barclays analyst Ramsey El Assal maintains with a buy rating, and maintains the target price at $350.

Guggenheim analyst Jonathan Lee CFA maintains with a buy rating.

BMO Capital analyst Keith Bachman maintains with a hold rating, and adjusts the target price from $380 to $390.

Furthermore, according to the comprehensive report, the opinions of $Accenture (ACN.US)$'s main analysts recently are as follows:

The stock is anticipated to experience an expansion in its multiple as the advent of Gen AI is expected to drive revenue growth in conjunction with ongoing capital return.

The key insights from Accenture's earnings discussion highlighted that the upper range of the FY25 constant currency revenue growth forecast between 3%-6% does not count on any uptick in discretionary spending. Conversely, the lower end has room to absorb a potential decline. It is believed that investors will value the understated nature of this early FY25 projection. Additionally, a comparison to the previous year shows a rise in the volume of substantial transformational contracts currently in backlog, which bolsters visibility.

Ongoing momentum within the Health & Public Service sector has bolstered management's confidence in achieving the upper boundary of the company's projected 0-3% year-over-year constant currency organic growth. This has resulted in a more optimistic narrative regarding the company's organic growth prospects for FY25.

Accenture's robust Q4 earnings surpassed expectations, attributed to the recognition of revenue from larger projects initiated in previous periods, which has significantly propelled sequential growth, especially within the Strategy & Consulting segment. Furthermore, a substantial increase was observed in gen-AI bookings for FY24, reaching over $3 billion, with corresponding revenues escalating to $900 million, compared to $300 million and $100 million in FY23.

The assessment reflects that Accenture's valuation is considered balanced in light of constrained organic growth, yet acknowledges the company's robust bookings. The projection for fiscal year 2025 is in line with general expectations, with the revenue outlook for 2024 slightly surpassing the consensus. Additionally, the company saw strong performance in Managed Services bookings and a modest enhancement in GenAI bookings.

Here are the latest investment ratings and price targets for $Accenture (ACN.US)$ from 11 analysts:

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

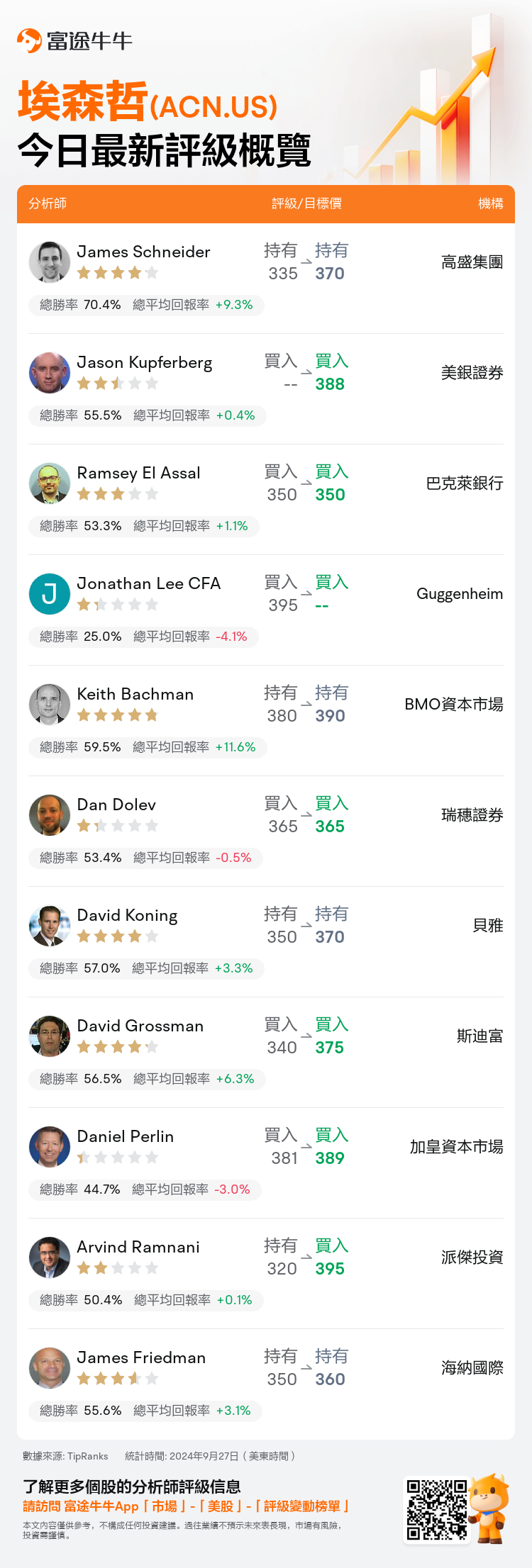

美東時間9月27日,多家華爾街大行更新了$埃森哲 (ACN.US)$的評級,目標價介於350美元至395美元。

高盛集團分析師James Schneider維持持有評級,並將目標價從335美元上調至370美元。

美銀證券分析師Jason Kupferberg維持買入評級,目標價388美元。

巴克萊銀行分析師Ramsey El Assal維持買入評級,維持目標價350美元。

巴克萊銀行分析師Ramsey El Assal維持買入評級,維持目標價350美元。

Guggenheim分析師Jonathan Lee CFA維持買入評級。

BMO資本市場分析師Keith Bachman維持持有評級,並將目標價從380美元上調至390美元。

此外,綜合報道,$埃森哲 (ACN.US)$近期主要分析師觀點如下:

預計該股的倍數將擴大,因爲預計Gen AI的出現將推動收入增長以及持續的資本回報。

埃森哲業績討論中的關鍵見解突出表明,25財年固定貨幣收入增長預測的上限在3%-6%之間,並不意味着全權支出會有任何增加。相反,低端有吸收潛在下跌的空間。據信,投資者將看重25財年初預測的低調性質。此外,與去年相比,目前積壓的大量轉型合同數量有所增加,這提高了知名度。

健康和公共服務領域的持續勢頭增強了管理層的信心,即實現公司預計的同比固定貨幣有機增長0-3%的上限。這使人們對公司25財年的有機增長前景有了更加樂觀的看法。

埃森哲第四季度強勁的收益超出了預期,這要歸因於前幾個時期啓動的大型項目的收入得到確認,這極大地推動了連續增長,尤其是在戰略與諮詢領域。此外,觀察到24財年的Gen-AI預訂量大幅增加,達到30億美元以上,相應的收入從23財年的3億美元和1億美元增加到9億美元。

該評估表明,鑑於有機增長受限,埃森哲的估值被認爲是平衡的,但也承認了該公司的強勁預訂。2025財年的預測符合總體預期,2024年的收入前景略高於市場預期。此外,該公司在管理服務預訂方面表現強勁,GenAI預訂量略有增加。

以下爲今日11位分析師對$埃森哲 (ACN.US)$的最新投資評級及目標價:

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。