Frontier Group Holdings, Inc. (NASDAQ:ULCC) shareholders are no doubt pleased to see that the share price has bounced 26% in the last month, although it is still struggling to make up recently lost ground. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 7.0% over the last year.

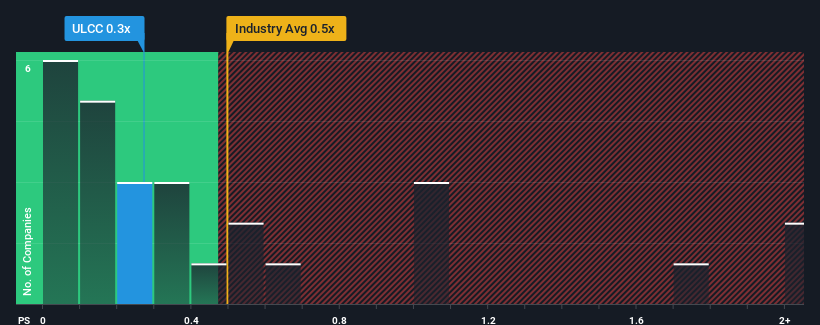

In spite of the firm bounce in price, it's still not a stretch to say that Frontier Group Holdings' price-to-sales (or "P/S") ratio of 0.3x right now seems quite "middle-of-the-road" compared to the Airlines industry in the United States, where the median P/S ratio is around 0.4x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

NasdaqGS:ULCC Price to Sales Ratio vs Industry September 22nd 2024

What Does Frontier Group Holdings' P/S Mean For Shareholders?

Frontier Group Holdings could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Want the full picture on analyst estimates for the company? Then our free report on Frontier Group Holdings will help you uncover what's on the horizon.

Is There Some Revenue Growth Forecasted For Frontier Group Holdings?

Frontier Group Holdings' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. Still, the latest three year period has seen an excellent 171% overall rise in revenue, in spite of its uninspiring short-term performance. Therefore, it's fair to say the revenue growth recently has been great for the company, but investors will want to ask why it has slowed to such an extent.

Turning to the outlook, the next year should generate growth of 10% as estimated by the ten analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 51%, which is noticeably more attractive.

With this in mind, we find it intriguing that Frontier Group Holdings' P/S is closely matching its industry peers. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

What Does Frontier Group Holdings' P/S Mean For Investors?

Its shares have lifted substantially and now Frontier Group Holdings' P/S is back within range of the industry median. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Given that Frontier Group Holdings' revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. Circumstances like this present a risk to current and prospective investors who may see share prices fall if the low revenue growth impacts the sentiment.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for Frontier Group Holdings with six simple checks on some of these key factors.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Frontier Group Holdings, Inc. (納斯達克股票代碼: ULCC) 的股東們無疑很高興看到股價在過去一個月裏上漲了26%,儘管它仍在努力彌補最近失去的地位。不幸的是,即使在過去30天中股票恢復了,股東們在過去一年中仍有約7.0%的虧損。

儘管股價有所反彈,但可以說Frontier Group Holdings的市銷率目前爲0.3倍,與美國航空公司行業的中位數市銷率約爲0.4倍相比,似乎相對平均。然而,如果市銷率沒有合理的基礎,投資者可能會忽視一個明顯的機會或潛在的挫折。

納斯達克股票代碼: ULCC 的市銷率與行業比較於2024年9月22日

Frontier Group Holdings的市銷率對股東意味着什麼?

由於最近Frontier Group Holdings的營業收入一直在下降,而大多數其他公司的營業收入增長都爲正,它的表現可能還有改進的空間。如果許多人期待這種低迷的營收表現能夠積極恢復,這就使得市銷率沒有下降。你真的希望如此,否則你爲這樣一家增長潛力有限的公司支付了相對較高的價格。

想要了解該公司的分析師對該公司的預測嗎?那麼我們關於Frontier Group Holdings的免費報告將幫助您揭示未來的情景。

Frontier Group Holdings是否有一定的營收增長預測?

Frontier Group Holdings的市銷率對於一家預計只能實現適度增長並且與行業持平的公司來說是典型的。

Frontier Group Holdings' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Frontier Group Holdings' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Frontier Group Holdings的市銷率對於一家預計只能實現適度增長並且與行業持平的公司來說是典型的。

Frontier Group Holdings的市銷率對於一家預計只能實現適度增長並且與行業持平的公司來說是典型的。