Further Weakness as Digimarc (NASDAQ:DMRC) Drops 9.1% This Week, Taking Five-year Losses to 41%

Further Weakness as Digimarc (NASDAQ:DMRC) Drops 9.1% This Week, Taking Five-year Losses to 41%

Over five years, Digimarc grew its revenue at 11% per year. That's a fairly respectable growth rate. Shareholders have seen the share price fall at 7% per year, for five years: a poor performance. Clearly, the expectations from back then have not been satisfied. The lesson is that if you buy shares in a money losing company you could end up losing money.

Over five years, Digimarc grew its revenue at 11% per year. That's a fairly respectable growth rate. Shareholders have seen the share price fall at 7% per year, for five years: a poor performance. Clearly, the expectations from back then have not been satisfied. The lesson is that if you buy shares in a money losing company you could end up losing money. For many, the main point of investing is to generate higher returns than the overall market. But the main game is to find enough winners to more than offset the losers At this point some shareholders may be questioning their investment in Digimarc Corporation (NASDAQ:DMRC), since the last five years saw the share price fall 41%. We also note that the stock has performed poorly over the last year, with the share price down 23%. And the share price decline continued over the last week, dropping some 9.1%.

對於許多人來說,投資的主要目的是產生比整體市場更高的回報。但主要的問題是找到足夠多的贏家來彌補輸家的損失。此時,一些股東可能會對他們在數字標識公司(納斯達克:DMRC)的投資產生疑問,因爲過去五年股價下跌了41%。我們還注意到,該股在過去一年表現不佳,股價下跌了23%。而股價的下跌在過去一週繼續下跌,下跌了9.1%。

With the stock having lost 9.1% in the past week, it's worth taking a look at business performance and seeing if there's any red flags.

由於該股在過去一週內下跌了9.1%,因此值得查看業務表現以確定是否存在任何警示信號。

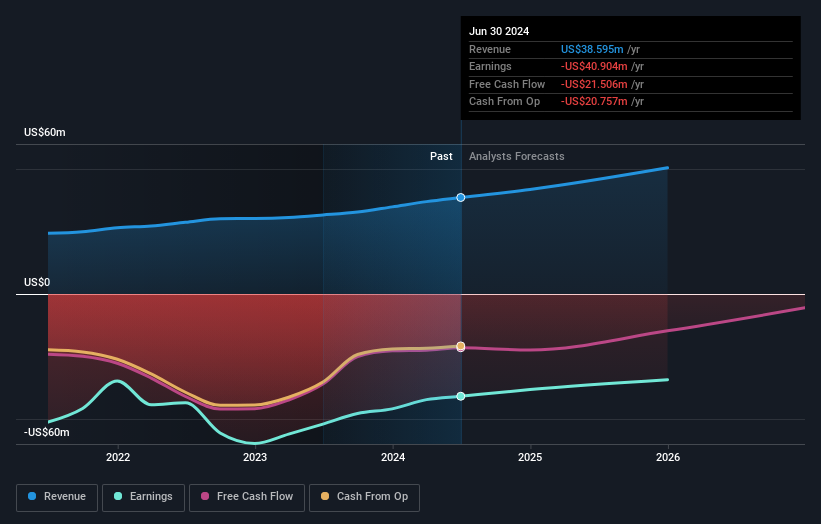

Digimarc wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. When a company doesn't make profits, we'd generally hope to see good revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

數字標識在過去十二個月內沒有盈利,因此其股價與每股收益(EPS)之間的關聯性不強。可以說,營業收入是我們的下一個最好的選擇。當一家公司沒有盈利時,我們通常希望看到良好的營業收入增長。這是因爲如果營業收入增長微乎其微,而且從未盈利,很難相信這家公司將能持續下去。

Over five years, Digimarc grew its revenue at 11% per year. That's a fairly respectable growth rate. Shareholders have seen the share price fall at 7% per year, for five years: a poor performance. Clearly, the expectations from back then have not been satisfied. The lesson is that if you buy shares in a money losing company you could end up losing money.

在過去的五年中,數字標識的營業收入以每年11%的速度增長。這是一個相當可觀的增長率。股東們看到股價在過去五年中以每年7%的速度下跌,表現不佳。顯然,當時的期望沒有得到滿足。教訓是,如果你購買了一家虧損的公司的股票,你可能會虧錢。

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

以下圖像顯示了公司的營業收入和盈利(隨時間變化)(單擊以查看準確的數字)。

If you are thinking of buying or selling Digimarc stock, you should check out this FREE detailed report on its balance sheet.

如果你正在考慮買入或賣出Digimarc股票,你應該查看這份免費的詳細報告和它的資產負債表。

A Different Perspective

不同的觀點

Investors in Digimarc had a tough year, with a total loss of 23%, against a market gain of about 23%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 7% per year over five years. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. To that end, you should be aware of the 2 warning signs we've spotted with Digimarc .

Digimarc的投資者度過了艱難的一年,總虧損達到23%,而市場卻獲得了大約23%的收益。但是,請記住,即使是最好的股票有時也會在12個月的期間表現不佳。遺憾的是,去年的表現使這段糟糕的運行又雪上加霜,股東們在過去五年中面臨了每年總損失7%。一般來說,長期股價的走弱可能是一個不好的跡象,儘管反向投資者可能希望通過研究股票來寄望逆轉。我發現從長期來看股價是業務表現的代理指標非常有趣。但是要真正獲取洞察力,我們還需要考慮其他信息。爲此,你應該注意到我們發現的2個關鍵風險。

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: many of them are unnoticed AND have attractive valuation).

如果您喜歡與管理層一起購買股票,那麼您可能會喜歡這個公司的免費列表。 (提示:其中許多公司不爲人注意且具有吸引力的估值。)

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

請注意,本文所引述的市場回報反映了目前在美國交易所上市的股票的市場加權平均回報。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

譯文內容由第三人軟體翻譯。