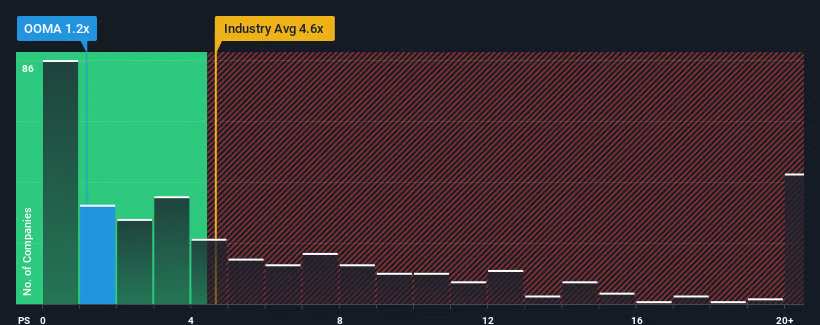

Ooma, Inc.'s (NYSE:OOMA) price-to-sales (or "P/S") ratio of 1.2x might make it look like a strong buy right now compared to the Software industry in the United States, where around half of the companies have P/S ratios above 4.6x and even P/S above 11x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

NYSE:OOMA Price to Sales Ratio vs Industry August 29th 2024

What Does Ooma's Recent Performance Look Like?

Recent times haven't been great for Ooma as its revenue has been rising slower than most other companies. It seems that many are expecting the uninspiring revenue performance to persist, which has repressed the growth of the P/S ratio. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Keen to find out how analysts think Ooma's future stacks up against the industry? In that case, our free report is a great place to start.

What Are Revenue Growth Metrics Telling Us About The Low P/S?

In order to justify its P/S ratio, Ooma would need to produce anemic growth that's substantially trailing the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 8.7% last year. The latest three year period has also seen an excellent 38% overall rise in revenue, aided somewhat by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 7.9% each year during the coming three years according to the seven analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 19% per year, which is noticeably more attractive.

In light of this, it's understandable that Ooma's P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Ooma maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. The company will need a change of fortune to justify the P/S rising higher in the future.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Ooma you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Taking a look back first, we see that the company managed to grow revenues by a handy 8.7% last year. The latest three year period has also seen an excellent 38% overall rise in revenue, aided somewhat by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Taking a look back first, we see that the company managed to grow revenues by a handy 8.7% last year. The latest three year period has also seen an excellent 38% overall rise in revenue, aided somewhat by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

首先回顧一下,去年該公司的營業收入有了令人滿意的8.7%的增長。過去三年,營業收入總體上也增長了38%,在短期的表現的幫助下得到了一些推動。因此,股東肯定會歡迎這些中期的營收增長率。

首先回顧一下,去年該公司的營業收入有了令人滿意的8.7%的增長。過去三年,營業收入總體上也增長了38%,在短期的表現的幫助下得到了一些推動。因此,股東肯定會歡迎這些中期的營收增長率。