Impressive Earnings May Not Tell The Whole Story For Yoshitsu (NASDAQ:TKLF)

Impressive Earnings May Not Tell The Whole Story For Yoshitsu (NASDAQ:TKLF)

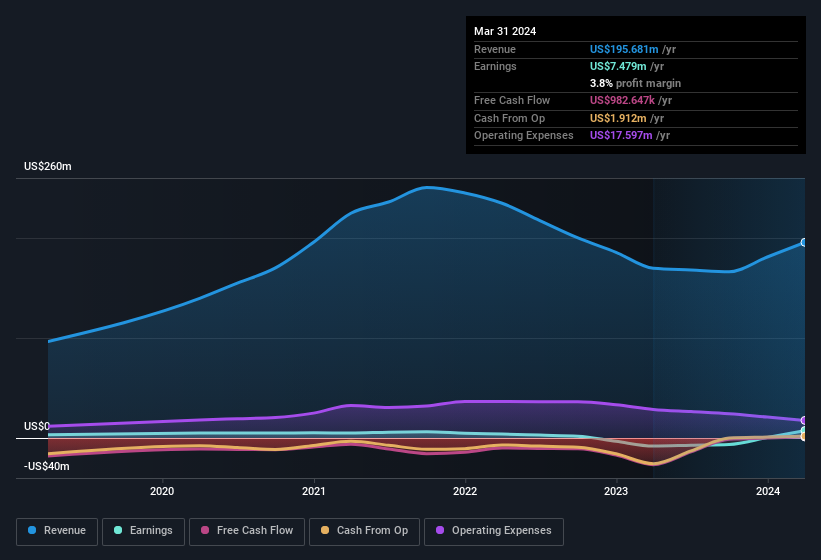

Yoshitsu Co., Ltd (NASDAQ:TKLF) just reported some strong earnings, and the market reacted accordingly with a healthy uplift in the share price. We did some analysis and think that investors are missing some details hidden beneath the profit numbers.

Yoshitsu有限公司(納斯達克:TKLF)剛剛公佈了一些強勁的收益,市場隨即出現了健康的股價上漲。我們進行了一些分析,並認爲投資者正在錯過盈利數字之下隱藏的一些細節。

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. As it happens, Yoshitsu issued 16% more new shares over the last year. Therefore, each share now receives a smaller portion of profit. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out Yoshitsu's historical EPS growth by clicking on this link.

爲了了解一個公司收益增長的價值,必須考慮到股東利益的任何稀釋。事實上,Yoshitsu在過去一年中發行了更多的新股,增加了16%。因此,每股收益現在獲得的利潤份額更少了。光憑淨利潤就慶祝,而忽略了股份稀釋的影響,就像因爲你有一個大披薩的一片而興高采烈,但忽略了這個披薩現在被分成更多片。點擊此鏈接查看Yoshitsu歷史上每股收益的增長。

How Is Dilution Impacting Yoshitsu's Earnings Per Share (EPS)?

稀釋對Yoshitsu的每股收益(EPS)產生了何種影響?

Unfortunately, we don't have any visibility into its profits three years back, because we lack the data. And even focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). And so, you can see quite clearly that dilution is influencing shareholder earnings.

不幸的是,由於我們缺乏數據,我們無法了解其三年前的利潤情況。即使是隻關注過去十二個月,我們也沒有一個有意義的增長率,因爲它一年前也曾虧損。但撇開數學不談,看到曾經虧損的企業表現良好總是好的(雖然我們認爲如果不需要稀釋,利潤會更高)。所以,很明顯,稀釋正在影響股東的收益。

If Yoshitsu's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

如果Yoshitsu的每股收益能夠隨着時間增長,則股票價格大幅上漲的可能性會大大提高。但另一方面,我們會感到不太興奮,了解到利潤(但不是EPS)正在改善。對於普通的零售股東,EPS是檢查公司利潤假想“份額”的好措施。

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Yoshitsu.

注意:我們始終建議投資者檢查資產負債表的強度。點擊此處,進入我們對Yoshitsu資產負債表分析的界面。

The Impact Of Unusual Items On Profit

除了稀釋之外,還應該注意的是,萬集科技在過去12個月中因不尋常項目獲得了價值人民幣3.5萬元的利潤。雖然我們希望看到利潤增加,但當這些不尋常項目對利潤做出重大貢獻時,我們會更加謹慎。我們對全球大部分上市公司的數據進行了分析,發現不尋常項目往往是一次性的。這正如我們所期望的那樣,因爲這些提升被描述爲"不尋常"。相對於其利潤而言,萬集科技在2021年12月前的不尋常項目貢獻大。因此,我們可以推斷出,這些不尋常項目正在使其財務利潤顯著增強。

Alongside that dilution, it's also important to note that Yoshitsu's profit was boosted by unusual items worth US$1.1m in the last twelve months. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's as you'd expect, given these boosts are described as 'unusual'. If Yoshitsu doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

除了稀釋之外,還要注意,Yoshitsu的利潤在過去十二個月中受到了價值110萬美元的不尋常項目的推動。我們不能否認,更高的利潤通常會讓我們感到樂觀,但我們更希望它是可持續的。當我們分析全球大多數上市公司時,我們發現不尋常的項目往往不會重複。這是可以預料的,因爲這些收益被描述爲“不尋常的”。如果Yoshitsu沒有看到這種收益的持續增加,那麼一切都相等,我們預計其利潤將在當前年份下降。

Our Take On Yoshitsu's Profit Performance

我們對Yoshitsu的盈利表現的看法

To sum it all up, Yoshitsu got a nice boost to profit from unusual items; without that, its statutory results would have looked worse. And furthermore, it went and issued plenty of new shares, ensuring that each shareholder (who did not tip more money in) now owns a smaller proportion of the company. Considering all this we'd argue Yoshitsu's profits probably give an overly generous impression of its sustainable level of profitability. If you'd like to know more about Yoshitsu as a business, it's important to be aware of any risks it's facing. For instance, we've identified 5 warning signs for Yoshitsu (3 are a bit concerning) you should be familiar with.

總之,Yoshitsu從不尋常的項目中獲得了利潤的巨大提升;如果沒有這一點,其法定結果看起來會更糟。此外,它還發行了大量新股,確保每個股東(沒有更多投資的股東)現在擁有的公司比例更小了。考慮到所有這些,我們認爲Yoshitsu的利潤可能過於慷慨地表現了其可持續盈利水平的形象。如果您想更多了解Yoshitsu作爲一家企業的情況,了解任何風險是很重要的。例如,我們已經爲Yoshitsu確定了5個警示信號(其中3個有點令人擔憂),您應該了解這些風險。

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

在本文中,我們已經看到了可以損害利潤數字實用性的許多因素,而且我們已經變得謹慎。但是,如果您能夠將注意力集中在細節上,則總有更多發現。有些人認爲高淨資產回報率是高質量企業的一個好標誌。因此,您可能希望查看這個高淨資產回報率的免費公司收集,或這個高內部所有權的股票清單。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

對本文有任何反饋?對內容有任何疑慮?請直接與我們聯繫。或者,發送電子郵件至editorial-team@simplywallst.com。

譯文內容由第三人軟體翻譯。