Franklin Wireless Corp. (NASDAQ:FKWL) shares have continued their recent momentum with a 26% gain in the last month alone. Looking further back, the 18% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

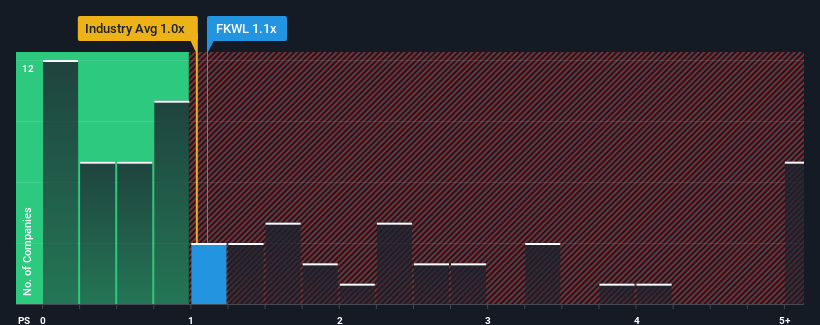

Although its price has surged higher, you could still be forgiven for feeling indifferent about Franklin Wireless' P/S ratio of 1.1x, since the median price-to-sales (or "P/S") ratio for the Communications industry in the United States is also close to 1x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

NasdaqCM:FKWL Price to Sales Ratio vs Industry July 17th 2024

What Does Franklin Wireless' Recent Performance Look Like?

It looks like revenue growth has deserted Franklin Wireless recently, which is not something to boast about. One possibility is that the P/S is moderate because investors think this benign revenue growth rate might not be enough to outperform the broader industry in the near future. Those who are bullish on Franklin Wireless will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

Although there are no analyst estimates available for Franklin Wireless, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.

What Are Revenue Growth Metrics Telling Us About The P/S?

Franklin Wireless' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

If we review the last year of revenue, the company posted a result that saw barely any deviation from a year ago. This isn't what shareholders were looking for as it means they've been left with a 80% decline in revenue over the last three years in total. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Comparing that to the industry, which is predicted to deliver 4.7% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

In light of this, it's somewhat alarming that Franklin Wireless' P/S sits in line with the majority of other companies. Apparently many investors in the company are way less bearish than recent times would indicate and aren't willing to let go of their stock right now. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

The Key Takeaway

Its shares have lifted substantially and now Franklin Wireless' P/S is back within range of the industry median. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

The fact that Franklin Wireless currently trades at a P/S on par with the rest of the industry is surprising to us since its recent revenues have been in decline over the medium-term, all while the industry is set to grow. When we see revenue heading backwards in the context of growing industry forecasts, it'd make sense to expect a possible share price decline on the horizon, sending the moderate P/S lower. If recent medium-term revenue trends continue, it will place shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Franklin Wireless (of which 1 makes us a bit uncomfortable!) you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Franklin Wireless Corp. (納斯達克:FKWL)的股票在過去一個月中保持了其近期勢頭,漲幅高達26%。回溯更長的時間,儘管過去30天表現強勁,但在過去12個月中上漲18%並不算太糟糕。

Franklin Wireless目前與其餘行業以相同的市銷率交易,這對我們來說是令人驚訝的,因爲該公司的最近營收在中期內一直在下降,而整個行業卻保持增長。當我們看到營收在增長行業預測的背景下向後退縮時,可以合理地預期可能會出現潛在的股票價格下跌,將市銷率降低至更低的水平。如果最近的中期營收趨勢持續下去,它將使股東的投資風險增加,潛在投資者將面臨支付不必要的溢價的危險。

Franklin Wireless' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Franklin Wireless' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Franklin Wireless的市銷率對於一個只預計實現溫和增長並且與行業表現基本持平的公司來說是典型的。

Franklin Wireless的市銷率對於一個只預計實現溫和增長並且與行業表現基本持平的公司來說是典型的。