Bath & Body Works, Inc. (NYSE:BBWI) shareholders won't be pleased to see that the share price has had a very rough month, dropping 26% and undoing the prior period's positive performance. Longer-term shareholders will rue the drop in the share price, since it's now virtually flat for the year after a promising few quarters.

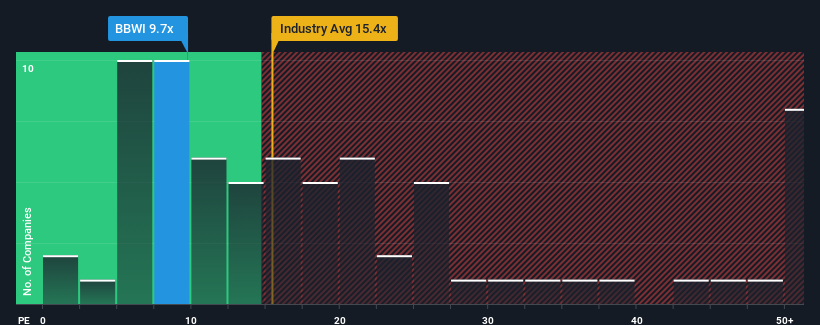

Although its price has dipped substantially, given about half the companies in the United States have price-to-earnings ratios (or "P/E's") above 17x, you may still consider Bath & Body Works as an attractive investment with its 9.7x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Recent times have been pleasing for Bath & Body Works as its earnings have risen in spite of the market's earnings going into reverse. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

NYSE:BBWI Price to Earnings Ratio vs Industry July 2nd 2024 Want the full picture on analyst estimates for the company? Then our free report on Bath & Body Works will help you uncover what's on the horizon.

Is There Any Growth For Bath & Body Works?

In order to justify its P/E ratio, Bath & Body Works would need to produce sluggish growth that's trailing the market.

If we review the last year of earnings growth, the company posted a terrific increase of 24%. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 12% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 2.2% per year over the next three years. With the market predicted to deliver 10% growth per annum, the company is positioned for a weaker earnings result.

In light of this, it's understandable that Bath & Body Works' P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Key Takeaway

Bath & Body Works' recently weak share price has pulled its P/E below most other companies. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Bath & Body Works' analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

You should always think about risks. Case in point, we've spotted 4 warning signs for Bath & Body Works you should be aware of, and 1 of them can't be ignored.

If these risks are making you reconsider your opinion on Bath & Body Works, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Bath & Body Works, Inc. (NYSE:BBWI) 的股東將不高興看到股價在過去一個月中大幅下跌26%,並撤銷了上期的積極表現。從更長期來看,股價的下跌可能會讓股東感到遺憾,因爲經過幾個季度的希望,現在的股價基本持平。

儘管其價格已大幅下跌,但考慮到美國約一半的公司市盈率(或“P/E”)高於17倍,您仍可以考慮Bath & Body Works作爲一種有吸引力的投資,因爲其市盈率爲9.7倍。不過,僅僅看市盈率未必聰明,因爲可能有一個限制的解釋。

最近的時期對Bath & Body Works來說是令人愉悅的,因爲其收益即使在市場收益逆轉的情況下仍在上升。可能會有很多人認爲,強勁的收益表現可能會大幅惡化,可能比市場更爲嚴重,而市盈率則受到抑制。如果不是這樣,那麼現有股東對股價未來走勢有充分的理由感到樂觀。

NYSE:BBWI千萬股收益比行業板塊2024年7月2日想要了解關於公司的分析師預測的完整信息?那麼我們對Bath & Body Works的免費報告將幫助您揭示未來的情況。