Starbucks (NASDAQ:SBUX) Investors Are Sitting on a Loss of 28% If They Invested Three Years Ago

Starbucks (NASDAQ:SBUX) Investors Are Sitting on a Loss of 28% If They Invested Three Years Ago

In order to justify the effort of selecting individual stocks, it's worth striving to beat the returns from a market index fund. But if you try your hand at stock picking, you risk returning less than the market. Unfortunately, that's been the case for longer term Starbucks Corporation (NASDAQ:SBUX) shareholders, since the share price is down 32% in the last three years, falling well short of the market return of around 18%. Shareholders have had an even rougher run lately, with the share price down 15% in the last 90 days.

爲了證明選擇個股的努力是值得的,努力打敗市場指數基金的回報是值得的。但如果您嘗試進行個股選擇,則有可能面臨低於市場回報的風險。不幸的是,在過去的三年中,長揸星巴克公司(NASDAQ:SBUX)股票的股東人數不斷減少,因爲股票價格跌了32%,遠低於市場回報率約18%。股東最近的日子更爲艱難,股票價格在過去的90天內下跌了15%。

It's worthwhile assessing if the company's economics have been moving in lockstep with these underwhelming shareholder returns, or if there is some disparity between the two. So let's do just that.

值得評估公司的經濟狀況是否與這些不盡如人意的股東回報同時發展並步調一致,或者兩者之間是否存在差異。因此,讓我們來看看。

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

引用本傑明·格雷厄姆的話:短期內市場是一個投票機,但長期來看它是一個稱重機。評估公司周邊環境的情緒變化的一種有缺陷但合理的方法是將每股收益(EPS)與股價進行比較。

During the unfortunate three years of share price decline, Starbucks actually saw its earnings per share (EPS) improve by 63% per year. Given the share price reaction, one might suspect that EPS is not a good guide to the business performance during the period (perhaps due to a one-off loss or gain). Alternatively, growth expectations may have been unreasonable in the past.

不幸的是,在股票價格下跌的三年中,星巴克實際上每年的每股收益(EPS)有所提高,提高了63%。鑑於股票價格的反應,人們可能會懷疑在此期間EPS是否不是業務表現的良好指南(可能是由於一次性損失或收益),或者過去的增長預期可能是不合理的。

Since the change in EPS doesn't seem to correlate with the change in share price, it's worth taking a look at other metrics.

由於EPS的變化似乎與股價的變化不相關,因此值得查看其他指標。

We note that, in three years, revenue has actually grown at a 12% annual rate, so that doesn't seem to be a reason to sell shares. It's probably worth investigating Starbucks further; while we may be missing something on this analysis, there might also be an opportunity.

我們注意到,在三年內,營業收入實際上以12%的年度增長率增長,因此這似乎不是出售股票的原因。可能值得進一步調查星巴克公司;雖然我們可能在這個分析中有所遺漏,但也可能存在機會。

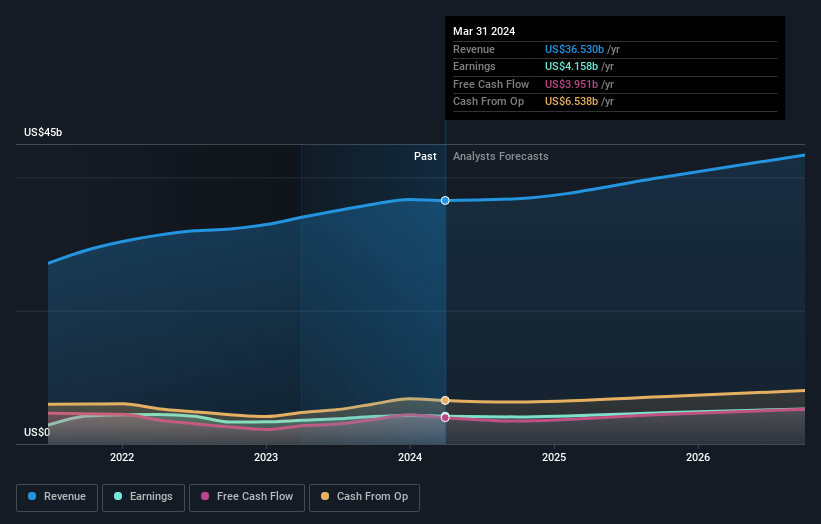

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

以下圖像顯示了公司的營業收入和盈利(隨時間變化)(單擊以查看準確的數字)。

Starbucks is a well known stock, with plenty of analyst coverage, suggesting some visibility into future growth. So we recommend checking out this free report showing consensus forecasts

星巴克是一隻廣受關注的知名股票,有很多分析師進行了覆蓋,這表明有一定的未來增長可見性。因此,我們建議查看這份免費報告,展示共識預測。

What About Dividends?

那麼分紅怎麼樣呢?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. In the case of Starbucks, it has a TSR of -28% for the last 3 years. That exceeds its share price return that we previously mentioned. And there's no prize for guessing that the dividend payments largely explain the divergence!

除了衡量股票價格回報外,投資者還應考慮股東總回報(TSR)。股票價格回報只反映了股票價格的變化,TSR還包括股息的價值(假設它們進行了再投資)以及任何打折募資或剝離的效益。從某種意義上說,TSR提供了更全面的股票回報圖片。在星巴克的例子中,最近3年TSR爲-28%。這超過了我們之前提到的股價回報。想必股息支付在很大程度上解釋了這種分歧!

A Different Perspective

不同的觀點

While the broader market gained around 23% in the last year, Starbucks shareholders lost 19% (even including dividends). However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 0.3% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with Starbucks (at least 1 which is a bit concerning) , and understanding them should be part of your investment process.

儘管最近一年市場總體上漲約23%,但星巴克的股東卻虧損了19%(包括股息在內)。然而,要記住,即使最好的股票也有時會在十二個月的時間內表現低於市場。可悔的是,去年的表現結束了糟糕的時期,股東在過去五年中面臨了年平均總損失0.3%。我們認識到Baron Rothschild曾說過投資者應該“在街上有血時買進”,但我們警告投資者首先要確定他們正在購買高質量的企業。雖然考慮到市場條件對股票價格的不同影響是值得考慮的,但還有其他更重要的因素。例如,永遠存在的投資風險。我們已檢測到星巴克存在兩個警示信號(至少有一個有點令人擔憂),了解這些警示信號應成爲您的投資過程的一部分。

For those who like to find winning investments this free list of undervalued companies with recent insider purchasing, could be just the ticket.

對於那些喜歡尋找獲勝投資的人來說,最近有內部購買的低估公司免費列表可能是一個很好的選擇。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

請注意,本文所引述的市場回報反映了目前在美國交易所上市的股票的市場加權平均回報。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?關於內容有所顧慮?直接和我們聯繫。或者,發送電子郵件至editorial-team (at) simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

對本文有反饋?關於內容有所顧慮?直接和我們聯繫。或者發送電子郵件至editorial-team@simplywallst.com。

譯文內容由第三人軟體翻譯。