Shareholders May Be More Conservative With SJW Group's (NYSE:SJW) CEO Compensation For Now

Shareholders May Be More Conservative With SJW Group's (NYSE:SJW) CEO Compensation For Now

Key Insights

主要見解

- SJW Group's Annual General Meeting to take place on 20th of June

- Total pay for CEO Eric Thornburg includes US$874.0k salary

- Total compensation is 1,441% above industry average

- Over the past three years, SJW Group's EPS grew by 7.0% and over the past three years, the total loss to shareholders 17%

- SJW集團的股東年會將於6月20日舉行。

- 總裁埃裏克·桑伯格的總薪酬包括874.0萬美元的工資。

- 總補償額比行業平均水平高出1441%。

- 在過去的三年裏,SJW集團的EPS增長了7.0%,而在過去的三年裏,股東的總損失爲17%。

The underwhelming share price performance of SJW Group (NYSE:SJW) in the past three years would have disappointed many shareholders. What is concerning is that despite positive EPS growth, the share price has not tracked the trend in fundamentals. The AGM coming up on the 20th of June could be an opportunity for shareholders to bring these concerns to the board's attention. Voting on resolutions such as executive remuneration and other matters could also be a way to influence management. Here's our take on why we think shareholders may want to be cautious of approving a raise for the CEO at the moment.

在過去的三年中,SJW集團(紐交所:SJW)的股價表現令許多股東失望。更令人擔憂的是,儘管EPS增長表現出正面趨勢,但股價並未跟隨基本面的趨勢。6月20日即將舉行的年度股東大會可能是股東將這些問題帶到董事會注意的機會。投票表決如執行薪酬和其他事項也可以成爲影響管理的方法。以下是我們對爲什麼股東可能要謹慎批准CEO加薪的看法。

How Does Total Compensation For Eric Thornburg Compare With Other Companies In The Industry?

埃裏克·桑伯格的總薪酬與其他公司在行業中的比較如何?

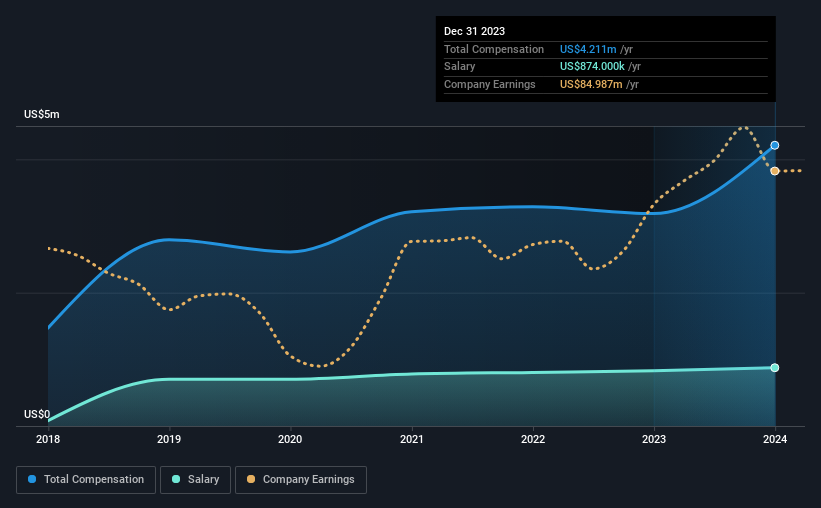

At the time of writing, our data shows that SJW Group has a market capitalization of US$1.7b, and reported total annual CEO compensation of US$4.2m for the year to December 2023. Notably, that's an increase of 32% over the year before. We think total compensation is more important but our data shows that the CEO salary is lower, at US$874k.

截至撰寫本文時,我們的數據顯示,SJW集團的市值爲17億美元,截至2023年12月報告的CEO總年薪爲420萬美元。值得注意的是,這比前一年增加了32%。我們認爲總薪酬更重要,但我們的數據顯示CEO工資較低,爲874,000美元。

On examining similar-sized companies in the American Water Utilities industry with market capitalizations between US$1.0b and US$3.2b, we discovered that the median CEO total compensation of that group was US$273k. This suggests that Eric Thornburg is paid more than the median for the industry. What's more, Eric Thornburg holds US$2.4m worth of shares in the company in their own name.

在美國水務公用事業行業市值在10億美元至32億美元之間的同等規模公司中,我們發現該集團CEO薪酬中位數爲273,000美元。這表明埃裏克·桑伯格的薪酬超過了該行業的中位數。此外,埃裏克·桑伯格以自己的名義持有價值240萬美元的公司股票。

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$874k | US$828k | 21% |

| Other | US$3.3m | US$2.4m | 79% |

| Total Compensation | US$4.2m | US$3.2m | 100% |

| 組成部分 | 2023 | 2022 | 比例(2023) |

| 薪資 | 874,000美元 | 828,000美元 | 21% |

| 其他 | 3300000美元 | 240萬美元 | 79% |

| 總補償 | 420萬美元 | 320萬美元 | 100% |

On an industry level, around 38% of total compensation represents salary and 62% is other remuneration. It's interesting to note that SJW Group allocates a smaller portion of compensation to salary in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

在行業層面上,約38%的總補償代表工資,62%的補償是其他報酬。值得注意的是,與整個行業相比,SJW集團將更少的報酬分配給工資。如果非工資報酬占主導地位,這表明高管薪資與公司績效掛鉤。

SJW Group's Growth

SJW集團的增長

SJW Group has seen its earnings per share (EPS) increase by 7.0% a year over the past three years. Its revenue is up 7.7% over the last year.

在過去的三年中,SJW集團的每股收益(EPS)年增長率爲7.0%。其營業收入在去年上漲了7.7%。

We would argue that the improvement in revenue is good, but isn't particularly impressive, but we're happy with the modest EPS growth. Considering these factors we'd say performance has been pretty decent, though not amazing. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

我們認爲收入的改善是好的,但並不特別令人印象深刻,但我們對於適度的EPS增長感到滿意。考慮到這些因素,我們認爲表現相當不錯,雖然並不是令人驚豔的。放棄當前形式,檢查這位分析師對未來期望的自由視覺描繪可能是很重要的。

Has SJW Group Been A Good Investment?

SJW集團是個好投資嗎?

Since shareholders would have lost about 17% over three years, some SJW Group investors would surely be feeling negative emotions. So shareholders would probably want the company to be less generous with CEO compensation.

由於股東在過去三年中將損失約17%,一些SJW集團的投資者肯定會感到消極情緒。因此,股東可能希望公司在CEO薪酬上不那麼慷慨。

To Conclude...

總之...

The fact that shareholders are sitting on a loss on the value of their shares in the past few years is certainly disconcerting. A huge lag in share price growth when earnings have grown may indicate there could be other issues that are affecting the company at the moment that the market is focused on. If there are some unknown variables that are influencing the stock's price, surely shareholders would have some concerns. At the upcoming AGM, shareholders will get the opportunity to discuss any issues with the board, including those related to CEO remuneration and assess if the board's plan will likely improve performance in the future.

股東持股的價值在過去幾年中的下跌事實確實令人不安。在盈利增長時股價增長嚴重滯後,可能表明目前市場關注的是其他問題。如果有一些未知變量正在影響股價,股東肯定會有些擔憂。即將到來的年度股東大會,股東將有機會討論與董事會相關的任何問題,包括與CEO薪酬有關的問題,並評估董事會的計劃是否有可能改善未來的業績。

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 3 warning signs for SJW Group (of which 1 doesn't sit too well with us!) that you should know about in order to have a holistic understanding of the stock.

通過研究公司的CEO薪酬趨勢以及其他方面的情況,我們可以了解公司各方面的狀況。這就是爲什麼我們進行了研究,並確定了SJW集團存在3個警告信號(其中1個不太合適),以便您全面了解股票。

Important note: SJW Group is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

重要說明:sjw group 是一隻激動人心的股票,但我們明白投資者可能正在尋找無負擔的資產負債表和巨大的回報。您可能會在這份有高roe和低債務的有趣公司名單中找到更好的選擇。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對本文有反饋?關於內容有所顧慮?直接和我們聯繫。或者,發送電子郵件至editorial-team (at) simplywallst.com。

這篇文章是Simply Wall St的一般性文章。我們根據歷史數據和分析師預測提供評論,只使用公正的方法論,我們的文章並不意味着提供任何金融建議。文章不構成買賣任何股票的建議,也不考慮您的目標或您的財務狀況。我們的目標是帶給您基本數據驅動的長期關注分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。Simply Wall St沒有任何股票頭寸。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

對本文有反饋?關於內容有所顧慮?直接和我們聯繫。或者發送電子郵件至editorial-team@simplywallst.com。

譯文內容由第三人軟體翻譯。