The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Comfort Systems USA (NYSE:FIX). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Comfort Systems USA with the means to add long-term value to shareholders.

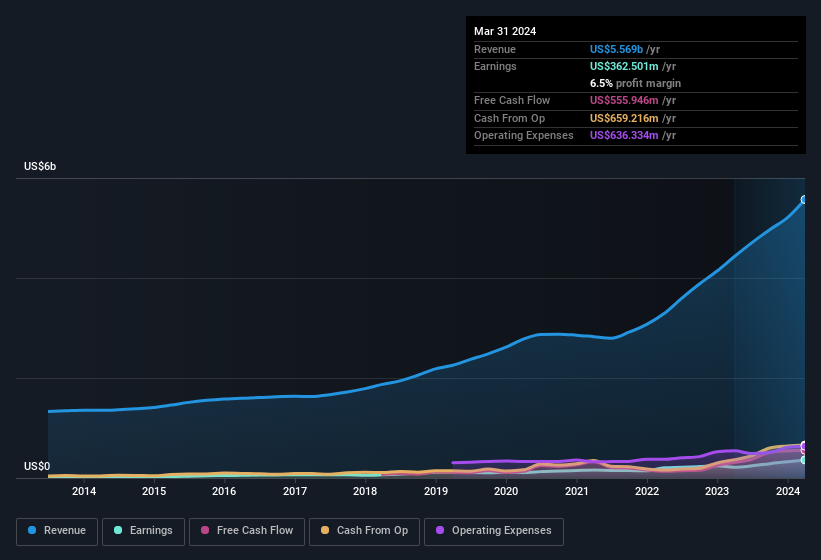

How Quickly Is Comfort Systems USA Increasing Earnings Per Share?

Generally, companies experiencing growth in earnings per share (EPS) should see similar trends in share price. That means EPS growth is considered a real positive by most successful long-term investors. Impressively, Comfort Systems USA has grown EPS by 33% per year, compound, in the last three years. If growth like this continues on into the future, then shareholders will have plenty to smile about.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. Comfort Systems USA shareholders can take confidence from the fact that EBIT margins are up from 6.3% to 8.8%, and revenue is growing. Ticking those two boxes is a good sign of growth, in our book.

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

NYSE:FIX Earnings and Revenue History May 23rd 2024

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Comfort Systems USA's future profits.

Are Comfort Systems USA Insiders Aligned With All Shareholders?

Owing to the size of Comfort Systems USA, we wouldn't expect insiders to hold a significant proportion of the company. But thanks to their investment in the company, it's pleasing to see that there are still incentives to align their actions with the shareholders. We note that their impressive stake in the company is worth US$183m. This suggests that leadership will be very mindful of shareholders' interests when making decisions!

While it's always good to see some strong conviction in the company from insiders through heavy investment, it's also important for shareholders to ask if management compensation policies are reasonable. Our quick analysis into CEO remuneration would seem to indicate they are. For companies with market capitalisations over US$8.0b, like Comfort Systems USA, the median CEO pay is around US$14m.

The Comfort Systems USA CEO received total compensation of just US$6.6m in the year to December 2023. First impressions seem to indicate a compensation policy that is favourable to shareholders. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. It can also be a sign of good governance, more generally.

Should You Add Comfort Systems USA To Your Watchlist?

If you believe that share price follows earnings per share you should definitely be delving further into Comfort Systems USA's strong EPS growth. If that's not enough, consider also that the CEO pay is quite reasonable, and insiders are well-invested alongside other shareholders. Everyone has their own preferences when it comes to investing but it definitely makes Comfort Systems USA look rather interesting indeed. You should always think about risks though. Case in point, we've spotted 1 warning sign for Comfort Systems USA you should be aware of.

While opting for stocks without growing earnings and absent insider buying can yield results, for investors valuing these key metrics, here is a carefully selected list of companies in the US with promising growth potential and insider confidence.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對一些投機者來說,投資一家能夠扭轉命運的公司的興奮感是一個很大的吸引力,因此,即使是沒有收入、沒有利潤、有虧損記錄的公司,也可以設法找到投資者。但是正如彼得·林奇所說 One Up On Wall 街,“遠射幾乎永遠不會得到回報。”虧損的公司總是與時間賽跑以實現財務可持續性,因此這些公司的投資者承擔的風險可能超出了應有的範圍。

因此,如果這種高風險和高回報的想法不適合,那麼你可能會對盈利的、成長中的公司更感興趣,例如美國舒適系統(紐約證券交易所代碼:FIX)。即使市場對這家公司進行了合理的估值,投資者也會同意,創造穩定的利潤將繼續爲Comfort Systems USA提供爲股東增加長期價值的手段。

如果你認爲股價跟隨每股收益,那麼你肯定應該進一步研究美國舒適系統公司的強勁每股收益增長。如果這還不夠,還要考慮首席執行官的薪酬相當合理,內部人士與其他股東一起投資良好。在投資方面,每個人都有自己的偏好,但這無疑使Comfort Systems USA看起來確實很有趣。但是,你應該時刻考慮風險。舉個例子,我們發現了一個你應該注意的美國舒適系統警告標誌。