Inner Mongolia Baotou Steel Union (SHSE:600010) Has A Somewhat Strained Balance Sheet

Inner Mongolia Baotou Steel Union (SHSE:600010) Has A Somewhat Strained Balance Sheet

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Inner Mongolia Baotou Steel Union Co., Ltd. (SHSE:600010) does have debt on its balance sheet. But is this debt a concern to shareholders?

由伯克希尔·哈撒韦公司的查理·芒格支持的外部基金经理李露对此毫不掩饰,他说:“最大的投资风险不是价格的波动,而是你是否会遭受永久的资本损失。”因此,很明显,当你考虑任何给定股票的风险时,你需要考虑债务,因为过多的债务会使公司陷入困境。我们注意到,内蒙古包钢联股份有限公司(SHSE: 600010)的资产负债表上确实有债务。但是这笔债务是股东关心的问题吗?

Why Does Debt Bring Risk?

为什么债务会带来风险?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

当企业无法通过自由现金流或以有吸引力的价格筹集资金来轻松履行债务和其他负债时,债务和其他负债就会面临风险。资本主义的重要组成部分是 “创造性破坏” 的过程,在这个过程中,倒闭的企业将被银行家无情地清算。但是,更常见(但仍然代价高昂)的情况是,公司必须以低廉的价格发行股票,永久稀释股东,以支撑其资产负债表。当然,债务的好处在于它通常代表廉价资本,尤其是当它取代了对一家能够以高回报率进行再投资的公司的摊薄时。当我们检查债务水平时,我们首先要同时考虑现金和债务水平。

What Is Inner Mongolia Baotou Steel Union's Net Debt?

内蒙古包钢联的净负债是多少?

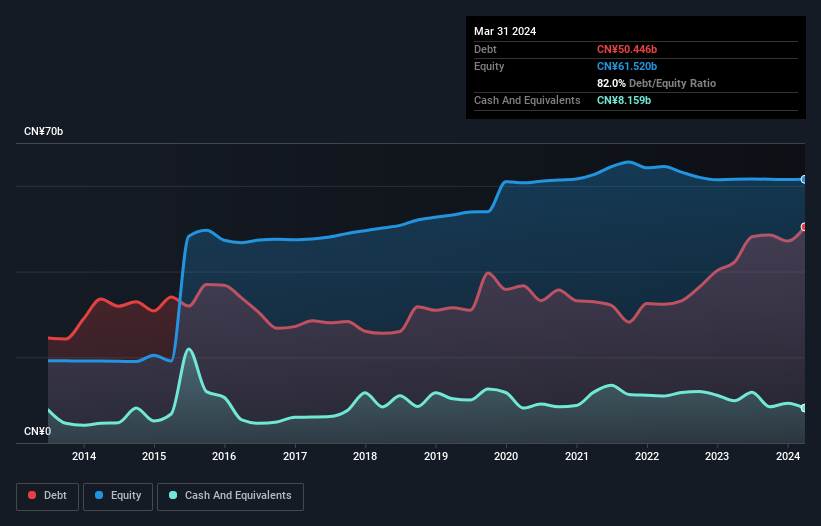

The image below, which you can click on for greater detail, shows that at March 2024 Inner Mongolia Baotou Steel Union had debt of CN¥50.4b, up from CN¥42.2b in one year. However, because it has a cash reserve of CN¥8.16b, its net debt is less, at about CN¥42.3b.

您可以点击下图查看更多详情,该图片显示,截至2024年3月,内蒙古包头钢铁联盟的债务为504亿元人民币,高于一年内的422亿元人民币。但是,由于其现金储备为81.6亿元人民币,其净负债较少,约为423亿元人民币。

How Strong Is Inner Mongolia Baotou Steel Union's Balance Sheet?

内蒙古包头钢铁联盟的资产负债表有多强?

According to the last reported balance sheet, Inner Mongolia Baotou Steel Union had liabilities of CN¥66.4b due within 12 months, and liabilities of CN¥24.9b due beyond 12 months. On the other hand, it had cash of CN¥8.16b and CN¥13.8b worth of receivables due within a year. So it has liabilities totalling CN¥69.3b more than its cash and near-term receivables, combined.

根据上次报告的资产负债表,内蒙古包头钢铁联盟的负债为664亿元人民币,12个月以后到期的负债为249亿元人民币。另一方面,它有一年内到期的现金为81.6亿元人民币,还有价值138亿元人民币的应收账款。因此,它的负债总额比现金和短期应收账款的总和多出693亿元人民币。

This is a mountain of leverage relative to its market capitalization of CN¥72.2b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

相对于其722亿元人民币的市值,这是一座巨大的杠杆率。如果其贷款人要求其支撑资产负债表,股东可能会面临严重的稀释。

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

我们使用两个主要比率来告知我们相对于收益的债务水平。第一个是净负债除以利息、税项、折旧和摊销前的收益(EBITDA),第二个是其利息和税前收益(EBIT)覆盖其利息支出(或简称利息保障)的多少倍。因此,我们将债务与收益的关系考虑在内,包括和不包括折旧和摊销费用。

Inner Mongolia Baotou Steel Union shareholders face the double whammy of a high net debt to EBITDA ratio (6.8), and fairly weak interest coverage, since EBIT is just 1.2 times the interest expense. This means we'd consider it to have a heavy debt load. However, it should be some comfort for shareholders to recall that Inner Mongolia Baotou Steel Union actually grew its EBIT by a hefty 164%, over the last 12 months. If it can keep walking that path it will be in a position to shed its debt with relative ease. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Inner Mongolia Baotou Steel Union's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

由于息税前利润仅为利息支出的1.2倍,内蒙古包钢联的股东面临着净负债与息税折旧摊销前利润比率高(6.8)和相当薄弱的利息覆盖率的双重打击。这意味着我们会认为它有沉重的债务负担。但是,回想起内蒙古包头钢铁联盟在过去12个月中实际上将其息税前利润大幅增长了164%,这应该让股东感到欣慰。如果它能继续走这条路,它将能够相对轻松地减轻债务。资产负债表显然是分析债务时需要关注的领域。但是,未来收益将决定内蒙古包头钢铁联盟未来维持健康资产负债表的能力。因此,如果你想看看专业人士的想法,你可能会发现这份关于分析师利润预测的免费报告很有趣。

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. During the last three years, Inner Mongolia Baotou Steel Union produced sturdy free cash flow equating to 78% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

最后,公司只能用冷硬现金偿还债务,不能用会计利润偿还债务。因此,值得检查一下息税前利润中有多少是由自由现金流支持的。在过去的三年中,内蒙古包头钢铁联盟产生了稳健的自由现金流,相当于其息税前利润的78%,与我们的预期差不多。这种自由现金流使公司处于有利地位,可以在适当的时候偿还债务。

Our View

我们的观点

We feel some trepidation about Inner Mongolia Baotou Steel Union's difficulty interest cover, but we've got positives to focus on, too. To wit both its EBIT growth rate and conversion of EBIT to free cash flow were encouraging signs. Looking at all the angles mentioned above, it does seem to us that Inner Mongolia Baotou Steel Union is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 1 warning sign with Inner Mongolia Baotou Steel Union , and understanding them should be part of your investment process.

我们对内蒙古包钢联的困难利息保障感到有些担忧,但我们也有积极的方面需要关注。顺便说一句,其息税前利润增长率以及将息税前利润转换为自由现金流都是令人鼓舞的迹象。从上面提到的所有角度来看,在我们看来,由于其债务,内蒙古包头钢铁联盟确实是一项风险较大的投资。这不一定是一件坏事,因为杠杆可以提高股本回报率,但这是需要注意的事情。毫无疑问,我们从资产负债表中学到的关于债务的知识最多。但归根结底,每家公司都可以控制资产负债表之外存在的风险。我们已经向内蒙古包头钢铁联盟确定了一个警告信号,我们知道它们应该成为您投资过程的一部分。

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

归根结底,通常最好将注意力集中在没有净负债的公司身上。您可以访问我们的此类公司的特别名单(所有公司都有利润增长记录)。它是免费的。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。