When we're researching a company, it's sometimes hard to find the warning signs, but there are some financial metrics that can help spot trouble early. When we see a declining return on capital employed (ROCE) in conjunction with a declining base of capital employed, that's often how a mature business shows signs of aging. This indicates to us that the business is not only shrinking the size of its net assets, but its returns are falling as well. And from a first read, things don't look too good at Groupon (NASDAQ:GRPN), so let's see why.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Groupon, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.067 = US$19m ÷ (US$581m - US$297m) (Based on the trailing twelve months to March 2024).

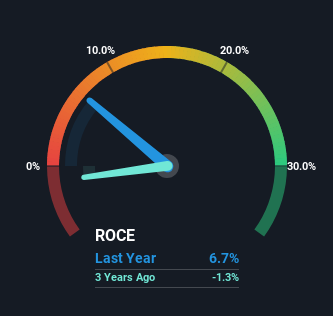

So, Groupon has an ROCE of 6.7%. Ultimately, that's a low return and it under-performs the Multiline Retail industry average of 11%.

NasdaqGS:GRPN Return on Capital Employed May 12th 2024

In the above chart we have measured Groupon's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for Groupon .

What Can We Tell From Groupon's ROCE Trend?

The trend of ROCE doesn't look fantastic because it's fallen from 12% five years ago and the business is utilizing 60% less capital, even after their capital raise (conducted prior to the latest reporting period).

On a side note, Groupon's current liabilities are still rather high at 51% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

What We Can Learn From Groupon's ROCE

In summary, it's unfortunate that Groupon is shrinking its capital base and also generating lower returns. We expect this has contributed to the stock plummeting 81% during the last five years. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

Groupon does have some risks though, and we've spotted 3 warning signs for Groupon that you might be interested in.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

當我們研究一家公司時,有時很難找到警告信號,但是有一些財務指標可以幫助及早發現問題。當我們看到下降時 返回 在資本使用率(ROCE)的下降的同時 基礎 就所使用的資本而言,成熟的企業通常會以這種方式顯示出老化的跡象。這向我們表明,該企業不僅在縮小其淨資產規模,而且其回報率也在下降。從第一次讀起,Groupon(納斯達克股票代碼:GRPN)的情況看起來並不太好,所以讓我們看看原因。

什麼是資本使用回報率(ROCE)?

如果你以前沒有與ROCE合作過,它會衡量公司從其業務中使用的資本中產生的 “回報”(稅前利潤)。要計算Groupon的這個指標,公式如下:

已動用資本回報率 = 息稅前收益 (EBIT) ¥(總資產-流動負債)

0.067 = 1900 萬美元 ÷(5.81 億美元-2.97 億美元) (基於截至2024年3月的過去十二個月)。

因此,Groupon的投資回報率爲6.7%。歸根結底,這是一個低迴報,其表現低於多線零售行業11%的平均水平。

納斯達克GS:GRPN 2024年5月12日動用資本回報率

在上圖中,我們將Groupon先前的投資回報率與之前的表現進行了比較,但可以說,未來更爲重要。如果您想了解分析師對未來的預測,則應查看我們的免費Groupon分析師報告。

我們可以從Groupon的投資回報率趨勢中得出什麼?

投資回報率的趨勢看起來並不理想,因爲它已從五年前的12%下降了,而且即使在籌集資金(在最新報告期之前進行)之後,該業務使用的資本也減少了60%。

順便說一句,Groupon的流動負債仍然相當高,佔總資產的51%。這可能會帶來一些風險,因爲該公司的運營基本上在很大程度上依賴其供應商或其他類型的短期債權人。理想情況下,我們希望看到這種情況減少,因爲這將意味着減少承擔風險的債務。

我們可以從 Groupon 的 ROCE 中學到什麼

總而言之,不幸的是,Groupon正在縮小其資本基礎,同時產生的回報也較低。我們預計,這導致該股在過去五年中暴跌了81%。既然如此,除非潛在趨勢恢復到更積極的軌跡,否則我們會考慮將目光投向其他地方。

但是,Groupon確實存在一些風險,我們已經發現了Groupon的3個警告信號,你可能會感興趣。