We Think Huadian Energy's (SHSE:600726) Solid Earnings Are Understated

We Think Huadian Energy's (SHSE:600726) Solid Earnings Are Understated

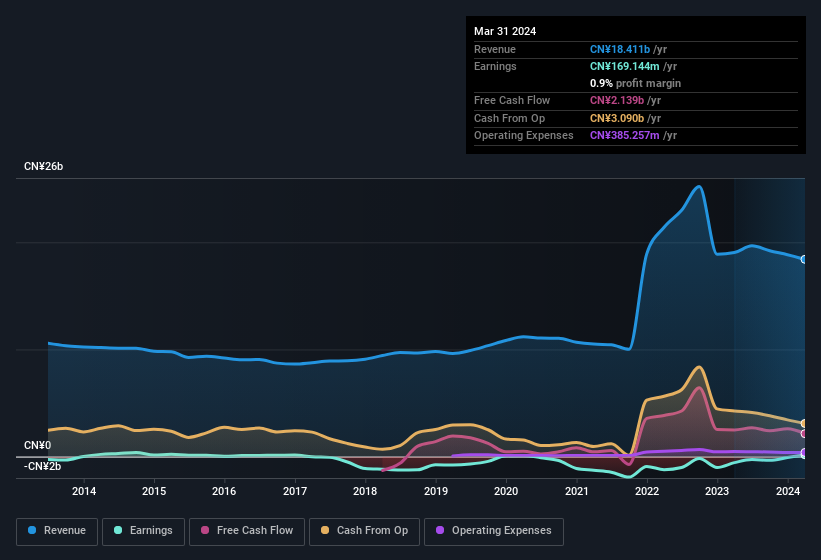

Huadian Energy has an accrual ratio of -0.11 for the year to March 2024. That indicates that its free cash flow was a fair bit more than its statutory profit. Indeed, in the last twelve months it reported free cash flow of CN¥2.1b, well over the CN¥169.1m it reported in profit. Huadian Energy did see its free cash flow drop year on year, which is less than ideal, like a Simpson's episode without Groundskeeper Willie.

Huadian Energy has an accrual ratio of -0.11 for the year to March 2024. That indicates that its free cash flow was a fair bit more than its statutory profit. Indeed, in the last twelve months it reported free cash flow of CN¥2.1b, well over the CN¥169.1m it reported in profit. Huadian Energy did see its free cash flow drop year on year, which is less than ideal, like a Simpson's episode without Groundskeeper Willie. Huadian Energy Company Limited (SHSE:600726) announced a healthy earnings result recently, and the market rewarded it with a strong uplift in the stock price. Looking deeper at the numbers, we found several encouraging factors beyond the headline profit numbers.

華電能源有限公司(SHSE: 600726)最近公佈了健康的收益業績,市場對其進行了強勁的股價上漲。深入研究這些數字,除了總體利潤數字外,我們還發現了幾個令人鼓舞的因素。

Zooming In On Huadian Energy's Earnings

放大華電能源的收益

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

許多投資者還沒有聽說過現金流的應計比率,但它實際上是衡量公司在給定時期內自由現金流(FCF)在多大程度上支持利潤的有用指標。簡而言之,該比率從淨利潤中減去FCF,然後將該數字除以該時期公司的平均運營資產。你可以將現金流的應計比率視爲 “非FCF利潤率”。

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

因此,負應計比率對公司來說是正數,而正應計比率是負數。這並不意味着我們應該擔心應計比率爲正,但值得注意的是,應計比率相當高的地方。這是因爲一些學術研究表明,高應計率往往會導致利潤下降或利潤增長減弱。

Huadian Energy has an accrual ratio of -0.11 for the year to March 2024. That indicates that its free cash flow was a fair bit more than its statutory profit. Indeed, in the last twelve months it reported free cash flow of CN¥2.1b, well over the CN¥169.1m it reported in profit. Huadian Energy did see its free cash flow drop year on year, which is less than ideal, like a Simpson's episode without Groundskeeper Willie.

截至2024年3月的一年中,華電能源的應計比率爲-0.11。這表明其自由現金流遠超過其法定利潤。事實上,在過去的十二個月中,它報告的自由現金流爲21億元人民幣,遠遠超過其報告的利潤1.691億元人民幣。華電能源的自由現金流確實同比下降,這並不理想,就像辛普森沒有場地管理員威利的劇集一樣。

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Huadian Energy.

注意:我們始終建議投資者檢查資產負債表的實力。點擊此處查看我們對華電能源的資產負債表分析。

Our Take On Huadian Energy's Profit Performance

我們對華電能源盈利表現的看法

As we discussed above, Huadian Energy has perfectly satisfactory free cash flow relative to profit. Based on this observation, we consider it likely that Huadian Energy's statutory profit actually understates its earnings potential! And one can definitely find a positive in the fact that it made a profit this year, despite losing money last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. While conducting our analysis, we found that Huadian Energy has 1 warning sign and it would be unwise to ignore this.

正如我們上面討論的,相對於利潤,華電能源的自由現金流非常令人滿意。基於這一觀察,我們認爲華電能源的法定利潤實際上可能低估了其盈利潛力!儘管去年虧損,但它今年還是實現了盈利,這一事實肯定可以找到積極的一面。本文的目標是評估我們在多大程度上可以依靠法定收益來反映公司的潛力,但還有很多需要考慮的地方。有鑑於此,如果你想對公司進行更多分析,了解所涉及的風險至關重要。在進行分析時,我們發現華電能源有1個警告信號,忽視這一點是不明智的。

This note has only looked at a single factor that sheds light on the nature of Huadian Energy's profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

本報告僅研究了揭示華電能源利潤性質的單一因素。但是,還有很多其他方法可以讓你對公司的看法。例如,許多人認爲高股本回報率是有利的商業經濟的標誌,而另一些人則喜歡 “關注資金”,尋找內部人士正在買入的股票。雖然可能需要你進行一些研究,但你可能會發現這份免費收集的擁有高股本回報率的公司,或者這份內部人士正在購買的股票清單很有用。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。