Ningxia Zhongke Biotechnology Co., Ltd (SHSE:600165) shares have had a horrible month, losing 57% after a relatively good period beforehand. For any long-term shareholders, the last month ends a year to forget by locking in a 61% share price decline.

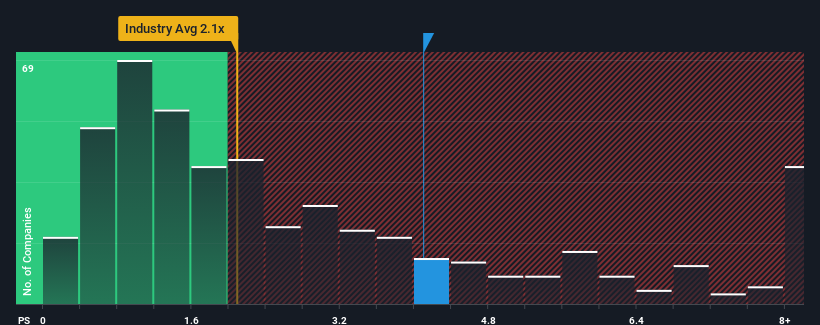

Although its price has dipped substantially, you could still be forgiven for thinking Ningxia Zhongke Biotechnology is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 4.1x, considering almost half the companies in China's Chemicals industry have P/S ratios below 2.1x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

How Ningxia Zhongke Biotechnology Has Been Performing

For example, consider that Ningxia Zhongke Biotechnology's financial performance has been poor lately as its revenue has been in decline. One possibility is that the P/S is high because investors think the company will still do enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Ningxia Zhongke Biotechnology will help you shine a light on its historical performance.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, Ningxia Zhongke Biotechnology would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered a frustrating 58% decrease to the company's top line. Still, the latest three year period has seen an excellent 140% overall rise in revenue, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 23% shows it's noticeably more attractive.

With this information, we can see why Ningxia Zhongke Biotechnology is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

What We Can Learn From Ningxia Zhongke Biotechnology's P/S?

A significant share price dive has done very little to deflate Ningxia Zhongke Biotechnology's very lofty P/S. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Ningxia Zhongke Biotechnology maintains its high P/S on the strength of its recent three-year growth being higher than the wider industry forecast, as expected. Right now shareholders are comfortable with the P/S as they are quite confident revenue aren't under threat. Barring any significant changes to the company's ability to make money, the share price should continue to be propped up.

You always need to take note of risks, for example - Ningxia Zhongke Biotechnology has 3 warning signs we think you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.