Yahoo Finance

Yahoo Finance Carter's (CRI) Q1 Earnings Improve Y/Y, Sales Decline 4.9%

Carter's, Inc. CRI came up with its first-quarter 2024 results, wherein the top line beat the Zacks Consensus Estimate but declined year over year. Nonetheless, the bottom line improved from the year-ago period.

The company experienced higher and earlier-than-expected demand from its largest wholesale customers, attributed to leaner retailer inventories and a need for new seasonal products.

However, cooler weather across many parts of the United States dampened the demand for Carter's Spring product offerings in its U.S. Retail business. Despite these variations, The company anticipates its product innovation, fleet optimization and brand marketing strategies to drive sales trends throughout 2024.

Carter's, Inc. Price, Consensus and EPS Surprise

Carter's, Inc. price-consensus-eps-surprise-chart | Carter's, Inc. Quote

Q1 in Detail

Carter’s reported first-quarter 2024 adjusted earnings of $1.04 per share. The figure rose 6.1% from 98 cents posted in the prior-year quarter.

The company reported consolidated net sales of $661.5 million, which beat the Zacks Consensus Estimate of $633 million. However, the metric declined 4.9% from the $695.9 million posted in the year-ago period. The ongoing impacts of inflation on families with young children, coupled with the delayed onset of spring weather, led to a decrease in demand. Changes in foreign currency exchange rates favorably impacted consolidated net sales by approximately $2 million compared with the year-ago quarter.

Segmental Sales

Sales in the U.S. Retail segment decreased 5% to $307.6 million year over year and surpassed our estimate of $305.1 million. U.S. Retail Comparable net sales fell 6.8% in the first quarter of 2024.

The U.S. Wholesale segment’s sales increased 5.7% year over year to $264.1 million and beat our estimate of $240.8 million.

The International segment witnessed a 2.7% year-over-year drop in revenues from $92.2 million to $89.7 million in the first quarter. The metric surpassed our estimate of $88.9 million.

Image Source: Zacks Investment Research

Margins

Gross profit increased 1.8% year over year to $315.2 million. Meanwhile, the gross margin expanded 310 basis points to 47.6%.

Adjusted operating income decreased 4.3% year over year to $55 million in the reported quarter. The adjusted operating margin increased 20 basis points to 8.3% in the quarter under review.

Selling, general, and administrative (SG&A) expenses increased 2.2% year over year to $265.4 million, reflecting investments in new stores and higher store payroll expenses, partly offset by lower volume-related expenses. As a percentage of net sales, this metric expanded 280 bps year over year to 40.1% in the quarter under review.

Balance Sheet & Shareholder-Friendly Moves

This Zacks Rank #3 (Hold) player ended the first quarter with cash and cash equivalents of $267.6 million, long-term debt of $497.5 million, and shareholders’ equity of $841.4 million.

In the first quarter of 2024, the company returned $38.3 million to shareholders through share repurchases and cash dividends. During the quarter, it repurchased and retired approximately 108 thousand shares of its common stock for $9 million at an average price of $83.48 per share. As of Apr 25, 2023, CRI had a $631-million remaining capacity under its previously announced repurchase authorization.

Also, it paid out a dividend of 80 cents per common share in the said quarter.

Outlook

For the second quarter of 2024, net sales are expected to be $560-$570 million, indicating a decline from the $600 million recorded in the year-ago quarter. Management informed that the earlier Easter and slow start to Spring shopping would impact second-quarter sales.

Adjusted earnings are likely to be 35-45 cents, suggesting a decline from the 64 cents reported in the prior-year quarter. Adjusted operating income is expected to be $25-$30 million, implying a decline from the $38 million recorded in the year-ago quarter.

For 2024, Carter’s expects net sales of $2.95-$3 billion, whereas it reported $2.95 billion in 2023. The company anticipates mid-single-digit growth in adjusted operating income, which was $328 million in 2023. It expects low to mid-single-digit growth in adjusted earnings per share, whereas it reported $6.19 in 2023. Additionally, the company’s operating cash flow is likely to exceed $250 million and it plans a capital expenditure of $80 million.

The forecast for 2024 includes an expected improvement in the macroeconomic environment and consumer demand as the year progresses, leading to a return to low-single-digit comparable sales growth in the U.S. Retail segment in the second half.

Carter’s also anticipates continued conservative inventory commitments by some wholesale customers, gross margin expansion and increased SG&A due to higher growth-related investments and inflation, partially offset by productivity initiatives. Additionally, the forecast indicates lower net interest expenses, a higher effective tax rate and a continued return of capital.

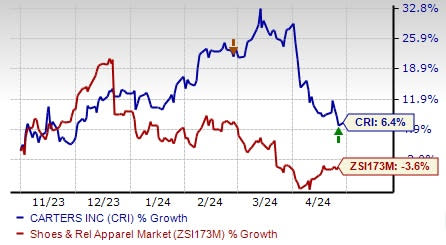

CRI shares have gained 6.4% in the past six months against the industry’s 3.6% decline.

Key Picks

A few better-ranked stocks are American Eagle Outfitters Inc. AEO, Abercrombie & Fitch Co. ANF and The Gap, Inc. GPS.

American Eagle Outfitters is a specialty retailer of casual apparel, accessories and footwear. The company sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for American Eagle Outfitters’ current fiscal-year earnings and sales indicates growth of 12.5% and 3.3% from the year-ago period’s reported figures. AEO has a trailing four-quarter average earnings surprise of 22.7%.

Abercrombie & Fitch is a specialty retailer of premium, high-quality casual apparel. The company currently flaunts a Zacks Rank of 1. ANF has a trailing four-quarter average earnings surprise of 715.6%.

The Zacks Consensus Estimate for Abercrombie & Fitch’s current fiscal-year earnings and sales indicates growth of 19.1% and 5.6% from the year-ago period’s reported figures.

The Gap is a premier international specialty retailer offering a diverse range of clothing, accessories and personal care products. The company has a Zacks Rank of 2 (Buy) at present.

The Zacks Consensus Estimate for The Gap’s current fiscal-year earnings and sales indicates declines of 0.3% and 4.9% from the year-ago period’s reported figures. GPS has a trailing four-quarter average earnings surprise of 180.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

American Eagle Outfitters, Inc. (AEO) : Free Stock Analysis Report

The Gap, Inc. (GPS) : Free Stock Analysis Report

Carter's, Inc. (CRI) : Free Stock Analysis Report