What You Need To Know About The Pulike Biological Engineering, Inc. (SHSE:603566) Analyst Downgrade Today

What You Need To Know About The Pulike Biological Engineering, Inc. (SHSE:603566) Analyst Downgrade Today

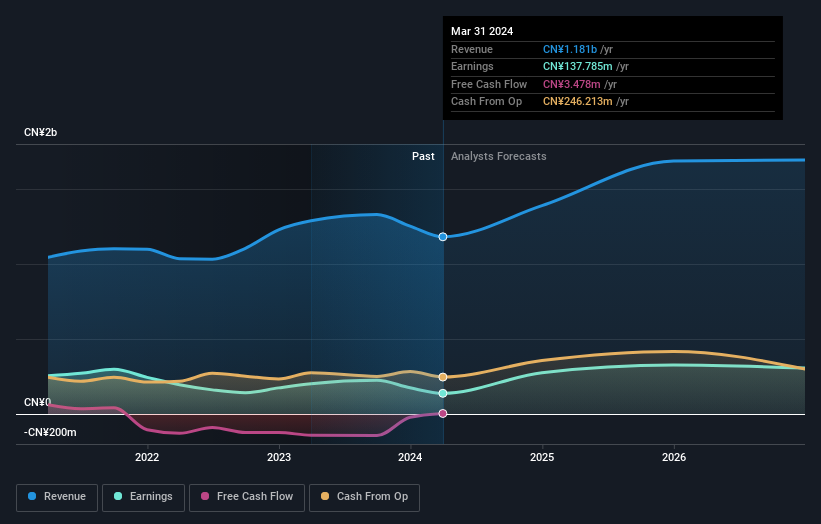

One thing we could say about the analysts on Pulike Biological Engineering, Inc. (SHSE:603566) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative.

关于Pulike Biological Engineering, Inc.(SHSE: 603566)的分析师,我们可以说一件事——他们并不乐观,他们刚刚对该组织的短期(法定)预测进行了重大负面修正。该报告侧重于收入估计,看来该业务的共识已经变得更加保守。

Following the downgrade, the latest consensus from Pulike Biological Engineering's six analysts is for revenues of CN¥1.4b in 2024, which would reflect a meaningful 18% improvement in sales compared to the last 12 months. Per-share earnings are expected to jump 93% to CN¥0.79. Before this latest update, the analysts had been forecasting revenues of CN¥1.6b and earnings per share (EPS) of CN¥0.91 in 2024. Indeed, we can see that the analysts are a lot more bearish about Pulike Biological Engineering's prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

评级下调后,普莱克生物工程的六位分析师的最新共识是,2024年的收入为14亿元人民币,这将反映出与过去12个月相比销售额的18%的显著增长。每股收益预计将增长93%,至0.79元人民币。在最新更新之前,分析师一直预测2024年的收入为16亿元人民币,每股收益(EPS)为0.91元人民币。事实上,我们可以看出,分析师对Pulike Biologic Engineering的前景更加悲观,他们大幅削减了收入预期,并下调了每股收益预期。

The consensus price target fell 12% to CN¥19.98, with the weaker earnings outlook clearly leading analyst valuation estimates.

共识目标股价下跌12%,至19.98元人民币,疲软的盈利前景显然领先于分析师的估值预期。

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We can infer from the latest estimates that forecasts expect a continuation of Pulike Biological Engineering'shistorical trends, as the 18% annualised revenue growth to the end of 2024 is roughly in line with the 15% annual revenue growth over the past five years. Juxtapose this against our data, which suggests that other companies (with analyst coverage) in the industry are forecast to see their revenues grow 15% per year. So although Pulike Biological Engineering is expected to maintain its revenue growth rate, it's only growing at about the rate of the wider industry.

我们可以从大局的角度看待这些估计值的另一种方式,例如预测如何与过去的表现相提并论,以及预测相对于业内其他公司是否或多或少看涨。我们可以从最新估计中推断,预测预计Pulike Biolical Engineering的历史趋势将延续,因为到2024年底的18%的年化收入增长与过去五年15%的年收入增长大致一致。将其与我们的数据并列,后者表明,预计该行业的其他公司(有分析师的报道)的收入每年将增长15%。因此,尽管Pulike Biologic Engineering预计将保持其收入增长率,但其增长速度仅与整个行业差不多。

The Bottom Line

底线

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. There was also a drop in their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider market. Furthermore, there was a cut to the price target, suggesting that the latest news has led to more pessimism about the intrinsic value of the business. Often, one downgrade can set off a daisy-chain of cuts, especially if an industry is in decline. So we wouldn't be surprised if the market became a lot more cautious on Pulike Biological Engineering after today.

要了解的最重要的一点是,分析师下调了每股收益预期,预计业务状况将明显下降。他们的收入估计也有所下降,尽管正如我们之前看到的那样,预计增长仅与整个市场大致相同。此外,还下调了目标股价,这表明最新消息使人们对该业务的内在价值更加悲观。通常,一次降级可能会引发一系列的降级,尤其是在一个行业衰退的情况下。因此,如果今天之后市场对Pulike生物工程变得更加谨慎,我们也不会感到惊讶。

Not only have the analysts been downgrading the stock, but it looks like Pulike Biological Engineering might find it hard to maintain its dividends, if these forecasts prove accurate. For more information, you can click here to learn more about our dividend analysis and the 1 potential risk we've identified.

分析师不仅下调了该股的评级,而且如果这些预测被证明是准确的,看来Pulike Biological Engineering可能很难维持其股息。欲了解更多信息,您可以点击此处详细了解我们的股息分析以及我们已确定的1种潜在风险。

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

当然,看到公司管理层将大量资金投资于股票与了解分析师是否在下调预期一样有用。因此,您可能还希望搜索这份内部人士正在购买的免费股票清单。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。