Some Confidence Is Lacking In Avangrid, Inc.'s (NYSE:AGR) P/E

Some Confidence Is Lacking In Avangrid, Inc.'s (NYSE:AGR) P/E

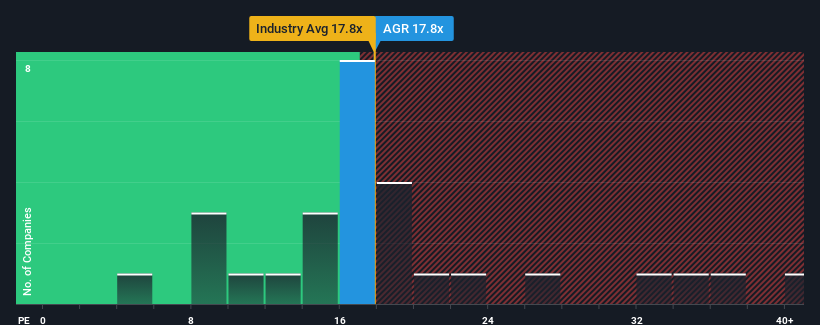

With a median price-to-earnings (or "P/E") ratio of close to 16x in the United States, you could be forgiven for feeling indifferent about Avangrid, Inc.'s (NYSE:AGR) P/E ratio of 17.8x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Recent times haven't been advantageous for Avangrid as its earnings have been falling quicker than most other companies. It might be that many expect the dismal earnings performance to revert back to market averages soon, which has kept the P/E from falling. You'd much rather the company wasn't bleeding earnings if you still believe in the business. If not, then existing shareholders may be a little nervous about the viability of the share price.

Is There Some Growth For Avangrid?

In order to justify its P/E ratio, Avangrid would need to produce growth that's similar to the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 11%. Regardless, EPS has managed to lift by a handy 8.3% in aggregate from three years ago, thanks to the earlier period of growth. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of earnings growth.

Shifting to the future, estimates from the eight analysts covering the company suggest earnings should grow by 8.3% per annum over the next three years. With the market predicted to deliver 10% growth each year, the company is positioned for a weaker earnings result.

In light of this, it's curious that Avangrid's P/E sits in line with the majority of other companies. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as this level of earnings growth is likely to weigh down the shares eventually.

The Final Word

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Avangrid currently trades on a higher than expected P/E since its forecast growth is lower than the wider market. Right now we are uncomfortable with the P/E as the predicted future earnings aren't likely to support a more positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Avangrid (1 is a bit unpleasant) you should be aware of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

在美國,市盈率中位數(或 “市盈率”)接近16倍,你對Avangrid, Inc.感到漠不關心是可以原諒的。”s(紐約證券交易所代碼:AGR)市盈率爲17.8倍。但是,如果市盈率沒有合理的基礎,投資者可能會忽略明顯的機會或潛在的挫折。

最近對Avangrid來說並不是有利的,因爲其收益的下降速度比大多數其他公司快。許多人可能預計,慘淡的收益表現將很快恢復到市場平均水平,這阻止了市盈率的下降。如果你仍然相信公司的業務,你寧願公司不流失收益。如果不是,那麼現有股東可能會對股價的可行性有些緊張。

Avangrid 有一些增長嗎?

爲了證明其市盈率是合理的,Avangrid需要實現與市場相似的增長。

首先回顧一下,該公司去年的每股收益增長並不令人興奮,因爲它公佈了令人失望的11%的跌幅。無論如何,由於較早的增長,每股收益總共比三年前增長了8.3%。因此,儘管股東本來希望保持盈利,但他們會對中期收益增長率大致滿意。

展望未來,報道該公司的八位分析師的估計表明,未來三年收益每年將增長8.3%。預計市場每年將實現10%的增長,因此該公司的盈利業績將疲軟。

有鑑於此,奇怪的是,Avangrid的市盈率與其他大多數公司持平。顯然,該公司的許多投資者沒有分析師所表示的那麼看跌,並且不願意立即放棄股票。維持這些價格將很難實現,因爲這種收益增長水平最終可能會壓低股價。

最後一句話

我們可以說,市盈率的力量主要不是作爲估值工具,而是衡量當前投資者情緒和未來預期。

我們已經確定,Avangrid目前的市盈率高於預期,因爲其預測的增長低於整個市場。目前,我們對市盈率感到不舒服,因爲預期的未來收益不太可能長期支撐更積極的情緒。除非這些條件有所改善,否則很難接受這些合理的價格。

別忘了可能還有其他風險。例如,我們已經確定了你應該注意的 Avangrid 的 2 個警告信號(1 個有點不愉快)。

當然,通過尋找一些優秀的候選人,你可能會找到一筆不錯的投資。因此,來看看這份增長記錄強勁、市盈率低的公司的免費名單吧。

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。

風險及免責聲明

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用瀏覽器的分享功能,分享給你的好友吧