We Think Shareholders Are Less Likely To Approve A Large Pay Rise For UOB-Kay Hian Holdings Limited's (SGX:U10) CEO For Now

We Think Shareholders Are Less Likely To Approve A Large Pay Rise For UOB-Kay Hian Holdings Limited's (SGX:U10) CEO For Now

Key Insights

關鍵見解

- UOB-Kay Hian Holdings will host its Annual General Meeting on 25th of April

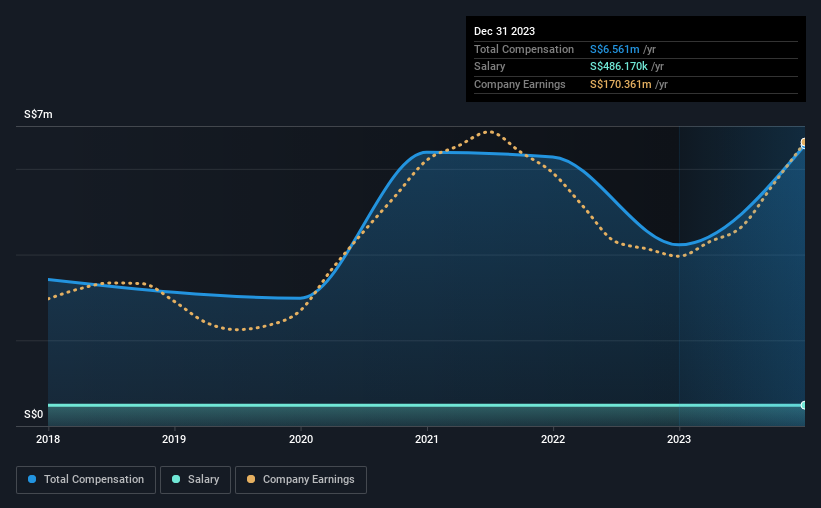

- CEO Ee-Chao Wee's total compensation includes salary of S$486.2k

- The overall pay is 996% above the industry average

- UOB-Kay Hian Holdings' EPS declined by 0.5% over the past three years while total shareholder loss over the past three years was 7.4%

- 大華銀行繼顯控股將於4月25日舉辦年度股東大會

- 首席執行官Ee-Chao Wee的總薪酬包括486.2萬新元的工資

- 總薪酬比行業平均水平高出99.6%

- UOB-Kay Hian Holdings的每股收益在過去三年中下降了0.5%,而過去三年的股東總虧損爲7.4%

In the past three years, the share price of UOB-Kay Hian Holdings Limited (SGX:U10) has struggled to generate growth for its shareholders. Per share earnings growth is also poor, despite revenues growing. The AGM coming up on 25th of April will be an opportunity for shareholders to have their concerns addressed by the board and for them to exercise their influence on management through voting on resolutions such as executive remuneration. Here's why we think shareholders should hold off on a raise for the CEO at the moment.

在過去的三年中,大華繼顯控股有限公司(新加坡證券交易所股票代碼:U10)的股價一直難以爲其股東帶來增長。儘管收入增長,但每股收益增長也很差。即將於4月25日舉行的股東周年大會將爲股東提供一個機會,使他們有機會讓董事會解決他們的擔憂,並通過對高管薪酬等決議進行表決,對管理層施加影響。這就是爲什麼我們認爲股東目前應該推遲對首席執行官的加薪。

Comparing UOB-Kay Hian Holdings Limited's CEO Compensation With The Industry

將大華繼顯控股有限公司的首席執行官薪酬與業界進行比較

At the time of writing, our data shows that UOB-Kay Hian Holdings Limited has a market capitalization of S$1.2b, and reported total annual CEO compensation of S$6.6m for the year to December 2023. We note that's an increase of 55% above last year. We think total compensation is more important but our data shows that the CEO salary is lower, at S$486k.

在撰寫本文時,我們的數據顯示,大華繼顯控股有限公司的市值爲12億新元,並報告稱,截至2023年12月的一年中,首席執行官的年度薪酬總額爲660萬新元。我們注意到,這比去年增長了55%。我們認爲總薪酬更爲重要,但我們的數據顯示,首席執行官的薪水較低,爲48.6萬新元。

For comparison, other companies in the Singapore Capital Markets industry with market capitalizations ranging between S$545m and S$2.2b had a median total CEO compensation of S$599k. Hence, we can conclude that Ee-Chao Wee is remunerated higher than the industry median. Moreover, Ee-Chao Wee also holds S$260m worth of UOB-Kay Hian Holdings stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

相比之下,新加坡資本市場行業中市值介於5.45億新元至22億新元之間的其他公司的首席執行官總薪酬中位數爲599萬新元。因此,我們可以得出結論,Ee-Chao Wee的薪酬高於行業中位數。此外,Ee-Chao Wee還直接以自己的名義持有價值2.6億新元的大華繼顯控股股票,這向我們表明他們在該公司擁有大量個人股份。

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | S$486k | S$486k | 7% |

| Other | S$6.1m | S$3.7m | 93% |

| Total Compensation | S$6.6m | S$4.2m | 100% |

| 組件 | 2023 | 2022 | 比例 (2023) |

| 工資 | 486 萬新元 | 486 萬新元 | 7% |

| 其他 | 610 萬新元 | 370 萬新元 | 93% |

| 總薪酬 | 660 萬新元 | 420 萬新元 | 100% |

Talking in terms of the industry, salary represented approximately 94% of total compensation out of all the companies we analyzed, while other remuneration made up 6% of the pie. It's interesting to note that UOB-Kay Hian Holdings allocates a smaller portion of compensation to salary in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

就行業而言,在我們分析的所有公司中,工資約佔總薪酬的94%,而其他薪酬佔總薪酬的6%。值得注意的是,與整個行業相比,大華銀行繼顯控股將薪酬分配給工資的比例較小。如果將總薪酬傾向於非工資福利,則表明首席執行官的薪酬與公司業績掛鉤。

A Look at UOB-Kay Hian Holdings Limited's Growth Numbers

看看大華繼顯控股有限公司的增長數字

UOB-Kay Hian Holdings Limited saw earnings per share stay pretty flat over the last three years. Its revenue is up 18% over the last year.

在過去三年中,大華銀行繼顯控股有限公司的每股收益保持不變。其收入比去年增長了18%。

The reduction in EPS, over three years, is arguably concerning. But in contrast the revenue growth is strong, suggesting future potential for EPS growth. It's hard to reach a conclusion about business performance right now. This may be one to watch. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

三年內每股收益的下降可以說是令人擔憂的。但相比之下,收入增長強勁,這表明未來每股收益的增長潛力。目前很難就業務績效得出結論。這可能值得關注。雖然我們沒有分析師對公司的預測,但股東們可能需要查看這張詳細的收益、收入和現金流歷史圖表。

Has UOB-Kay Hian Holdings Limited Been A Good Investment?

大華繼顯控股有限公司是一項不錯的投資嗎?

Given the total shareholder loss of 7.4% over three years, many shareholders in UOB-Kay Hian Holdings Limited are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

鑑於三年內股東總虧損7.4%,至少可以說,大華銀行繼顯控股有限公司的許多股東可能相當不滿意。這表明該公司向首席執行官支付過於慷慨的薪水是不明智的。

To Conclude...

總而言之...

The returns to shareholders is disappointing along with lack of earnings growth, which goes some way in explaining the poor returns. Shareholders will get the chance at the upcoming AGM to question the board on key matters, such as CEO remuneration or any other issues they might have and revisit their investment thesis with regards to the company.

股東的回報令人失望,而且收益缺乏增長,這在某種程度上解釋了回報不佳的原因。股東們將有機會在即將舉行的股東周年大會上就關鍵問題向董事會提問,例如首席執行官薪酬或他們可能遇到的任何其他問題,並重新審視他們對公司的投資論點。

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 2 warning signs for UOB-Kay Hian Holdings that investors should think about before committing capital to this stock.

首席執行官薪酬是你關注的關鍵方面,但投資者也需要睜大眼睛關注與業務績效相關的其他問題。這就是爲什麼我們進行了一些挖掘並確定了UOB-Kay Hian Hian Holdings的兩個警告信號,投資者在向該股投入資金之前應考慮這些信號。

Switching gears from UOB-Kay Hian Holdings, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

如果你正在尋找良好的資產負債表和保費回報,那麼從大華銀行凱顯控股公司手中切換方向,那麼這份免費的高回報、低負債公司清單是一個不錯的選擇。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。