Xinjiang Joinworld Co., Ltd.'s (SHSE:600888) price-to-earnings (or "P/E") ratio of 7.1x might make it look like a strong buy right now compared to the market in China, where around half of the companies have P/E ratios above 30x and even P/E's above 55x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Xinjiang Joinworld has been struggling lately as its earnings have declined faster than most other companies. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. You'd much rather the company wasn't bleeding earnings if you still believe in the business. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

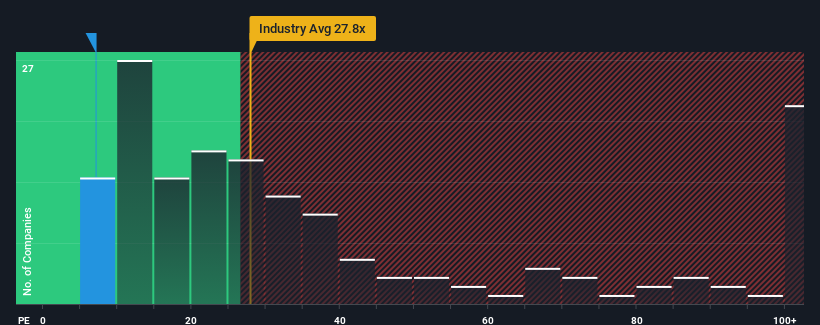

SHSE:600888 Price to Earnings Ratio vs Industry March 6th 2024 Keen to find out how analysts think Xinjiang Joinworld's future stacks up against the industry? In that case, our free report is a great place to start.

Does Growth Match The Low P/E?

Xinjiang Joinworld's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 5.5%. However, a few very strong years before that means that it was still able to grow EPS by an impressive 332% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Looking ahead now, EPS is anticipated to climb by 12% during the coming year according to the lone analyst following the company. Meanwhile, the rest of the market is forecast to expand by 41%, which is noticeably more attractive.

In light of this, it's understandable that Xinjiang Joinworld's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Xinjiang Joinworld maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Having said that, be aware Xinjiang Joinworld is showing 1 warning sign in our investment analysis, you should know about.

You might be able to find a better investment than Xinjiang Joinworld. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 5.5%. However, a few very strong years before that means that it was still able to grow EPS by an impressive 332% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 5.5%. However, a few very strong years before that means that it was still able to grow EPS by an impressive 332% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

如果我們回顧一下去年的收益,令人沮喪的是,該公司的利潤下降了5.5%。但是,在此之前的幾年非常強勁,這意味着它在過去三年中仍然能夠將每股收益總額增長332%,令人印象深刻。因此,我們可以首先確認該公司在此期間在增加收益方面總體上做得非常出色,儘管在此過程中遇到了一些小問題。

如果我們回顧一下去年的收益,令人沮喪的是,該公司的利潤下降了5.5%。但是,在此之前的幾年非常強勁,這意味着它在過去三年中仍然能夠將每股收益總額增長332%,令人印象深刻。因此,我們可以首先確認該公司在此期間在增加收益方面總體上做得非常出色,儘管在此過程中遇到了一些小問題。