First Bancorp (NASDAQ:FBNC) Shareholders Have Lost 18% Over 1 Year, Earnings Decline Likely the Culprit

First Bancorp (NASDAQ:FBNC) Shareholders Have Lost 18% Over 1 Year, Earnings Decline Likely the Culprit

While not a mind-blowing move, it is good to see that the First Bancorp (NASDAQ:FBNC) share price has gained 15% in the last three months. But in truth the last year hasn't been good for the share price. In fact, the price has declined 21% in a year, falling short of the returns you could get by investing in an index fund.

虽然不是一个令人难以置信的举动,但很高兴看到第一银行(纳斯达克股票代码:FBNC)的股价在过去三个月中上涨了15%。但实际上,去年对股价不利。实际上,价格在一年内下跌了21%,未达到投资指数基金所能获得的回报。

If the past week is anything to go by, investor sentiment for First Bancorp isn't positive, so let's see if there's a mismatch between fundamentals and the share price.

如果说过去一周有意义的话,投资者对First Bancorp的情绪并不乐观,所以让我们看看基本面与股价之间是否存在不匹配的情况。

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

用本杰明·格雷厄姆的话来说:从短期来看,市场是一台投票机器,但从长远来看,它是一台称重机。考虑市场对公司的看法发生了怎样的变化的一种不完美但简单的方法是将每股收益(EPS)的变化与股价走势进行比较。

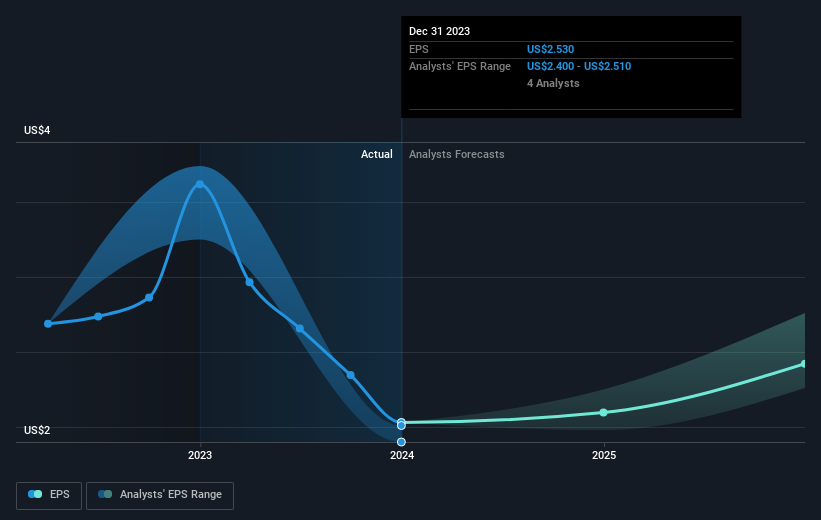

Unhappily, First Bancorp had to report a 39% decline in EPS over the last year. The share price fall of 21% isn't as bad as the reduction in earnings per share. So the market may not be too worried about the EPS figure, at the moment -- or it may have expected earnings to drop faster.

不幸的是,第一银行不得不报告去年每股收益下降了39%。股价下跌21%还不如每股收益的下降那么严重。因此,目前市场可能不太担心每股收益的数字,或者可能预计收益会更快地下降。

You can see below how EPS has changed over time (discover the exact values by clicking on the image).

你可以在下面看到 EPS 是如何随着时间的推移而变化的(点击图片发现确切的值)。

We consider it positive that insiders have made significant purchases in the last year. Even so, future earnings will be far more important to whether current shareholders make money. This free interactive report on First Bancorp's earnings, revenue and cash flow is a great place to start, if you want to investigate the stock further.

我们认为,内部人士在去年进行了大量收购,这是积极的。即便如此,未来的收益对于当前股东是否赚钱将更为重要。如果你想进一步调查First Bancorp的收益、收入和现金流,这份关于First Bancorp收益、收入和现金流的免费互动报告是一个很好的起点。

What About Dividends?

分红呢?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. It's fair to say that the TSR gives a more complete picture for stocks that pay a dividend. As it happens, First Bancorp's TSR for the last 1 year was -18%, which exceeds the share price return mentioned earlier. And there's no prize for guessing that the dividend payments largely explain the divergence!

重要的是要考虑任何给定股票的股东总回报率和股价回报率。基于股息再投资的假设,股东总回报率纳入了任何分拆或贴现资本筹集的价值以及任何股息。可以公平地说,股东总回报率为支付股息的股票提供了更完整的画面。碰巧的是,First Bancorp在过去一年的股东总回报率为-18%,超过了前面提到的股价回报率。而且,猜测股息支付在很大程度上解释了这种分歧是没有好处的!

A Different Perspective

不同的视角

Investors in First Bancorp had a tough year, with a total loss of 18% (including dividends), against a market gain of about 18%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. On the bright side, long term shareholders have made money, with a gain of 0.1% per year over half a decade. It could be that the recent sell-off is an opportunity, so it may be worth checking the fundamental data for signs of a long term growth trend. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Case in point: We've spotted 2 warning signs for First Bancorp you should be aware of.

First Bancorp的投资者经历了艰难的一年,总亏损了18%(包括股息),而市场涨幅约为18%。但是,请记住,即使是最好的股票有时也会在十二个月内表现不如市场。好的一面是,长期股东赚了钱,在过去的五年中,每年增长0.1%。最近的抛售可能是一个机会,因此可能值得查看基本面数据以寻找长期增长趋势的迹象。我发现将长期股价视为业务绩效的代表非常有趣。但是,要真正获得见解,我们还需要考虑其他信息。一个很好的例子:我们已经发现了First Bancorp的两个警告信号,你应该注意。

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

还有很多其他公司有内部人士购买股票。你可能不想错过这份业内人士正在收购的成长型公司的免费名单。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

请注意,本文引用的市场回报反映了目前在美国交易所交易的股票的市场加权平均回报。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。