Optimism Around Deluxe Family (SHSE:600503) Delivering New Earnings Growth May Be Shrinking as Stock Declines 11% This Past Week

Optimism Around Deluxe Family (SHSE:600503) Delivering New Earnings Growth May Be Shrinking as Stock Declines 11% This Past Week

As an investor its worth striving to ensure your overall portfolio beats the market average. But its virtually certain that sometimes you will buy stocks that fall short of the market average returns. Unfortunately, that's been the case for longer term Deluxe Family Co., Ltd. (SHSE:600503) shareholders, since the share price is down 38% in the last three years, falling well short of the market decline of around 26%. Shareholders have had an even rougher run lately, with the share price down 18% in the last 90 days.

作爲投資者,值得努力確保您的整體投資組合超過市場平均水平。但幾乎可以肯定的是,有時候你會買入低於市場平均回報率的股票。不幸的是,豪華家庭有限公司(SHSE: 600503)的長期股東就是這種情況,因爲股價在過去三年中下跌了38%,遠低於26%左右的市場跌幅。股東們最近的表現更加艱難,股價在過去90天中下跌了18%。

After losing 11% this past week, it's worth investigating the company's fundamentals to see what we can infer from past performance.

在上週下跌了11%之後,值得研究該公司的基本面,看看我們可以從過去的表現中推斷出什麼。

View our latest analysis for Deluxe Family

查看我們對豪華家庭的最新分析

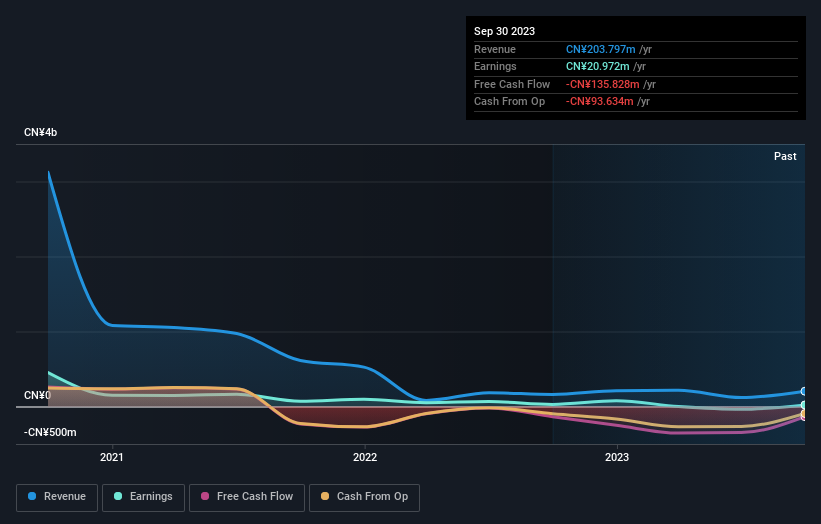

We don't think that Deluxe Family's modest trailing twelve month profit has the market's full attention at the moment. We think revenue is probably a better guide. As a general rule, we think this kind of company is more comparable to loss-making stocks, since the actual profit is so low. It would be hard to believe in a more profitable future without growing revenues.

我們認爲,Deluxe Family過去十二個月的微薄利潤目前並未引起市場的充分關注。我們認爲收入可能是更好的指導。通常,我們認爲這種公司更能與虧損股票相提並論,因爲實際利潤太低了。如果收入不增加,很難相信未來會有更有利可圖的未來。

In the last three years Deluxe Family saw its revenue shrink by 98% per year. That's definitely a weaker result than most pre-profit companies report. On the face of it we'd posit the share price fall of 11% compound, over three years is well justified by the fundamental deterioration. It would probably be worth asking whether the company can fund itself to profitability. Of course, it is possible for businesses to bounce back from a revenue drop - but we'd want to see that before getting interested.

在過去的三年中,豪華家庭的收入每年減少98%。這絕對比大多數盈利前公司報告的結果要差。從表面上看,我們認爲股價在三年內複合下跌11%,這完全是基本面惡化所證明的。可能值得一問的是,該公司能否爲自己籌集資金以實現盈利。當然,企業有可能從收入下降中恢復過來——但我們希望在產生興趣之前先看看這一點。

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

下圖描繪了收入和收入隨着時間的推移而發生的變化(點擊圖片顯示確切的數值)。

You can see how its balance sheet has strengthened (or weakened) over time in this free interactive graphic.

您可以在這張免費的交互式圖片中看到其資產負債表如何隨着時間的推移而增強(或減弱)。

A Different Perspective

不同的視角

The total return of 17% received by Deluxe Family shareholders over the last year isn't far from the market return of -18%. So last year was actually even worse than the last five years, which cost shareholders 5% per year. Weak performance over the long term usually destroys market confidence in a stock, but bargain hunters may want to take a closer look for signs of a turnaround. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Take risks, for example - Deluxe Family has 3 warning signs (and 1 which is a bit concerning) we think you should know about.

去年,豪華家庭股東獲得的總回報率爲17%,與-18%的市場回報率相差不遠。因此,去年的情況實際上比過去五年還要糟糕,後者每年使股東損失5%。長期表現疲軟通常會破壞市場對股票的信心,但討價還價者可能需要仔細觀察轉機的跡象。儘管市場狀況可能對股價產生的不同影響值得考慮,但還有其他因素更爲重要。例如,冒險吧——豪華家庭有 3 個警告標誌(其中 1 個有點令人擔憂),我們認爲你應該知道。

But note: Deluxe Family may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

但請注意:豪華家庭可能不是最值得購買的股票。因此,來看看這份過去盈利增長(以及進一步增長預測)的有趣公司的免費清單。

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Chinese exchanges.

請注意,本文引用的市場回報反映了目前在中國交易所交易的股票的市場加權平均回報率。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St 的這篇文章本質上是籠統的。我們僅使用公正的方法提供基於歷史數據和分析師預測的評論,我們的文章並非旨在提供財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不會考慮最新的價格敏感型公司公告或定性材料。華爾街只是沒有持有上述任何股票的頭寸。

譯文內容由第三人軟體翻譯。