Despite an already strong run, Zhidao International (Holdings) Limited (HKG:1220) shares have been powering on, with a gain of 152% in the last thirty days. The annual gain comes to 137% following the latest surge, making investors sit up and take notice.

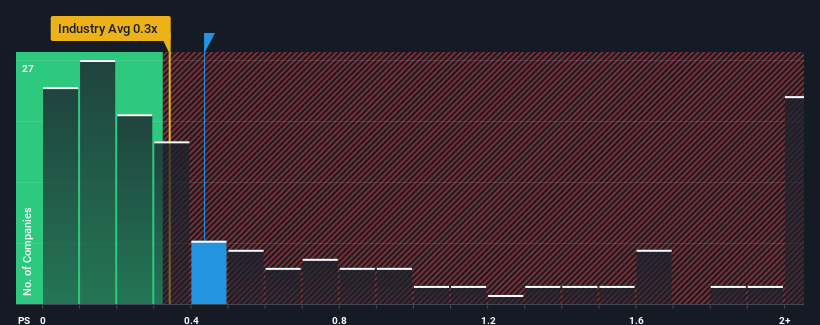

Although its price has surged higher, you could still be forgiven for feeling indifferent about Zhidao International (Holdings)'s P/S ratio of 0.4x, since the median price-to-sales (or "P/S") ratio for the Construction industry in Hong Kong is also close to 0.3x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

See our latest analysis for Zhidao International (Holdings)

SEHK:1220 Price to Sales Ratio vs Industry December 18th 2023

What Does Zhidao International (Holdings)'s Recent Performance Look Like?

Zhidao International (Holdings) certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. Perhaps the market is expecting future revenue performance to taper off, which has kept the P/S from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Although there are no analyst estimates available for Zhidao International (Holdings), take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.

What Are Revenue Growth Metrics Telling Us About The P/S?

The only time you'd be comfortable seeing a P/S like Zhidao International (Holdings)'s is when the company's growth is tracking the industry closely.

If we review the last year of revenue growth, the company posted a terrific increase of 206%. Pleasingly, revenue has also lifted 300% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

When compared to the industry's one-year growth forecast of 13%, the most recent medium-term revenue trajectory is noticeably more alluring

In light of this, it's curious that Zhidao International (Holdings)'s P/S sits in line with the majority of other companies. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

What Does Zhidao International (Holdings)'s P/S Mean For Investors?

Zhidao International (Holdings) appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We didn't quite envision Zhidao International (Holdings)'s P/S sitting in line with the wider industry, considering the revenue growth over the last three-year is higher than the current industry outlook. It'd be fair to assume that potential risks the company faces could be the contributing factor to the lower than expected P/S. It appears some are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Zhidao International (Holdings) (1 is potentially serious!) that you need to be mindful of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly.

儘管已經表現強勁,但智道國際(控股)有限公司(HKG:1220)的股價一直在上漲,在過去三十天中上漲了152%。在最近的飆升之後,年漲幅達到137%,這讓投資者大吃一驚。

儘管其價格飆升,但你對智道國際(控股)0.4倍的市盈率漠不關心仍然是可以原諒的,因爲香港建築業的市盈率(或 “市盈率”)中位數也接近0.3倍。但是,如果市盈率沒有合理的基礎,投資者可能會忽視明顯的機會或潛在的挫折。

查看我們對智道國際(控股)的最新分析

香港交易所:1220 市銷比與行業的比率 2023 年 12 月 18 日

智道國際(控股)最近的表現如何?

智道國際(控股)最近確實做得很好,因爲它的收入增長非常快。也許市場預計未來的收入表現將逐漸減弱,這使市盈率無法上升。如果你喜歡這家公司,你會希望情況並非如此,這樣你就有可能在它不太有利的情況下買入一些股票。

儘管沒有分析師對智道國際(控股)的估計,但請看一下這個數據豐富的免費可視化,看看該公司如何增加收益、收入和現金流。

收入增長指標告訴我們有關市盈率的哪些信息?

看到像智道國際(控股)這樣的市盈率只有當公司的增長密切關注行業時,你才會感到舒服。

如果我們回顧一下去年的收入增長,該公司公佈了206%的驚人增長。令人高興的是,得益於過去12個月的增長,總收入也比三年前增長了300%。因此,可以公平地說,該公司最近的收入增長非常好。

與該行業預測的13%一年增長相比,最新的中期收入軌跡明顯更具吸引力

有鑑於此,奇怪的是,智道國際(控股)的市盈率與其他大多數公司持平。顯然,一些股東認爲最近的表現已達到極限,並一直在接受較低的銷售價格。

智道國際(控股)的市盈率對投資者意味着什麼?

智道國際(控股)似乎重新受到青睞,股價穩步上漲,使其市盈率與業內其他公司持平。通常,在做出投資決策時,我們謹慎行事,不要過多地考慮市售比率,儘管這可以充分揭示其他市場參與者對公司的看法。

考慮到過去三年的收入增長高於當前的行業前景,我們並不完全設想智道國際(控股)的市盈率將與整個行業保持一致。可以公平地假設,該公司面臨的潛在風險可能是市盈率低於預期的原因。看來有些人確實在預測收入不穩定,因爲這些最近的中期條件的持續存在通常會提振股價。

我們不想在遊行隊伍中下太多雨,但我們也發現智道國際(控股)有兩個警告標誌(其中一個可能很嚴重!)你需要注意的。

重要的是要確保你尋找一家優秀的公司,而不僅僅是你遇到的第一個想法。因此,如果盈利能力的增長與你對一家優秀公司的想法一致,那就來看看這份免費名單吧,列出了最近收益增長強勁(市盈率低)的有趣公司。

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。