Yahoo Finance

Yahoo Finance Do MindChamps PreSchool's (SGX:CNE) Earnings Warrant Your Attention?

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like MindChamps PreSchool (SGX:CNE). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

See our latest analysis for MindChamps PreSchool

How Quickly Is MindChamps PreSchool Increasing Earnings Per Share?

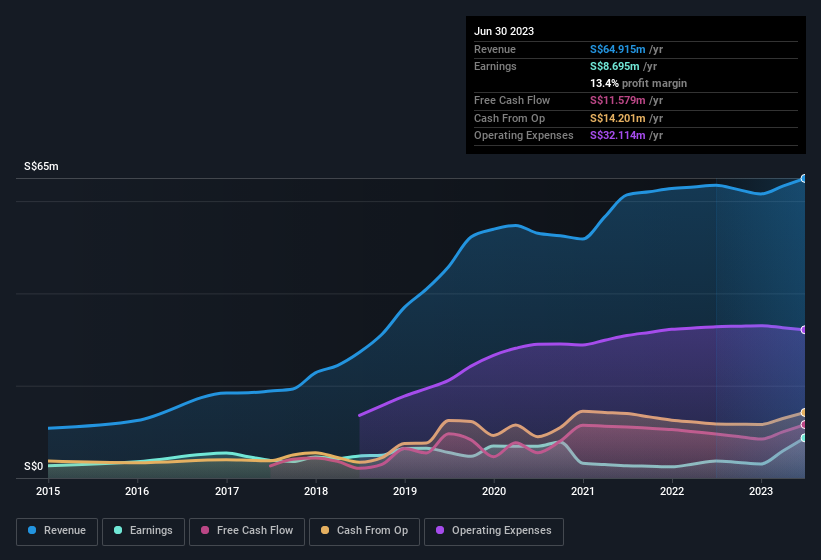

Generally, companies experiencing growth in earnings per share (EPS) should see similar trends in share price. Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. We can see that in the last three years MindChamps PreSchool grew its EPS by 8.1% per year. That growth rate is fairly good, assuming the company can keep it up.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. The music to the ears of MindChamps PreSchool shareholders is that EBIT margins have grown from -2.8% to 0.9% in the last 12 months and revenues are on an upwards trend as well. Ticking those two boxes is a good sign of growth, in our book.

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

MindChamps PreSchool isn't a huge company, given its market capitalisation of S$60m. That makes it extra important to check on its balance sheet strength.

Are MindChamps PreSchool Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

The good news for MindChamps PreSchool shareholders is that no insiders reported selling shares in the last year. So it's definitely nice that Non-Independent Non-Executive Director Catherine Du bought S$11k worth of shares at an average price of around S$0.15. It seems that at least one insider is prepared to show the market there is potential within MindChamps PreSchool.

Does MindChamps PreSchool Deserve A Spot On Your Watchlist?

One important encouraging feature of MindChamps PreSchool is that it is growing profits. It's not easy for business to grow EPS, but MindChamps PreSchool has shown the strengths to do just that. Despite there being a solitary insider adding to their holdings, it's enough to consider adding this to the watchlist. It's still necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with MindChamps PreSchool (at least 1 which is a bit unpleasant) , and understanding them should be part of your investment process.

Keen growth investors love to see insider buying. Thankfully, MindChamps PreSchool isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.