Why It Might Not Make Sense To Buy PNE Industries Ltd (SGX:BDA) For Its Upcoming Dividend

Why It Might Not Make Sense To Buy PNE Industries Ltd (SGX:BDA) For Its Upcoming Dividend

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. An unusually high payout ratio of 326% of its profit suggests something is happening other than the usual distribution of profits to shareholders. A useful secondary check can be to evaluate whether PNE Industries generated enough free cash flow to afford its dividend. Over the last year, it paid out more than three-quarters (83%) of its free cash flow generated, which is fairly high and may be starting to limit reinvestment in the business.

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. An unusually high payout ratio of 326% of its profit suggests something is happening other than the usual distribution of profits to shareholders. A useful secondary check can be to evaluate whether PNE Industries generated enough free cash flow to afford its dividend. Over the last year, it paid out more than three-quarters (83%) of its free cash flow generated, which is fairly high and may be starting to limit reinvestment in the business. Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see PNE Industries Ltd (SGX:BDA) is about to trade ex-dividend in the next 4 days. The ex-dividend date is one business day before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn't show on the record date. Accordingly, PNE Industries investors that purchase the stock on or after the 25th of May will not receive the dividend, which will be paid on the 16th of June.

普通讀者會知道我們喜歡 Simply Wall St 的分紅,這就是爲什麼看到它令人興奮的原因 PNE 工業有限公司 (SGX: BDA) 即將在未來4天內進行除息交易。除息日是記錄日期前一個工作日,這是股東在公司賬簿上有資格獲得股息支付的截止日期。除息日是需要注意的重要日期,因爲在此日期或之後購買任何股票都可能意味着未在記錄日期顯示的延遲結算。因此,在5月25日或之後購買股票的PNE Industries投資者將不會獲得股息,股息將在6月16日支付。

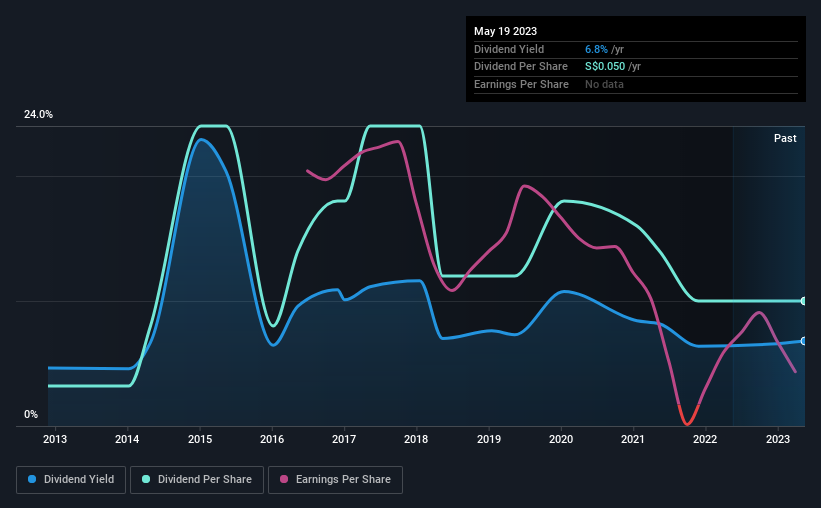

The company's next dividend payment will be S$0.01 per share. Last year, in total, the company distributed S$0.05 to shareholders. Based on the last year's worth of payments, PNE Industries stock has a trailing yield of around 6.8% on the current share price of SGD0.735. If you buy this business for its dividend, you should have an idea of whether PNE Industries's dividend is reliable and sustainable. So we need to check whether the dividend payments are covered, and if earnings are growing.

該公司的下一次股息將爲每股0.01新元。去年,該公司總共向股東分配了0.05新元。根據去年的付款價值,PNE Industries股票的後續收益率約爲6.8%,而目前的股價爲0.735新元。如果你收購這家企業是爲了獲得股息,你應該知道PNE Industries的股息是否可靠和可持續。因此,我們需要檢查股息支付是否包括在內,以及收益是否在增長。

Check out our latest analysis for PNE Industries

查看我們對 PNE Industries 的最新分析

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. An unusually high payout ratio of 326% of its profit suggests something is happening other than the usual distribution of profits to shareholders. A useful secondary check can be to evaluate whether PNE Industries generated enough free cash flow to afford its dividend. Over the last year, it paid out more than three-quarters (83%) of its free cash flow generated, which is fairly high and may be starting to limit reinvestment in the business.

股息通常從公司收入中支付,因此,如果公司支付的股息超過其收入,則其股息被削減的風險通常更高。其利潤的326%的異常高的派息率表明,除了通常向股東分配利潤之外,還有其他事情正在發生。一個有用的輔助檢查可以是評估PNE Industries是否產生了足夠的自由現金流來支付股息。去年,它支付了其產生的自由現金流的四分之三(83%)以上,相當高,可能開始限制對該業務的再投資。

It's good to see that while PNE Industries's dividends were not covered by profits, at least they are affordable from a cash perspective. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Extraordinarily few companies are capable of persistently paying a dividend that is greater than their profits.

很高興看到,儘管PNE Industries的股息沒有被利潤所覆蓋,但至少從現金的角度來看,它們是負擔得起的。儘管如此,如果該公司一再支付的股息超過其利潤,我們會感到擔憂。極少數公司能夠持續支付高於其利潤的股息。

Click here to see how much of its profit PNE Industries paid out over the last 12 months.

點擊此處查看PNE Industries在過去12個月中支付了多少利潤。

Have Earnings And Dividends Been Growing?

收益和股息一直在增長嗎?

When earnings decline, dividend companies become much harder to analyse and own safely. If earnings fall far enough, the company could be forced to cut its dividend. PNE Industries's earnings have collapsed faster than Wile E Coyote's schemes to trap the Road Runner; down a tremendous 34% a year over the past five years.

當收益下降時,股息公司變得更加難以分析和安全擁有。如果收益下降得足夠遠,該公司可能被迫削減股息。PNE Industries的收益暴跌速度快於Wile E Coyote誘捕Road Runner的計劃;在過去五年中,每年大幅下降34%。

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. PNE Industries has delivered an average of 12% per year annual increase in its dividend, based on the past 10 years of dividend payments. The only way to pay higher dividends when earnings are shrinking is either to pay out a larger percentage of profits, spend cash from the balance sheet, or borrow the money. PNE Industries is already paying out 326% of its profits, and with shrinking earnings we think it's unlikely that this dividend will grow quickly in the future.

衡量公司股息前景的另一種關鍵方法是衡量其歷史股息增長率。根據過去10年的股息支付情況,PNE Industries的股息平均每年增長12%。在收益萎縮時支付更高股息的唯一方法是要麼支付更大比例的利潤,要麼從資產負債表中花錢,要麼借錢。PNE Industries已經支付了其利潤的326%,由於收益萎縮,我們認爲該股息將來不太可能迅速增長。

Final Takeaway

最後的外賣

Is PNE Industries an attractive dividend stock, or better left on the shelf? It's never fun to see a company's earnings per share in retreat. Additionally, PNE Industries is paying out quite a high percentage of its earnings, and more than half its cash flow, so it's hard to evaluate whether the company is reinvesting enough in its business to improve its situation. Bottom line: PNE Industries has some unfortunate characteristics that we think could lead to sub-optimal outcomes for dividend investors.

PNE Industries 是一隻有吸引力的股息股,還是最好留在貨架上?看到公司的每股收益下降從來都不是一件好事。此外,PNE Industries支付的收益佔其收益的比例相當高,現金流超過一半,因此很難評估該公司對其業務的再投資是否足以改善其狀況。底線:PNE Industries有一些不幸的特徵,我們認爲這些特徵可能會給股息投資者帶來不理想的結果。

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with PNE Industries. Every company has risks, and we've spotted 5 warning signs for PNE Industries (of which 2 can't be ignored!) you should know about.

話雖如此,如果你在不太擔心股息的情況下看待這隻股票,那麼你仍然應該熟悉PNE Industries所涉及的風險。每家公司都有風險,我們已經發現 PNE Industries 的 5 個警告標誌 (其中 2 個不容忽視!)你應該知道。

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

如果您在市場上尋找實力雄厚的股息支付者,我們建議 查看我們精選的頂級股息股票。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?擔心內容嗎? 取得聯繫 直接和我們在一起。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St 的這篇文章本質上是籠統的。 我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。 它不構成買入或賣出任何股票的建議,也沒有考慮您的目標或財務狀況。我們的目標是爲您提供由基本面數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感公司公告或定性材料。簡而言之,華爾街在上述任何股票中都沒有頭寸。

譯文內容由第三人軟體翻譯。