Improved Earnings Required Before Parkson Retail Asia Limited (SGX:O9E) Stock's 26% Jump Looks Justified

Improved Earnings Required Before Parkson Retail Asia Limited (SGX:O9E) Stock's 26% Jump Looks Justified

Despite an already strong run, Parkson Retail Asia Limited (SGX:O9E) shares have been powering on, with a gain of 26% in the last thirty days. This latest share price bounce rounds out a remarkable 810% gain over the last twelve months.

儘管運行已經很強勁, 百盛零售亞洲有限公司 新加坡交易所:O9E)股票一直在通電,在過去三十天內獲得 26% 的收益。最新的股價反彈使過去十二個月內獲得了 810% 的顯著收益。

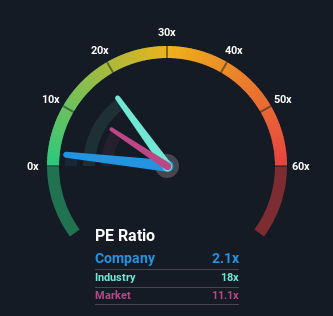

In spite of the firm bounce in price, given close to half the companies in Singapore have price-to-earnings ratios (or "P/E's") above 12x, you may still consider Parkson Retail Asia as a highly attractive investment with its 2.1x P/E ratio. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

儘管公司的價格反彈,鑑於接近一半的新加坡公司的股價收益比率(或「市盈率」)高於 12 倍,您仍然可以認為百盛亞洲零售亞洲是一項具有 2.1x P/E 比率的極具吸引力的投資。但是,由於某種原因,P/E 可能相當低,需要進一步調查以確定是否合理。

Parkson Retail Asia certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

百盛亞洲零售業肯定最近做得很好,因為它的收入正在以非常快的速度增長。可能是許多人預計強勁的盈利表現會大幅下降,這使市盈利壓抑了市盈率,如果沒有結果發生,那麼現有股東有理由對股價的未來方向非常樂觀。

See our latest analysis for Parkson Retail Asia

查看我們有關百盛亞洲零售的最新分析

Does Growth Match The Low P/E?

增長是否匹配低 P/E?

Parkson Retail Asia's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

百盛亞洲零售業的市盈率對於預期增長極差甚至收益下降的公司來說,是典型的,而且更重要的是,表現比市場差很多。

If we review the last year of earnings growth, the company posted a terrific increase of 81%. However, the latest three year period hasn't been as great in aggregate as it didn't manage to provide any growth at all. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

如果我們回顧盈利增長的去年,該公司發布了 81% 的驚人增長。但是,最近三年的時間並沒有總體那麼大,因為它根本沒有設法提供任何增長。因此,可以公平地說,最近公司的收益增長不一致。

This is in contrast to the rest of the market, which is expected to grow by 3.7% over the next year, materially higher than the company's recent medium-term annualised growth rates.

這與市場其他市場形成鮮明對比,預計明年將增長 3.7%,遠高於該公司近期的中期年化增長率。

In light of this, it's understandable that Parkson Retail Asia's P/E sits below the majority of other companies. It seems most investors are expecting to see the recent limited growth rates continue into the future and are only willing to pay a reduced amount for the stock.

有鑑於此,百盛亞洲零售的 P/E 低於大多數其他公司是可以理解的。似乎大多數投資者都期望看到近期的有限增長率將繼續到未來,並且只願意為股票支付較低的金額。

What We Can Learn From Parkson Retail Asia's P/E?

我們可以從百盛零售亞洲的市盈科學到什麼?

Shares in Parkson Retail Asia are going to need a lot more upward momentum to get the company's P/E out of its slump. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

百盛亞洲零售的股票將需要更多的向上動力才能使公司的 P/E 擺脫低迷。通常情況下,在進行投資決策時,我們會提防不要太多地閱讀價格與收益比,儘管它可以揭示很多其他市場參與者對公司的看法。

We've established that Parkson Retail Asia maintains its low P/E on the weakness of its recent three-year growth being lower than the wider market forecast, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. If recent medium-term earnings trends continue, it's hard to see the share price rising strongly in the near future under these circumstances.

我們已確定百盛亞洲零售業保持低位,原因是其近三年增長疲軟低於更廣泛的市場預測,正如預期的那樣。在這個階段,投資者認為盈利改善的潛力不足以證明更高的市盈率是合理的。如果近期的中期盈利趨勢持續下去,在這種情況下,股價在不久的將來強勁上漲是很難看到的。

It's always necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with Parkson Retail Asia (at least 2 which make us uncomfortable), and understanding these should be part of your investment process.

總是有必要考慮永遠存在的投資風險幽靈。 我們在百盛亞洲零售業發現了 4 個警告標誌 (至少有 2 個使我們感到不舒服),並且了解這些應該是您投資過程的一部分。

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a P/E below 20x.

當然, 通過查看幾個優秀的候選人,您可能會發現一個夢幻般的投資。 因此,請先看看這個 自由 具有強勁增長記錄的公司名單,在 20 倍以下的市盈率交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?關注內容? 取得聯繫 直接與我們聯繫。 或者,通過電子郵件發送電子郵件給編輯團隊。

這篇文章由簡單牆聖是一般性質. 我們僅使用公正的方法,根據歷史數據和分析師預測提供評論,我們的文章並不打算作為財務建議。 它並不構成購買或出售任何股票的建議,也不會考慮您的目標或您的財務狀況。我們的目標是為您帶來由基本數據驅動的長期集中分析。請注意,我們的分析可能不會考慮最新的價格敏感公司公告或定性材料。簡易華街在提及的任何股票中都沒有倉位。

譯文內容由第三人軟體翻譯。