Qian Hu Corporation Limited's (SGX:BCV) 26% Jump Shows Its Popularity With Investors

Qian Hu Corporation Limited's (SGX:BCV) 26% Jump Shows Its Popularity With Investors

The Qian Hu Corporation Limited (SGX:BCV) share price has done very well over the last month, posting an excellent gain of 26%. Notwithstanding the latest gain, the annual share price return of 2.2% isn't as impressive.

該 錢湖股份有限公司 SGX:BCV)股價在過去一個月表現非常好,錄得 26% 的極佳收益。儘管有最新收益,2.2% 的年度股價回報率並不那麼令人印象深刻。

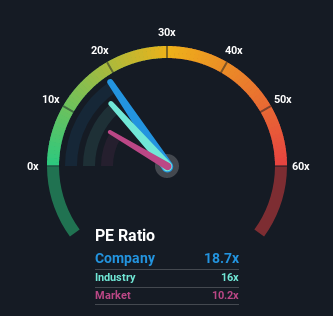

After such a large jump in price, Qian Hu may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 18.7x, since almost half of all companies in Singapore have P/E ratios under 10x and even P/E's lower than 6x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

經過這麼大的價格上漲之後,錢胡可能在目前以 18.7x 的價格對盈利(或「P/E」)比率發出非常看跌的信號,因為幾乎一半的新加坡公司的 P/E 比率低於 10 倍,甚至 P/E 低於 6x 也不尋常。儘管如此,我們需要更深入地研究以確定是否有高度升高的 P/E 的合理基礎。

For instance, Qian Hu's receding earnings in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

例如,錢胡近期收益下調將是一些值得考慮的食物。許多人可能希望該公司在未來一段時間內仍然超越大多數其他公司,這使得 P/E 不會崩潰。你真的希望如此, 否則你付出了相當高昂的代價沒有特別的原因.

View our latest analysis for Qian Hu

查看我們的最新分析

Is There Enough Growth For Qian Hu?

錢湖有足夠的成長嗎?

In order to justify its P/E ratio, Qian Hu would need to produce outstanding growth well in excess of the market.

為了證明其市盈率的合理性,錢胡需要在市場之外產生出色的增長。

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 19%. Even so, admirably EPS has lifted 52% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

如果我們回顧盈利的最後一年,令人沮喪的是,該公司的利潤下降到 19% 的調整。即便如此,儘管過去 12 個月,令人欽佩的每股收益比三年前總增長了 52%。因此,儘管他們寧願繼續運行,但股東可能會歡迎中期盈利增長率。

In contrast to the company, the rest of the market is expected to decline by 2.9% over the next year, which puts the company's recent medium-term positive growth rates in a good light for now.

與該公司相比,市場其餘部分預計將在未來一年下降 2.9%,這使得該公司近期的中期正增長率目前處於良好狀態。

In light of this, it's understandable that Qian Hu's P/E sits above the majority of other companies. Investors are willing to pay more for a stock they hope will buck the trend of the broader market going backwards. However, its current earnings trajectory will be very difficult to maintain against the headwinds other companies are facing at the moment.

有鑑於此,錢胡的 P/E 位於大多數其他公司之上是可以理解的。投資者願意為股票付出更多,他們希望將推動更廣泛的市場向後走勢。但是,其目前的盈利軌跡將非常難以抵禦其他公司目前面臨的不利因素。

The Bottom Line On Qian Hu's P/E

底線上錢胡的 P/E

Qian Hu's P/E is flying high just like its stock has during the last month. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

錢胡的 P/E 正在高飛,就像上個月的股票一樣。僅使用股價與盈利比率來確定您是否應該出售股票並不明智,但這可能是公司未來前景的實用指南。

We've established that Qian Hu maintains its high P/E on the strength of its recentthree-year growth beating forecasts for a struggling market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Our only concern is whether its earnings trajectory can keep outperforming under these tough market conditions. Otherwise, it's hard to see the share price falling strongly in the near future if its earnings performance persists.

正如預期的那樣,我們已經確定了錢胡保持其最近三年增長的強度,超過了對掙扎的市場預測的高 P/E。在這個階段,投資者認為盈利惡化的可能性不足以證明較低的市盈率是合理的。我們唯一關注的是,在這些艱難的市場條件下,它的收益軌跡能否保持優於表現。否則,如果股票的盈利表現持續存在,很難看到股價在不久的將來強烈下跌。

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for Qian Hu that you should be aware of.

在投資之前,還有其他重要的風險因素需要考慮,我們已經發現 1 個錢湖的警告標誌 你應該知道的。

If P/E ratios interest you, you may wish to see this free collection of other companies that have grown earnings strongly and trade on P/E's below 20x.

如果 P/E 比率利息你,你不妨看看這個 自由 收入強勁增長並在市盈率低於 20 倍交易的其他公司的集合。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?關注內容? 取得聯繫 直接與我們聯繫。 或者,通過電子郵件發送電子郵件給編輯團隊。

這篇文章由簡單牆聖是一般性質. 我們僅使用公正的方法,根據歷史數據和分析師預測提供評論,我們的文章並不打算作為財務建議。 它並不構成購買或出售任何股票的建議,也不會考慮您的目標或您的財務狀況。我們的目標是為您帶來由基本數據驅動的長期集中分析。請注意,我們的分析可能不會考慮最新的價格敏感公司公告或定性材料。簡易華街在提及的任何股票中都沒有倉位。

譯文內容由第三人軟體翻譯。