要知道,

要知道,

Source: Geek Park

Author: Cao Siqi

$XIAOMI-W (01810.HK)$ Delivered the "strongest annual report" since the company was established 15 years ago.

Growth may not be a new thing, but for giants, especially in fiercely competitive sectors like Smart Phones and Autos, achieving a 35% growth is indeed very challenging.

It should be noted that, $Apple (AAPL.US)$ and$Tesla (TSLA.US)$This year's revenue growth rates were only 2% and 1%. In the Internet industry, the rising star ByteDance achieved a growth rate of 40% in 2023.

It should be noted that, $Apple (AAPL.US)$ and$Tesla (TSLA.US)$This year's revenue growth rates were only 2% and 1%. In the Internet industry, the rising star ByteDance achieved a growth rate of 40% in 2023.

More importantly, with the success of car manufacturing, XIAOMI's image has undergone a transformation in 2024. The noise around "XIAOMI Autos 0.099 million" before the listing has dissipated, and the average selling price of XIAOMI Autos has exceeded 0.234 million yuan, with a quarterly gross margin of 20.4%, surpassing that of the intended high-end brand, which is recognized by the market.

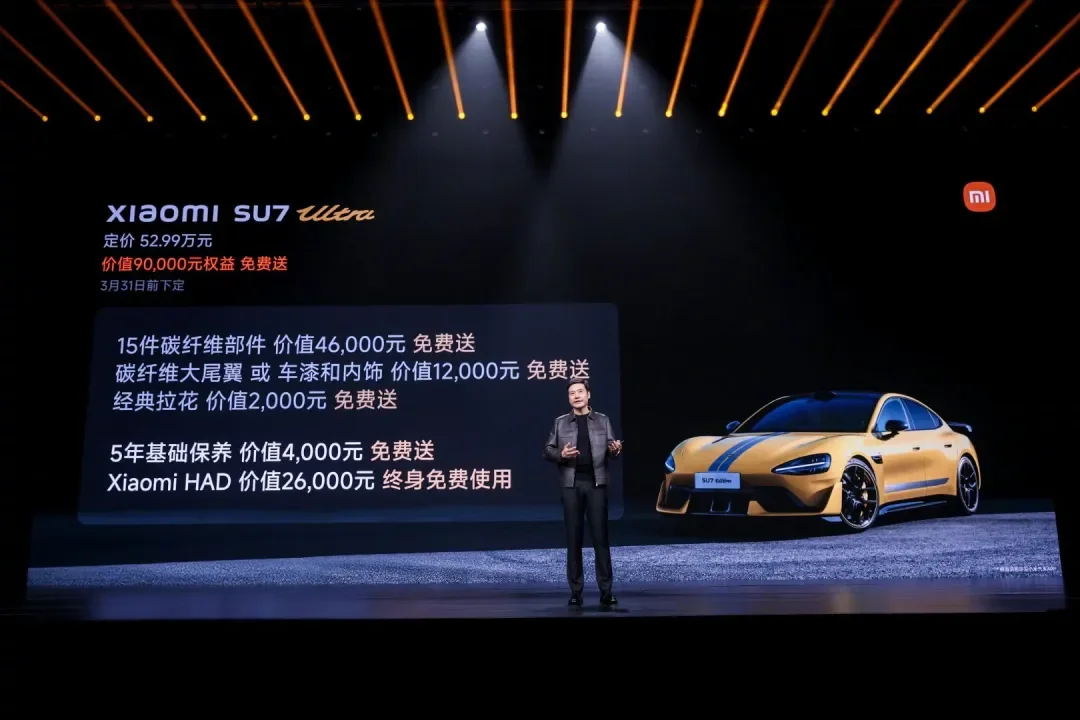

The starting price of the XIAOMI SU7 Ultra is 0.5299 million yuan, and within 3 days of its launch, the number of locked orders exceeded 0.01 million, achieving its annual KPI ahead of schedule.

XIAOMI's president Lu Weibing also stated at the earnings communication meeting that more attention will be paid to improving product structure rather than focusing solely on sales and market share.

In the past year, XIAOMI's market cap has tripled in the secondary market. Now, XIAOMI hopes to continue to reshape the image of its brand and product strength in the minds of consumers.

1. The better the car sells, the better the phone sells.

In the Hardware field, it's hard not to envy XIAOMI's rapid growth in 2024.

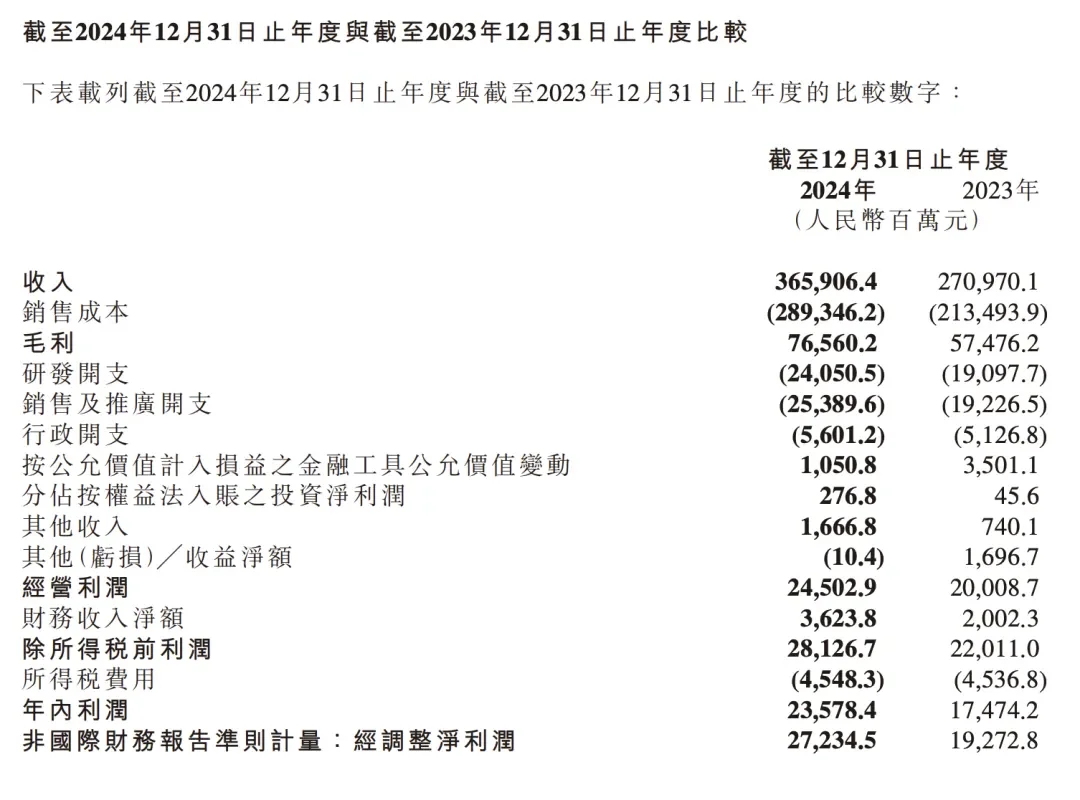

In 2024, XIAOMI-W's total revenue reached 365.91 billion yuan, a year-on-year increase of 35.0%. The gross margin was 76.56 billion yuan, and the operating profit was 24.5 billion yuan, representing growth of 33.2% and 22.5%, respectively.

Currently, this growth rate of 35.0% is far higher than other Hardware giants, and it can match only the high growth of top Internet companies - referring to relevant media reports, ByteDance's revenue growth in 2023 was about 40%. In contrast, the other two major international giants in the mobile phone and Smart Automobile industry, Apple and Tesla, achieved only 2.0% and 1% revenue growth in 2024, respectively.

XIAOMI-W's 2024 revenue data | Image source: Earnings Reports.

In 2024, XIAOMI-W's Autos business had an ASP (Average Selling Price) of 0.234 million yuan. If readers still remember the public price guessing game before the launch of the XIAOMI-W SU7 this time last year, this result is clearly the best response to the previous 'XIAOMI-W Autos 0.099 million yuan'.

Moreover, this figure has quietly approached the leader in new forces, Li Auto, which is currently the number one in sales domestically and primarily targets the high-end market.$Li Auto (LI.US)$In 2024, the average vehicle price is 0.2768 million yuan.

Of course, a careful reading of XIAOMI-W's 2024 Earnings Reports reveals that the automotive business is still in the growth phase, with its contribution to revenue not exceeding 10% of total revenue.

However, the launch of Xiaomi's first automobile product, including the subsequent Xiaomi SU7 Ultra challenging the fastest lap at the Nürburgring, has clearly won over countless fans for the Xiaomi brand, significantly building public goodwill and playing an important role in enhancing the image of the Xiaomi brand.

At the performance communication meeting on March 18, Xiaomi's president, Lu Weibing, also stated that Xiaomi Automotive has exhibited significant synergy with Xiaomi's Other Products both online and offline. He provided two examples to support this view:

First, during the Spring Festival in 2025, sales of Xiaomi Autos exceeded daily sales, with many new users who had not previously registered for test drives or had intentions to buy completing transactions during the holiday period. According to common experience in the automotive industry, sales during holidays are only about 30% of daily sales.

Lu Weibing believes that this achievement is closely related to the fact that Xiaomi Autos can utilize Xiaomi's flagship stores in major cities' hypermarkets.

Geek Park's inquiry into the Xiaomi Automotive App found that even one year after its launch, the sales of the Xiaomi SU7 series remain hot and in short supply. Currently, ordering the standard version of the Xiaomi SU7 still has a waiting period of 37-40 weeks.

The second case reflects the reverse promotion of Other Products by Xiaomi Autos. According to Lu Weibing, after the 'Double Ultra' launch event at the end of February, the flagship smartphone product that launched alongside the Xiaomi SU7 Ultra, the Xiaomi 15 Ultra, also saw an 80% year-on-year increase in sales, achieving a breakthrough for Xiaomi phones in the price range above 6000 yuan.

Earnings Reports show that the ASP of Xiaomi smartphones for the whole year of 2024 was 1138.2 yuan, a year-on-year increase of 5.2%. In the fourth quarter following the launch of the Xiaomi 15 series, the ASP of Smart Phones reached 1202.4 yuan, the highest ever.

Another highlight is the growth in the AIoT Business Sector, particularly in major appliances (i.e., "Air Conditioner, Refrigerator, Washing Machine" products). In 2024, Xiaomi's Air Conditioner product shipments exceeded 6.8 million units, with a year-on-year growth rate of over 50%; Refrigerator product shipments exceeded 2.7 million units, with a year-on-year growth rate of over 30%; Washing Machine product shipments exceeded 1.9 million units, with a year-on-year growth rate of over 45%.

Lu Weibing stated that the major appliance market has "huge opportunities," and emphasized that in the mobile phone market, there will be greater focus on improving product structure and enhancing ASP performance rather than just growth scale.

2. Tear off the cost-performance label, with automobile gross margins exceeding expectations, Tesla.

In terms of the auto business, Xiaomi delivered over 0.136 million vehicles in 2024, with total revenue for Xiaomi's Smart Automobile and innovation business division reaching 32.8 billion, and gross margin at 18.5%. Among them, the smart automobile business revenue was 32.1 billion yuan, with an annual gross profit of 6.06 billion yuan.

In the fourth quarter, Xiaomi's automobile deliveries reached 69,697 units, and the gross margin rose to 20.4%, surpassing the current highest gross margin of the new domestic force, Li Auto (20.3%), and exceeding Tesla's gross margin (last year's third quarter, Tesla's gross margin excluding carbon credits was 17.1%).

It can be said that in the auto business, Xiaomi has completely torn off the cost-performance label that it held for many years.

Interestingly, in 2024, the other two rapidly growing car companies, LEAPMOTOR and Xpeng, had fourth-quarter gross margins of 13.3% and 10.0% (this refers to automobile gross margins, Xpeng's overall gross margin reached 14.3%). The market humorously claims that Xiaomi has created a high-end brand label in the automobile sector, while LEAPMOTOR and Xpeng have begun to undertake the cost-performance market that once belonged to Xiaomi.

In the Earnings Reports, the official explanation for the rise in gross margin is: a decrease in the prices of core components, a reduction in unit manufacturing costs due to an increase in production capacity month-on-month, and a decrease in vehicle deliveries benefiting from the launch period.

In simple terms, this means: a decrease in Battery Cell prices, realization of scale advantages, and no need for price cuts or interest-free policies to stimulate Consumer demand.

Additionally, according to some supply chain insiders who informed Geek Park, the Xiaomi SU7, as the first product of Xiaomi Autos, has many components "sourced from international supply chains." Therefore, another core reason for the high gross margin should be reflected in cost management and control capabilities.

It is known that Smart Electric Vehicles are considered an innovative Business. From a technological evolution perspective, intelligence is often placed in a very important position and is seen as the "soul". However, from a commercial standpoint, the development of this Business cannot skip the most fundamental process of the "Manufacturing Industry."

In this regard, Lei Jun's friend He XiaoPeng has felt quite deeply over the past two years. To find out why his own Steel procurement prices were higher than the market, he spent a full 9 months discovering that "the people below have been deceiving you," while he at one point "could not see the fundamentals."

$LEAPMOTOR (09863.HK)$Zhu Jiangming also mentioned that one big secret for LEAPMOTOR to achieve "good but not expensive" is through self-research and production of key core costs to realize effective cost reduction.

Moreover, in managing the manufacturing process and supply chain, Lei Jun, who has been in the mobile phone industry for many years, clearly has more experience than other founders of new forces with a background in the Internet. This also makes Xiaomi's Automotive Business currently appear to have, at least in the manufacturing aspect, not stepped into too many pitfalls.

Please stop saying that "Apple Automobiles lose money for every unit sold," okay?

Of course, the Smart Automobile business of XIAOMI-W is currently not profitable.

The Earnings Reports show that in 2024, XIAOMI-W's Smart Automobile and other innovative businesses incurred a total loss of 6.2 billion yuan.

Then, unsurprisingly, some Keywords began to do elementary school math. 6.2 billion yuan divided by 0.136 million units sold means XIAOMI-W loses 0.046 million yuan for each unit sold.

From the mathematical formula, there seems to be no problem. But please, can we stop calculating like this?

We know that for an automobile company (let's abstract XIAOMI-W's Smart Automobile business as an independent business concept), the costs mainly fall into the following categories:

BOM (Bill of Material), sales cost, research and development cost, administrative cost.

The first item is closely related to "single vehicle performance," which refers to the management of the supply chain and manufacturing mentioned earlier. The latter items generally involve significant investments in aspects such as store setup, factory construction and operation, and technology research and development.

These foundational investments are closely tied to the "scale effect" in the manufacturing industry. In other words, the larger the scale, the more these major investments can be diluted, leading to potential profitability.

From the data in XIAOMI-W's Earnings Reports, it can be seen that in the fourth quarter of 2024, the loss from Xiaomi's automobile business was 0.7 billion yuan (with losses of 1.8 billion yuan and 1.5 billion yuan in Q2 and Q3 respectively). It can also be observed that as delivery scale increases, the losses of Xiaomi's automobile business are gradually narrowing.

Currently, among the "new forces" in automobile manufacturing in China, three companies have achieved profitability, namely: $Li Auto (LI.US)$ 、$Chongqing Sokon Industry Group Stock (601127.SH)$and $LEAPMOTOR (09863.HK)$ Among them, Ideal aims for annual profitability, Chongqing Sokon Industry Group Stock for half-year profitability, and LEAPMOTOR for achieving profitability in a single quarter. Each respectively achieves a sales volume at break-even of approximately 0.36-0.45 million units per year.

On the day the earnings report was released, Lei Jun announced on his personal Weibo account that the delivery expectation for XIAOMI-W automobiles in 2025 was raised from 0.3 million units to 0.35 million units.

Although Lu Weibing stated in last night's conference call that there is currently no clear expectation for the automobile business to turn a profit, the reason being that it is still in a phase of high investment, if this year's XIAOMI-W automobile business can surprise on financial performance, it would not be unexpected.

At least, hope that there will no longer be absurd topics like 'losing money on every car sold'.

For XIAOMI-W's upcoming second SUV product YU7, as well as the rumored third model equipped with an extended-range solution, they will all enter the competitive mainstream arena from the 'differentiation' battlefield corresponding to XIAOMI-W SU7. From this perspective, Lu Weibing's caution seems understandable. However, it is evident that XIAOMI-W has now accumulated enough public goodwill and resources, ready to face the uncertain competition ahead with an upward posture.

Editor/rice

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath. Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Comment(6)

Reason For Report