Kerry Real Estate Research states that thanks to a series of measures such as boosting Consumer spending and stabilizing Asset prices, the housing prices in large and medium-sized cities will welcome more Bullish Signals, and the warmth of the new housing price Index will also accelerate its transmission to the second-hand housing market.

According to Zhitou Financial APP, Ke Rui Real Estate Research predicts that in the first half of 2025, the sales area and amount of commercial housing will accelerate to find a bottom, and more major cities will see a year-on-year recovery in monthly residential transaction volumes. Thanks to measures to boost consumer spending and stabilize asset prices, real estate prices in major cities will show more Bullish Signals, and the warmth of the primary housing price index will also accelerate its transmission to the secondary housing market. In terms of investment and construction, based on the Industry's task to destock and stabilize the market, the land market will continue to focus on quality with a reduced quantity, and the construction area is also expected to accelerate its adjustment to a scale more aligned with new housing sales. New constructions and development investments will still be in a contraction adjustment cycle, but thanks to the support of special bond storage and the promotion of urban village renovations, year-on-year indicators for the first half of the year are expected to see marginal improvements.

Looking ahead to the first half of 2025, based on the positive signals revealed by the central ministries and the Two Sessions at the beginning of the year, as well as the importance placed on stabilizing asset prices, the real estate sector is expected to continue to welcome a series of policy Bullish throughout the year: The demand side will further release housing demand potential, focusing on building "good houses" to support better expectations for property prices and continuously support residents in improving housing conditions through enhanced urban village renovations and fiscal incentives; the supply side will further improve inventory expectations, strengthening the structure of land supply in specific segments while controlling the scale of land supply, and accelerating the promotion of stock housing storage and the recovery of idle land; in terms of financial tools, funding support and risk management will be strengthened, increasing loan placement for the "white list" to fully guarantee project construction and delivery; and further improve the fundamental systems in the commercial housing development and sales process to ensure the quality and timely delivery of new and under-construction projects.

Ke Rui Real Estate Research believes that thanks to the positive signals reflected by current market demand and the support of active central fiscal policies, it is expected that regional authorities will further focus on improving supply and demand expectations in core segments in 2025. As the heat of the land, new housing, and second-hand housing markets transmits and spreads, "demonstration sectors for stabilizing the market" will appear more frequently in more cities.

Ke Rui Real Estate Research believes that thanks to the positive signals reflected by current market demand and the support of active central fiscal policies, it is expected that regional authorities will further focus on improving supply and demand expectations in core segments in 2025. As the heat of the land, new housing, and second-hand housing markets transmits and spreads, "demonstration sectors for stabilizing the market" will appear more frequently in more cities.

Focusing on Industry data and based on the latest guidance from the central ministries to stabilize the market, as well as the stability of trading data in the land, new housing, and second-hand housing markets, trading volume, property prices, inventory, and other Indicators are expected to continue to improve in the first half of 2025. As Chen Changsheng, a member of the drafting group of the "Government Work Report" and deputy director of the State Council Research Office, stated, the housing and stock markets are important barometers of economic running. Stabilizing asset prices can release wealth effects, and changes in asset price forms can boost consumption and promote moderate price rises. Improved Consumer expectations will further feed back into the real estate market, accelerating stabilization.

On the morning of March 17, the National Bureau of Statistics released macroeconomic and real estate data for January and February 2025. On the economic front, thanks to various regions and departments implementing the central policy decisions, economic operations started smoothly at the beginning of the year, showing a favorable development trend, and the growth rates of Indicators like industrial added value and retail sales of consumer goods have accelerated.

The real estate industry continues the stabilization trend started in the fourth quarter of 2024, with core Indicators like development investment, available funds, and sales showing a narrowing year-on-year decline. According to data disclosed by the State Council Information Office, in terms of 40 monitored key cities, the sales area and sales amount of newly built commercial housing increased year-on-year by 1.3% and 7.1% respectively in the first two months. Thanks to the support of special bonds for land storage and local supply-side regulation, land transaction volumes continue to be lower than the scale of commercial housing transactions, while the year-on-year growth rate of residential unsold area has contracted to below 10% for the first time since 2022, with a likelihood of entering a declining channel within the year. As Industry Indicators improve, the National Housing Prosperity Index has risen for two consecutive months, and the effectiveness of the real estate new model transformation is further evident.

01 The macroeconomic outlook is improving at the start, with monetary easing continuing to take effect.

In January-February 2025, the national economy continued its upward trend, with growth rates of industrial added value above designated size, total retail sales of consumer goods, and fixed asset investment accelerating compared to 2024. The specifics are as follows:

First, industrial production grew rapidly, with equipment manufacturing and high-tech manufacturing accelerating. In January-February, the industrial added value above designated size increased by 5.9% year-on-year, accelerating by 0.1 percentage points compared to the entire last year. The added value of high-tech manufacturing grew by 9.1%, accelerating by 0.2 percentage points. Second, market sales growth accelerated, the growth rate of fixed asset investment rebounded, and goods imports and exports remained stable. In January-February, the total retail sales of consumer goods reached 8373.1 billion yuan, a year-on-year growth of 4.0%, accelerating by 0.5 percentage points compared to the entire last year. National fixed asset investments (excluding farmers) reached 5261.9 billion yuan, with a year-on-year increase of 4.1%, accelerating by 0.9 percentage points compared to the entire last year. The total value of goods imports and exports was 6536.4 billion yuan, a year-on-year decline of 1.2%. Third, the employment situation remained generally stable, with the urban surveyed unemployment rate steady. In January-February, the average urban surveyed unemployment rate nationwide was 5.3%.

From the financial data in February, M1 increased by 0.1% year-on-year, marking three consecutive months of positive growth, while M2 year-on-year growth remained at 7.0%. In the second half of 2024, monetary issuance was strengthened, with the M1-M2 spread expanding to a maximum of 10 percentage points in the third quarter. Following the stabilization of the economic situation and the recovery of the Real Estate market since the fourth quarter, the spread has slightly narrowed. Since December 2024, the M1-M spread has been below 7 percentage points for three consecutive months, and residents' consumption willingness continues to recover. On March 16, the "Consumption Boost Special Action Plan" was officially announced, involving various areas of people's livelihood such as childbirth, education, housing, and Autos, and provided clear policy implementation opinions, which will further effectively boost residents' demand. At the end of February, residents' medium and long-term loans reached 62 trillion yuan, a year-on-year increase of 3.4%, with the year-on-year growth rate maintained close to the average of the past six months. With the adjustment of the Real Estate transaction volume to a scale that better matches housing demand, combined with the decline in mortgage rates and the effects of loan replacement, residents' medium and long-term loans are tending to stabilize, forming a positive interaction between the release of housing demand and the consumer boost action.

It should be noted that since the People's Bank of China started compiling January 2025 data, a newly revised narrow money (M1) statistical caliber has been implemented. The revised M1 includes individual demand deposits and customer reserve funds from non-bank payment institutions, and the above M1 has been calculated according to the new caliber.

At the end of February, broad money (M2) balance was 320.52 trillion yuan, a year-on-year growth of 7%. The narrow money (M1) balance was 109.44 trillion yuan, a year-on-year increase of 0.1%. The currency in circulation (M0) balance was 13.28 trillion yuan, a year-on-year increase of 9.7%. In the first two months, a net cash injection of 456.2 billion yuan was made. At the end of the month, the balance of RMB loans was 261.78 trillion yuan, a year-on-year increase of 7.3%. By the end of February 2025, the scale of social financing stock was 417.29 trillion yuan, a year-on-year increase of 8.2%.

02 Transaction scale indicators continue to recover, maintaining a positive momentum of stabilization.

In February, the new housing market transactions continued to stabilize. The transaction scale in first and second-tier cities continued to rise year-on-year, among which the new housing transaction area in Shanghai and Shenzhen rose to 3 times and 2 times year-on-year, respectively. Cities like Suzhou, Wuhan, Chongqing, Fuzhou, and Xuzhou steadily recovered, showing positive growth both year-on-year and month-on-month, with increasingly clear signs of bottoming out and stabilization. Affected by the traditional holiday of the Spring Festival, the enthusiasm of real estate companies to launch new projects has slightly declined, with an average opening and sales rate of 34%, which is 8 percentage points higher than the same period in 2024.

According to data from the National Bureau of Statistics, from January to February, the sales area of new commercial housing nationwide was 0.107 billion square meters, with sales amounting to 1.03 trillion yuan, reflecting a year-on-year decline of 7.8 and 14.5 percentage points respectively, the lowest decline since the beginning of this adjustment cycle, excluding the beginning of 2023 after the pandemic restrictions were lifted, continuing the trend of stabilizing and stopping the decline by the fourth quarter of 2024.

At the beginning of 2025, multiple ministries including the State Council, the central bank, and the Ministry of Housing and Urban-Rural Development have repeatedly expressed their intention to vigorously promote the stabilization of the real estate industry. Especially during the State Council meeting at the beginning of February, it was stated that 'we should dare to break conventions and introduce tangible policies and measures.' Moreover, the term 'good housing' was included in the government work report for the first time. With continuous support from central policies and strong promotion by local governments through city-specific measures, the property market in the core 30 cities began to improve ahead of schedule at the start of 2025, with new housing transaction volume growing by 10% year-on-year, and inventory pressure also continuing to alleviate.

03 The year-on-year decline in housing prices across 70 cities has continued to narrow for four consecutive months, and new home prices in first-tier cities continue to rise.

Looking at the price index of newly built commercial residences and second-hand residences in 70 cities with January 2021 as the base point, the speed of housing price decline further slowed down in February. New home prices have decreased by 7.4% compared to the beginning of 2021, while second-hand home prices have decreased by 17.2% compared to the beginning of 2021. According to data released by the statistics bureau, year-on-year, the decline in sales prices of commercial residences in various cities has continued to narrow. The price of new homes declined by 5.2% year-on-year, narrowing for four consecutive months, while second-hand home prices declined by 7.5% year-on-year, with a narrowing trend for five consecutive months. Among these, first-hand home prices in Shanghai rose by 5.6% year-on-year, while prices in Beijing, Guangzhou, and Shenzhen fell by 5.5%, 7.8%, and 4.4% respectively.

In terms of month-on-month comparisons, new commercial housing prices in first-tier cities continue to rise, with Beijing, Shanghai, and Shenzhen increasing by 0.1%, 0.2%, and 0.4% respectively, while Guangzhou fell by 0.2%. The sales prices of new commercial residences in second-tier cities remained flat month-on-month, and third-tier cities saw new housing prices decrease by 0.3%. Since November 2024, cities where first-hand housing prices have remained stable or increased have exceeded 20 for four consecutive months.

In the government work report released in March 2025, 'stabilizing the real estate and stock markets' was included in the overall requirements of the government work report for the first time, noting that real estate is an important part of residents' asset allocation, and stabilizing asset prices can release wealth effects. As stabilizing housing prices was emphasized more prominently, it is expected that this year local governments will further implement measures of 'de-inventory, loosening credit, and fiscal subsidies' to stabilize residents' price expectations, promote value reconstruction based on the 'good housing' standard, support the price core of properties, strengthen the guarantee of housing delivery, and implement risk prevention measures such as the 'white list' of financing. According to detailed transaction data monitored by CRIC, not only have first-hand housing prices stabilized and improved at the beginning of 2025, but confidence in the second-hand housing market has also spread from improving groups to those with urgent needs.

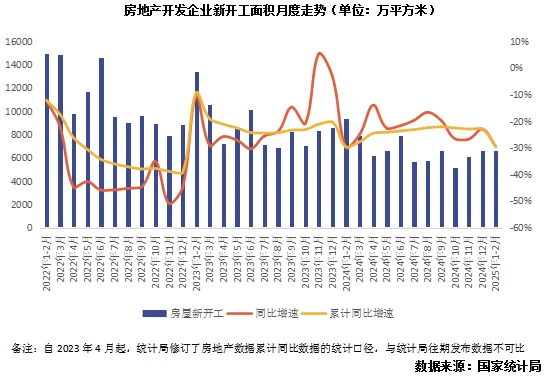

In 2024, new construction at the bottom helps accelerate inventory digestion with a significant slowdown in the year-on-year decline of completion scale.

In January-February 2025, the area of houses constructed by real estate development companies was 6.06 billion square meters, a year-on-year decrease of 9.1%. Among these, the area of residential construction was 4.2 billion square meters, a decrease of 9.7%. The newly started construction area was 66.14 million square meters, a decline of 29.6%. Of these, the new residential construction area was 48.21 million square meters, a decrease of 28.9%.

At the beginning of 2025, the year-on-year decline in real estate construction area further accelerated. The new construction area of 66.14 million square meters is only 61% of the commodity housing sales scale during the same period, indicating that the short-term inventory pressure in the industry is rapidly easing. Additionally, with the decline in land transaction volume at the beginning of 2025, the land transaction area from January to February was only 88.4 million square meters, about 80% of the new housing sales scale during the same period. Considering the non-saleable portions such as supporting constructions and commercial self-held properties, this implies that the long-term inventory scale in real estate has also entered a phase of rapid decline.

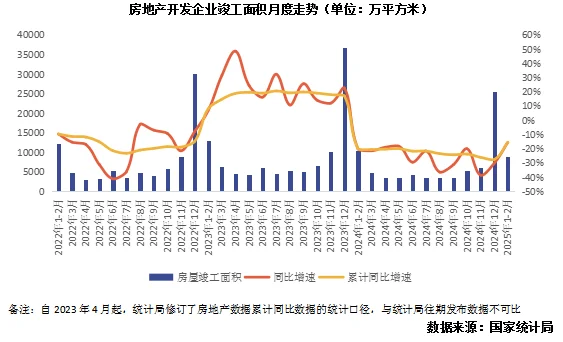

In January-February 2025, the area of houses completed was 87.64 million square meters, a decrease of 15.6%. Among these, the area of completed residential properties was 63.28 million square meters, a drop of 17.7%. Compared to the whole year of 2024, the year-on-year decline in the area of houses completed at the beginning of 2025 has narrowed significantly by 12.1 percentage points. As the industry entered a scale adjustment cycle after 2021, the completion scale is also bound to enter a rapid decline range. Currently, the industry’s completion scale exceeds the new construction scale by about 30%, indicating that the industry’s “guarantee for housing delivery” battle is proceeding smoothly and the industry’s inventory pressure is continuing to ease.

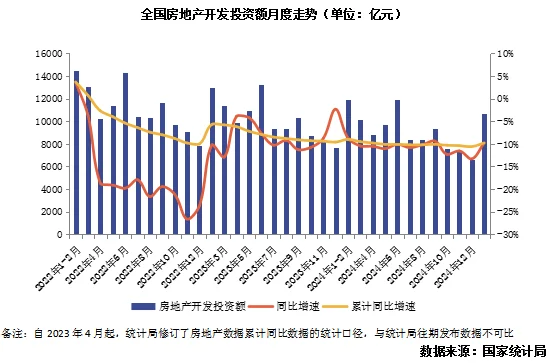

In 2025, the decline in development investment amount year-on-year has narrowed, and corporate investment confidence continues to recover.

In January-February 2025, national real estate development investment was 1,072 billion yuan, a year-on-year decrease of 9.8% (calculated on a comparable basis, see note 6), this decline is 0.8 percentage points narrower than the full year of last year; among these, residential investment was 805.6 billion yuan, a decrease of 9.2%, with a decline of 1.3 percentage points narrowing.

2025年初土地投资规模同比回落,1-2月土地成交建面0.08 billion平方米,同比下降13%,延续了2024年四季度以来的降幅。对比新房交易规模来看,2024年土地成交规模已经低于行业销售规模,在此基础之上,2025年初土地交易量仍在进一步回落,显示出地方主管部门积极去库存的决心。这离不开中央积极财政政策的作用,提高地方债额度、发行专项债、特别国债等举措,大大减轻了2025年地方政府资金面压力。

而房地产开发投资的同比降幅(9.8%)小于土地成交规模(13%),说明企业投资信心持续修复,以及行业融资环境有所改善。2025年以来,中央部委多次强调要进一步改善房地产融资环境,探索拓展宏观审慎和金融稳定功能,维护金融市场稳定。正如3月初中国人民银行行长潘功胜所言,“地方债务和房地产市场风险持续收敛”。一批优质住宅用地已然在2025年初的土地市场中崭露头角,上海、北京、杭州、成都等城市拍出了多宗高溢价高总价土地,企业投资信心持续修复。

不过就中期发展来看,与土地交易规模的下降同步,房地产开发投资规模也会随之继续下行。不过受到往期开发项目投资的影响,开发投资指标存在一定滞后性,开发投资指标的调整时间会慢于新房销售、一二手房价、新开工、土地交易等指标。对标历史行业投资-销售数据比例来看,在房地产投资回落到与商品房销售规模更加匹配的水平之前,该指标的下行调整还将持续一到两年时间。

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Today, after hitting the high near 24,000 in the early session and entering bearish positions, the index fell sharply by nearly over 600 points, immediately recouping yesterday's losses significantly.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath.

Moreover, today it broke the new high again, reaching a maximum of 24,076, but by the end of the market, it fell back by about 70 points, producing a bearish candle. The current trend has not yet been broken, but from the previous low until now, it has risen close to 6,000 points. It is believed that those with positions can continue to hold until there is a clear trend reversal for profit-taking. Those without positions can wait for a pullback to get in. Actually, it is hoped for a quick pullback, as it allows for entry and also provides a healthy breath. Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Currently, the outlook remains the same as before. It is believed that even if there is a pullback, it shouldn't be too deep. However, if Futures fail to stabilize and close below 22,350, there may still be room for decline. The chance of Futures falling below 21,400 in the short term should be low, so it is considered that if a significant pullback occurs, it presents a good opportunity to incrementally go long. Recently, there has been a consistent approach to not hold positions overnight, only focusing on immediate trades, as there is no high chasing and no casual short selling.

Comment(0)

Reason For Report